Optimal Policy Rules in HANK

†

Alisdair McKay Christian K. Wolf

FRB Minneapolis MIT & NBER

March 13, 2023

Abstract: We characterize optimal policy rules in business-cycle models with

nominal rigidities and heterogeneous households. The derived rules are expressed

in terms of the causal effects of policy instruments on policymaker targets. Our

first result is that the optimal policy rule of a “dual mandate” central banker—a

policymaker that only cares about inflation and output—is unaffected by house-

hold heterogeneity. The optimal rule of a Ramsey planner contains an additional

distributional term that incorporates the effects of her available policy instru-

ments on consumption inequality. We quantify the role of this term in a structural

model that incorporates and is consistent with evidence on the key distributional

channels of monetary policy, and we find that the concern for inequality only

has a moderate effect on optimal interest rate policy. Fiscal stimulus payments,

on the other hand, have strongly progressive effects and are thus well-suited to

cushion the distributional effects of cyclical fluctuations.

†

dari, Jordi Gal´ı,

´

Emilien Gouin-Bonenfant, and Ludwig Straub for helpful comments. The views expressed

herein are those of the authors and not necessarily those of the Federal Reserve Bank of Minneapolis or the

Federal Reserve System.

1

1 Introduction

Should household inequality affect the conduct of cyclical stabilization policy? Recent years

have seen a surge of interest in this question, with several prominent studies arguing that the

design of optimal monetary policy is substantially altered by distributional considerations

(e.g., Bhandari et al., 2021; Acharya et al., 2022). In principle, household heterogeneity can

affect optimal policy design in two separate ways. First, household inequality could alter the

transmission from policy instruments to any given target (e.g., inflation and output). This

change in transmission may affect whether or not a policymaker can attain her given targets,

and how policy instruments need to be set to do so. Second, household heterogeneity may

also alter the targets themselves. For example, with market incompleteness, policymakers

may want to dampen the distributional effects of cyclical fluctuations.

We provide new insights into this question by expressing optimal policy rules in business-

cycle models with household heterogeneity in terms of empirically measurable “sufficient

statistics.” Our first contribution is to cast optimal policy problems in a rich heterogeneous-

agent New Keynesian (HANK) environment in linear-quadratic form, closely mirroring the

canonical representative-agent New Keynesian (RANK) literature. As familiar from this lit-

erature, the solution to the linear-quadratic policy problem takes the form of a forecast target

criterion, providing a general characterization of optimal policy completely independently of

the shocks hitting the economy (Giannoni & Woodford, 2002). Drawing on McKay & Wolf

(2023), we furthermore show that these optimal policy rules can be expressed in terms of the

dynamic causal effects of policy instruments on policymaker targets. This “sufficient statis-

tics” characterization of optimal policy rules has two benefits. First, it provides a convenient

organizing device for understanding the literature—differences in optimal policy design can

be traced back to differences in the causal effects of the policy instrument on policymaker

targets. Second, it suggests a natural avenue for model discipline—connect as tightly as

possible with existing empirical evidence on the causal effects of policy interventions.

We then use our sufficient statistics framework to revisit the two ways in which household

heterogeneity can in principle affect optimal policy design. On transmission (i.e., fixing

policymaker targets), we show that the optimal policy rule of a dual mandate central banker

does not change with household heterogeneity. Such heterogeneity may affect the path of

interest rates required to implement the dual mandate optimum, but our sufficient statistics

perspective reveals that the scope even for this is rather limited. On targets, in principle,

distributional concerns can have large effects on optimal stabilization policy. In practice,

2

however, empirical evidence suggests that monetary policy has broad-based effects in the

cross-section of households, with consumption of all households rising following a monetary

easing, and vice-versa. Monetary policy is thus a rather blunt distributional tool, and as a

result a Ramsey planner in an environment consistent with such broad-based effects does

not choose to deviate much from dual mandate policy prescriptions.

Environment. Our analysis is set in a business-cycle model with nominal rigidities and

household heterogeneity. Households face idiosyncratic income risk and self-insure by bor-

rowing and saving in capital, short-term bonds, and long-term bonds. The policymaker sets

short-term nominal interest rates, pays transfers to households, and finances its expenditure

through taxation as well as bond issuance. As we discuss later, the environment is designed

to be rich enough to speak to the core channels of how monetary policy affects consumption

across the cross-section of households.

In this environment we study optimal policy problems cast in linear-quadratic form (e.g.,

Giannoni & Woodford, 2002; Benigno & Woodford, 2012). Linearization of the private-

sector relations of our economy yields the linear constraints. Our quadratic objective is then

either ad hoc—a conventional dual mandate objective—or derived as an approximation to a

particular Ramsey policy problem.

Dual-mandate central banker. We begin our analysis by studying the optimal policy

problem of a conventional “dual-mandate” central banker that seeks to close the output gap

and stabilize inflation. We find this ad hoc loss function useful as a starting point, for two

reasons. First, conceptually, it allows us to explore the effects of changes in policy instrument

propagation while fixing policymaker targets. Second, practically, it is arguably the relevant

objective function for real-world central banks.

Our main result is that the optimal interest rate target criterion for such a dual mandate

central banker is exactly the same as in a standard representative-agent environment. The

logic is as follows. Household heterogeneity in our environment only affects the demand side

of the economy (i.e., the model’s “IS” curve). In the optimal policy problem, however, this

demand block is a slack constraint: the policymaker can pick an output-inflation allocation

subject to the Phillips curve, and then set nominal interest rates as necessary to generate

demand consistent with the desired allocation. Household heterogeneity thus may matter

for the path of the policy instrument, but not for optimal output and inflation outcomes.

Leveraging our sufficient statistics perspective, we then connect these theoretical results

on optimal dual-mandate policy to empirical evidence on monetary policy shock transmis-

3

sion. The empirical literature has tried to identify the causal effects of nominal rate changes

on output and inflation (e.g. see Ramey, 2016). While silent on transmission mechanisms

and so in particular on the importance of heterogeneity-related channels, aggregate data are

informative about the size of interest rate movements required to move output and infla-

tion by a given amount. But it then follows that quantitatively relevant HANK and RANK

models—that is, models that are consistent with the empirical evidence on monetary shock

propagation—will not only share the same optimal dual-mandate policy rule, but they will

in fact also tend to agree quite closely on the interest rate path needed to implement the

optimal inflation and output outcomes. Our quantitative analysis confirms this insight: our

HANK model—which is calibrated to agree with this empirical evidence on monetary shock

propagation—agrees closely with a RANK model calibrated to the same evidence.

Ramsey problem. We next study a Ramsey problem in which the planner seeks to max-

imize a weighted sum of individual household utilities, allowing us to explore the role of

changes in policymaker objectives. Applying a second order approximation, we derive a loss

function that adds to the usual output gap and inflation objectives a third term reflect-

ing distributional concerns. We then solve the policymaker problem of minimizing this loss

function subject to linearized private-sector optimality conditions.

The policymaker’s problem now yields an optimal policy rule consisting of three terms,

trading off the policymaker’s ability to use her policy instrument to stabilize output, infla-

tion, and the cross-sectional consumption distribution. The third term of this rule—which,

importantly, is the sole difference from the optimal standard dual mandate policy rule—is

governed by the distributional incidence of the instrument. If, for example, interest rate

movements do not affect consumption shares (e.g., as in Werning, 2015), then the third term

is zero and the Ramsey rule is identical to the optimal dual-mandate rule; if, on the other

hand, monetary policy has large distributional effects (e.g., as in Bhandari et al., 2021), then

distributional concerns may swamp price and output stability considerations.

To characterize the quantitatively relevant Ramsey policy, we again leverage our sufficient

statistics perspective. As we have discussed, our conclusions on optimal policy will be

governed by the causal effects of interest rate policy on consumption inequality. Since prior

empirical work has delivered the sharpest results on the cross-sectional income incidence of

monetary policy, our strategy is to calibrate our model to match these distributional channels

of monetary policy, and then rely on the structure of the model to infer the ultimate effects on

consumption inequality. Two features of our model turn out to be particularly relevant. First,

4

our model features long-duration assets, allowing us to capture an important redistribution

channel of monetary policy (see Auclert, 2019). Second, the model is designed to generate

only a modest response of aggregate labor income following a monetary expansion, consistent

with empirical evidence. For our purposes, the key takeaway is that the model generates

fairly evenly distributed effects of policy, with consumption responding by similar percentage

amounts across the wealth and income distribution. Given this particular incidence, we find

that monetary policy is rather ill-suited as a tool to deal with the distributional implications

of business-cycle shocks. For example, if—in response to a shock that largely affects the

consumption of the poor—interest rates were set to stabilize consumption at the bottom,

then consumption of other households and so aggregate output and inflation would overshoot.

The Ramsey policymaker does not find such overshooting optimal, and instead responds to

the shock similarly to conventional optimal dual-mandate policy. These quantitative findings

contrast with recent work on optimal monetary policy with heterogeneous households that

tends to find an important role for distributional considerations (e.g., Bhandari et al., 2021;

Acharya et al., 2022; D´avila & Schaab, 2022).

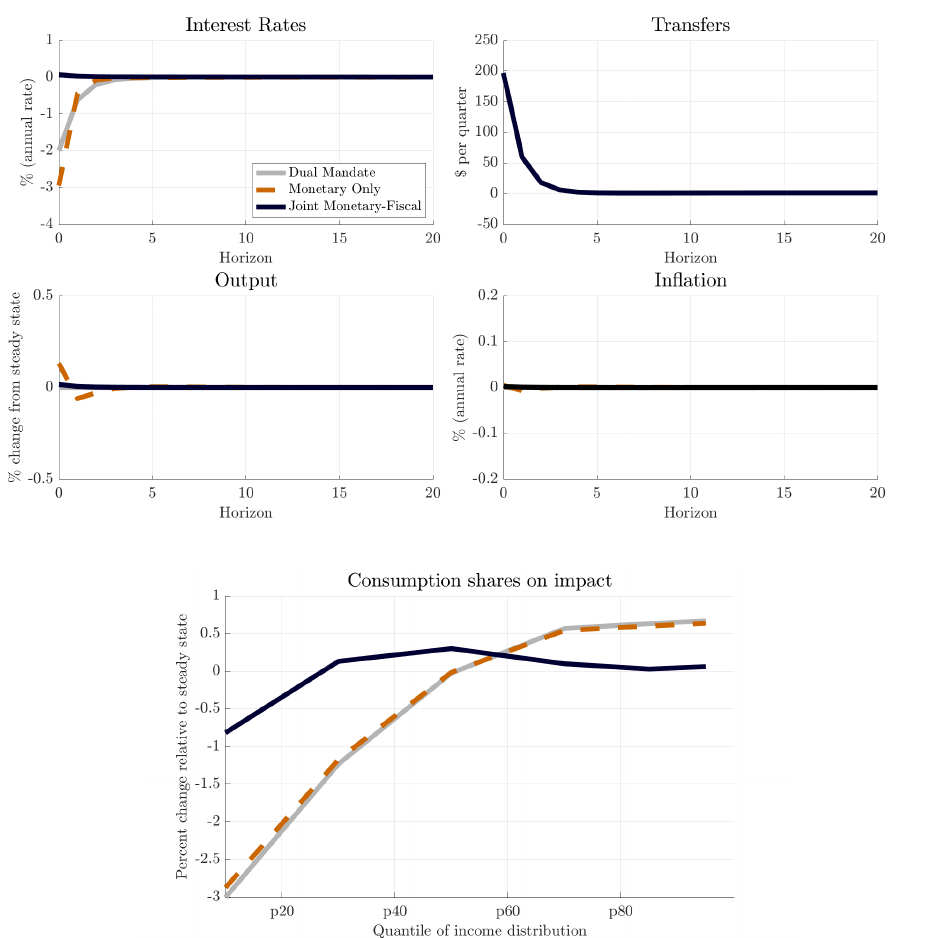

Finally, we also briefly consider a Ramsey policymaker that jointly sets interest rates and

stimulus checks, consistent with recent U.S. policy practice. While equivalent in their effects

on output and inflation (Wolf, 2021), the two instruments differ significantly in their distribu-

tional incidence, with fiscal stimulus payments sharply compressing consumption inequality.

The two instruments are thus highly complementary, with monetary policy primarily aimed

at aggregate stabilization while fiscal policy manages distributional concerns.

Literature. We contribute to the literature on optimal policy in business-cycle models

with rich microeconomic heterogeneity (Acharya et al., 2022; Bhandari et al., 2021; Le Grand

et al., 2022; D´avila & Schaab, 2022). Conceptually, our key contribution is to characterize

optimal policy through forecast target criteria expressed in terms of easily interpretable suf-

ficient statistics. Our computation of these optimal policy rules leverages sequence-space

representations of equilibria and thus the recent work of Auclert et al. (2021).

1

A con-

temporaneous paper that does the same is D´avila & Schaab (2022). Those authors do not

rely on linear-quadratic approximations, thus providing more general optimal policy results,

but without our sufficient statistics perspective. Our discussion of the mapping between

1

By the equivalence of perfect-foresight sequence-space and stochastic linear state-space methods, our tar-

geting criterion also applies to the analogous stochastic linear-quadratic optimal control problem. Sequence-

space linear-quadratic policy problems have been used in prior work to derive “optimal policy projections”

(Svensson, 2005; De Groot et al., 2021; Hebden & Winker, 2021).

5

policy rules and empirical evidence builds on our earlier work in McKay & Wolf (2023).

These conceptual innovations allow us to revisit several substantive results in the prior

heterogeneous-household optimal policy literature.

First, we derive a sharp set of irrelevance results for the effects of inequality on optimal

policy design. Prior work has emphasized that inequality will affect policy propagation by

altering the demand side of the economy (Kaplan et al., 2018; Auclert, 2019); our analysis,

however, reveals that these changes do not affect the optimal “dual mandate” output and in-

flation outcomes. If furthermore matched to the same evidence on policy shock propagation,

then HANK and RANK models will also (roughly) agree on the required rate paths.

Second, our sufficient statistics perspective provides novel insights on the insurance role

of stabilization policy. Our formulation of the Ramsey problem objective isolates the pol-

icymaker’s desire to provide insurance against aggregate shocks with unequal incidence on

consumption across households.

2

In particular, our second-order approximation to the social

welfare function extends a similar finding by Acharya et al. to a more traditional HANK

model that does not permit analytical aggregation. The key benefit of our formulation is that

it delivers a transparent characterization of optimal policy, with the extent to which house-

hold heterogeneity affects the optimal Ramsey policy fully governed by the distributional

effects of the policy instrument. Guided by these insights, and differently from prior work

(e.g., Bhandari et al., 2021; Le Grand et al., 2022), we consider a rich quantitative model

that is consistent with the main distributional channels of monetary stabilization policy.

Finally, our analysis of optimal joint fiscal-monetary policy extends results in Wolf (2021)

and Bilbiie et al. (2021). Wolf (2021) shows that, in a standard HANK setting, transfers and

monetary policy can implement the same aggregate allocations, but differ in their distribu-

tional implications. In a two-agent environment, Bilbiie et al. (2021) argue that monetary

and fiscal policy can together stabilize both the aggregate activity as well as the consump-

tion shares of the two household types. Our work is complementary: we analyze the optimal

monetary-fiscal policy mix in an environment with rich heterogeneity.

Outline. In Section 2, we present a general linear-quadratic sequence-space problem and

its solution. Section 3 outlines our HANK model, and Sections 4 and 5 discuss our results

for optimal dual-mandate and Ramsey policy, respectively. We conclude in Section 6.

2

As such, our formulation of the problem abstracts from many of the issues of time consistency and

inflation bias discussed in D´avila & Schaab (2022).

6

2 Linear-quadratic problems in the sequence space

Throughout this paper we study optimal policy problems that can be recast as deterministic

linear-quadratic control problems. We begin in Section 2.1 by first stating the problem and

presenting its solution. Section 2.2 then places our analysis in the broader context of the

literature, focussing in particular on the tight connection between our expressions and the

(in principle estimable) causal effects of policy shocks.

2.1 Problem & solution

We consider a policymaker that faces a linear-quadratic optimal control problem.

Preferences. The policymaker targets I variables, indexed by i. We let x

it

be the

deviation of the ith target variable from its target value at date t. We consider a policymaker

with quadratic loss function

L ≡

1

2

∞

X

t=0

β

t

I

X

i=1

λ

i

x

2

it

=

1

2

x

x

x

0

(Λ ⊗ W )x

x

x, (1)

where x

x

x

i

≡ (x

i0

, x

i1

, . . . )

0

is the perfect-foresight sequence of the ith target variable through

time and x

x

x ≡ (x

x

x

1

,x

x

x

2

, . . . ,x

x

x

I

)

0

stacks those paths for all of the I targets. The λ

i

’s denote the

weights associated with the different policy targets, with Λ ≡ diag(λ

1

, λ

2

, . . . , λ

I

). Finally

W = diag(1, β, β

2

, . . . ) summarizes the effects of discounting in the policymaker preferences,

with discount factor β ∈ (0, 1).

Constraints. The policymaker faces constraints imposed by the equilibrium relationships

between variables. These linear constraints are expressed compactly as

H

x

x

x

x + H

z

z

z

z + H

ε

ε

ε

ε = 0

0

0, (2)

where z

z

z ≡ (z

z

z

1

,z

z

z

2

, . . . ,z

z

z

J

)

0

stacks time paths for the J policy instruments available to the

policymaker, and ε

ε

ε ≡ (ε

ε

ε

1

,ε

ε

ε

2

, . . . ,ε

ε

ε

Q

)

0

similarly stacks the paths for Q exogenous shocks.

{H

x

, H

z

, H

ε

} are then conformable linear maps.

While the structural models considered in the remainder of this paper directly map into

constraints of the general form (2), it follows from the discussion in McKay & Wolf (2023)

7

that these constraints can equivalently and more conveniently be expressed as

x

x

x

i

=

J

X

j=1

Θ

x

i

,z

j

z

z

z

j

+

Q

X

q=1

Θ

x

i

,ε

q

ε

ε

ε

q

, i = 1, 2, . . . , I (3)

where the Θ’s are linear maps that capture the dynamic causal effects of a policy instrument

path z

z

z

j

or shock path ε

ε

ε

q

on a target variable path x

x

x

i

. The alternative constraint (3) thus

expresses the policy targets directly in terms of impulse responses to policy instruments and

exogenous shocks, as opposed to imposing implicit relationships as in (2).

3

Problem & solution. The optimal policy problem is to choose the instrument paths

z

z

z to minimize (1) subject either to (2) (for the original constraint formulation) or (3) (for

the re-cast constraint). The policymaker thus minimizes a convex objective subject to linear

constraints, and so the first-order conditions are necessary and sufficient for a solution to

the optimal policy problem.

For intuition, it is simpler and more instructive to use the constraint (3). Minimizing (1)

subject to (3) yields:

1. Optimal policy rule. For each policy instrument z

z

z

j

, the paths of the policy targets

satisfy the “policy criterion”

I

X

i=1

λ

i

· Θ

0

x

i

,z

j

W

|

{z }

(discounted) causal effect of z

j

on x

i

· x

x

x

i

= 0

0

0, j = 1, 2, . . . , J (4)

(4) is simply the first-order condition of the optimal policy problem. It says that, for each

instrument z

z

z

j

, the paths of the policy targets x

x

x

i

must be at an optimum within the space

implementable through z

z

z

j

. In the language of Svensson (1997) and Woodford (2003), this

rule is an example of a so-called implicit “target policy criterion”: the policymaker sets the

available instruments to align projections (i.e., future paths) of macro aggregates as well

as possible with its targets, given what is achievable through the available instruments.

3

The equivalence of (2) and (3) would be immediate for invertible H

x

. In typical macroeconomic models,

however, H

x

is not invertible, so recasting the constraint as (3) requires additional arguments. McKay & Wolf

(2023) provide those arguments; briefly, the core intuition is that the optimal policy problem can be shown

to be equivalent to the alternative, artificial problem of picking shocks to a given baseline, determinacy-

inducing policy rule. Policy and non-policy shocks relative to this arbitrary baseline policy rule then yield

the impulse response matrices Θ. See Appendix C.1 for further details.

8

We emphasize two important features of such rules. First, they are derived without

reference to and so apply independently of the non-policy shocks hitting the economy.

This robustness property is one of the main virtues of target policy criteria (Giannoni &

Woodford, 2002). Second, note that the optimal policy rule for instrument j places no

weight on a policy target i that cannot be moved by instrument j (i.e., Θ

x

i

,z

j

= 0), even

if λ

i

> 0—intuitively, if an instrument does not affect a target, then this target plays no

role in setting the instrument.

2. Optimal policy path. Given the exogenous shock paths ε

ε

ε, the policy rule (4) together

with the constraints (3) characterizes the evolution of the dynamic system. In particular,

the optimal instrument path z

z

z

∗

satisfies

z

z

z

∗

≡ −

Θ

0

x,z

(Λ ⊗ W )Θ

x,z

−1

×

Θ

0

x,z

(Λ ⊗ W )Θ

x,ε

ε

ε

ε

, (5)

where Θ

x,z

and Θ

x,ε

suitably stack the individual Θ

x

i

,z

j

’s and Θ

x

i

,ε

q

’s. The optimal path

of the policy instruments thus has an intuitive regression interpretation: the instruments

z

z

z are set to offset as well as possible—in a weighted least-squares sense—the perturbation

to the policy targets x

x

x caused by the exogenous shocks, given as Θ

x,ε

× ε

ε

ε. In particular,

the policymaker will rely most heavily on the tools z

j

that are best suited to offset the

perturbation to its targets induced by a particular shock path ε

ε

ε.

2.2 Discussion

Equations (4) and (5) will guide our analysis in much of the remainder of the paper. In

this section we briefly relate our results to prior work on: first, stochastic linear-quadratic

problems; and second, empirical measurement of the propagation of policy shocks.

Deterministic transitions vs. aggregate risk. It is well-established that, by cer-

tainty equivalence, the first-order perturbation solution of models with aggregate risk is

mathematically identical to linearized perfect-foresight transition paths.

4

This insight im-

plies the following connections between our linear-quadratic perfect foresight problem and

the canonical linear-quadratic stochastic problem (as in Benigno & Woodford, 2012). First,

the policy target criterion (4) corresponds to a forecast targeting criterion in a stochastic

4

For detailed discussions of this point see for example Fern´andez-Villaverde et al. (2016), Boppart et al.

(2018) or Auclert et al. (2021).

9

economy. For a time-0 problem with commitment, that forecast targeting criterion is simply

E

0

"

I

X

i=1

λ

i

· Θ

0

x

i

,z

j

W · x

x

x

i

#

= 0

0

0, j = 1, 2, . . . , J (6)

This is an implicit rule that determines the expected evolution of the economy as of date 0. In

a stochastic environment, new shocks will occur as time goes by, causing the evolution of the

economy to deviate from what was expected at date 0. In this case, (6) gives a rule for how to

revise forecasts at each date. Second, by the same logic, the optimal instrument path z

z

z

∗

in (5)

corresponds to the instrument impulse response to a time-0 shock that changes expectations

of the exogenous shifters from 0

0

0 to ε

ε

ε. The exact same impulse response interpretation applies

to our solution for the paths of the policy targets x

x

x

∗

.

Measurement and interpreation. The matrices stacked in Θ

x,z

collect the dynamic

causal effects of variations in the policy instruments z onto the policymaker targets x. In

other words, the effects of policy instruments on policymaker targets are sufficient statistics

for the characterization of optimal policy rules. This observation will guide much of our

analysis Sections 4.3 and 5.4, and in particular will allow us to transparently relate our find-

ings to those reported in previous work. We also note a useful connection to measurement:

as we show formally in McKay & Wolf (2023), entries of the causal effect maps Θ

x,z

can be

estimated using semi-structural time series methods applied to identified policy shocks (e.g.,

as in Ramey, 2016). We will thus in the subsequent analysis relate our findings as much as

possible to empirical evidence on the effects of (monetary) stabilization policy.

Outlook. In the remainder of this paper we will first show that optimal policy problems in

models with household heterogeneity can be represented in the form of our linear-quadratic

control problem, and then use (4) and (5) to characterize optimal policy rules. Section 3

begins the analysis with a description of our model environment.

3 Model

We consider a HANK economy with two special features. First, labor supply is intermediated

by labor unions. This will allow us to summarize the supply block through a standard Phillips

curve and thus cleanly focus on the demand-side implications of household heterogeneity.

Second, households invest in a menu of assets, which allows us to capture several empirically

10

relevant channels of redistribution induced by monetary policy. Previewing our applications

in Sections 4.3 and 5.4, we note that the model is designed to be just rich enough to be able

to speak to evidence on the aggregate and distributional implications of monetary policy.

Time is discrete and runs forever, t = 0, 1, 2, . . . . Consistent with our linear-quadratic

framework in Section 2, we will consider linearized perfect-foresight transition sequences.

By certainty equivalence, our solutions will be identical to the analogous economy with

aggregate risk and solved using conventional first-order perturbation techniques with respect

to aggregate variables. Throughout this section, boldface denotes time paths (so e.g., x

x

x ≡

(x

0

, x

1

, x

2

, . . . )

0

), bars indicate the model’s deterministic steady state (¯x), and hats denote

(log-)deviations from the steady state (bx).

5

3.1 Households

The economy is populated by a unit continuum of ex-ante identical households indexed by

i ∈ [0, 1]. Household preferences are given by

E

0

∞

X

t=0

β

t

c

1−γ

it

− 1

1 − γ

− ν (`

it

)

, (7)

where c

it

is the consumption of household i and `

it

is its labor supply.

Households face uninsurable risk to their individual incomes. Let ζ

it

be an idiosyncratic

stochastic event that determines the idiosyncratic component of household i’s income at date

t. The idiosyncratic event ζ

it

follows a stationary Markov process. Following Werning (2015)

and Alves et al. (2020), we assume there is an incidence function Φ that maps aggregate

labor income to individual labor income as a function of ζ

it

. Letting e

it

be the labor earnings

of the household, we have

e

it

= Φ(ζ

it

, m

t

, (1 − α)y

t

),

where m

t

is a distributional shock that tilts the incidence function towards or away from

high-income households, and (1 − α)y

t

is aggregate labor income. As we describe in greater

detail below, labor as a whole receives a share 1−α of total income y

t

. The incidence function

Φ thus satisfies

R

e

it

di = (1 − α)y

t

for any value of m

t

and y

t

, and so the shock m

t

only

affects the distribution of labor income, not the total amount. For the quantitative analysis

in Sections 4.3 and 5.4, the shock m

t

will be our example of an inequality shock—a shock

5

To be precise, we use log deviations for the variables {y, c, `, w, b, a, 1+r, 1+i, q

b

, q

k

, η} and level deviations

for the variables {π, τ

x

, τ

e

, m}.

11

that affects aggregate demand through redistribution and precautionary savings motives.

Next, labor supply is determined by a labor market union (described further below), so

hours worked `

it

are taken as given by the household. Total labor income is taxed at some

constant proportional rate τ

y

. Finally households also receive a time-varying lump-sum

transfer τ

x,t

+ τ

e,t

e

it

. The first component of the transfer, τ

x,t

, is the same for all households

and will be manipulated as part of the optimal policy problem; we will refer to it as a “fiscal

stimulus payment” as it resembles the real-world stimulus checks that have been used in

recent recessions in the U.S. The second component, τ

e,t

e

it

, is the “endogenous” component,

adjusting slowly over time to maintain long-run budget balance. This component of transfers

is proportional to the household’s productivity.

Households can save and possibly borrow in a variety of assets with different durations

and different exposures to surprise inflation. Due to certainty equivalence and no-arbitrage,

the returns on all of these assets must be equal at all dates along the equilibrium transition

path except possibly at t = 0, where revaluation effects can lead to heterogeneous realized

returns across households. Let r

t

denote the (equalized) return between t and t + 1, and

furthermore let a

it

denote the net worth of household i at the beginning of period t (inclusive

of interest). The overall budget constraint of household i is then

1

1 + r

t

a

it+1

+ c

it

= a

it

+ (1 − τ

y

+ τ

e,t

)e

it

+ τ

x,t

. (8)

All date-0 revaluation effects will be captured by the initial asset position a

i0

. We will discuss

these revaluation effects later. For now, we note that the distribution of households over

initial states (ζ

i0

, a

i0

) is endogenous, and we write it as Ψ

0

. Finally, we impose a constraint

on total household net worth: a

it+1

≥ a, where a ≤ 0.

The solution to each individual household i’s consumption-savings problem gives a map-

ping from paths of aggregate income y

y

y, real returns r

r

r, transfers τ

τ

τ

x

and τ

τ

τ

e

, shocks m

m

m, and the

initial asset position a

i0

to the path of consumption c

c

c

i

. Aggregating consumption decisions

across all households, we thus obtain an aggregate consumption function C(•):

c

c

c = C(y

y

y, r

r

r,τ

τ

τ

x

,τ

τ

τ

e

,m

m

m; Ψ

0

). (9)

3.2 Technology, unions, and firms

Final goods in our economy are produced by a representative firm that combines intermediate

inputs. Those intermediate goods in turn are produced out of capital and labor, with labor

12

supply intermediated by a union and the total capital stock of the economy fixed—an extreme

form of capital adjustment costs.

Final goods production. The production function of the final goods producer is

y

t

=

Z

j

y

η

t

−1

η

t

jt

dj

η

t

η

t

−1

.

The elasticity of substitution between different intermediate inputs, η

t

, is allowed to vary

(exogenously) over time. This “aggregate supply”-type shock will be important in our dis-

cussion of optimal policy. The final good is sold at nominal price p

t

.

Factor supply. A labor market union intermediates household labor supply. We assume

that hours worked are rationed equally across households, so `

it

= `

t

for all i. Given separable

preferences and with everyone supplying an equal amount of hours worked, it follows that all

households share a common marginal disutility of labor. The marginal utility of consumption,

however, is generally not equalized. For reasons that we will discuss in detail later, we assume

that the union evaluates the benefits of higher after-tax income using the marginal utility of

average consumption (c

−γ

t

) rather than the average of marginal utilities (

R

1

0

c

−γ

it

di), as also

done in Wolf (2021) and Auclert et al. (2021). Under those assumptions, the labor union

agrees to supply `

t

total units of labor at real wage

(1 − τ

y

)w

t

=

ν

0

(`

t

)

c

−γ

t

. (10)

The aggregate capital stock is fixed at k. We assume that capital owners must pay p

t

δ

units of the final good in order to maintain each unit of the capital stock.

Intermediate goods producers. A unit continuum of intermediate goods producers

combine capital and labor according to the production technology

y

jt

= Ak

α

jt

`

1−α

jt

. (11)

Let w

t

be the real wage and let r

k

t

be the real rental rate for capital. Cost minimization by

the intermediate producers implies they all use the same capital-labor ratio, with

`

jt

=

r

k

t

w

t

1 − α

α

k

jt

13

Integrating across firms and using input market clearing we have

w

t

`

t

1 − α

=

r

k

t

k

t

α

.

It thus follows that labor receives a share 1 − α of factor payments, while capital receives

the residual share α. Real marginal cost is common across firms and equal to

µ

t

=

1

A

r

k

t

α

α

w

t

1 − α

1−α

.

Total income is y

t

, with a share µ

t

of that total income going to factor payments and the

residual share 1 − µ

t

going to monopoly profits. We then furthermore assume that a share

1 − α of the monopoly profits is paid to workers in the form of profit sharing, which implies

that labor receives a share 1 − α of total aggregate income y

t

(see Appendix A.1). The union

then distributes this total labor income to households according to the incidence function Φ

introduced above. The remaining share of profits is distributed to capital owners, so capital

owners receive a share α of aggregate income.

Our assumption on profit sharing fixes the labor share at 1−α. In making this assumption

we have removed one potential source of redistribution from policy. The alternative, and

seemingly more natural, assumption that all monopoly profits are paid to capital owners

implies a sharp rise in the labor share following expansionary monetary policy. However, as

we discuss further below, empirical evidence suggests that monetary expansions have little

effect on the labor share (or perhaps even lower it), and so we have designed our model to

be consistent with that evidence.

Each intermediate goods firm sets its price in standard Calvo fashion, with probability

1 − θ of updating the price each period. We show in Appendix A.1 that the solution to this

problem gives rise to a standard linearized perfect-foresight New Keynesian Phillips curve:

bπ

t

= κby

t

+ βbπ

t+1

+ ψbη

t

, (12)

where the composite parameters κ and ψ are functions of model primitives and defined in

Appendix A.1. We furthermore allow for a (time-invariant) subsidy on production financed

with lump-sum taxes on the intermediate goods producers; this subsidy will matter in Sec-

tion 5, where we require efficiency of the deterministic steady state to write our optimal

policy problem in a form consistent with the linear-quadratic set-up of Section 2, exactly as

in prior work (e.g. Woodford, 2003).

14

Aggregate production function. Combining the production functions of final goods

producers and intermediate goods producers, we can write aggregate production as

y

t

=

Ak

α

d

t

`

1−α

t

, (13)

where d

t

≥ 1 captures efficiency losses from price dispersion.

3.3 Asset structure

There are three different assets: a short-term nominal bond, a long-term nominal bond, and

capital. As discussed above, by no-arbitrage, all assets will provide the same returns along

any equilibrium transition path except possibly at t = 0. This section presents the date-t ≥ 1

no-arbitrage relations as well as the date-0 revaluation effects.

Asset returns. The three assets pay out the following real returns.

1. Short-term bond. The short-term nominal interest rate is denoted i

t

. If p

t

dollars are

invested in the short-term bond at date t, then the payoff is valued at (1 + i

t

)p

t

/p

t+1

=

(1 + i

t

)/(1 + π

t+1

) units of goods in the next period.

2. Long-term bond. Households can purchase a unit of the long-term bond for a real price

of q

b

t

. At time t + 1, the household receives a real coupon of (¯r + σ

b

)(1 + π

t+1

)

−1

and

furthermore retains a fraction (1 − σ

b

)(1 + π

t+1

)

−1

of the asset position, now valued at

(1−σ

b

)(1+π

t+1

)

−1

q

b

t+1

. The parameter σ

b

controls the maturity of the asset, with coupons

decaying at rate σ

b

, while the coupon scaling factor (¯r + σ

b

) normalizes the steady-state

price of the bond to one. The inflation term captures the fact that inflation reduces the

real value of all future nominal payouts.

3. Capital. A unit of capital can be purchased for q

k

t

units of the final good. It follows from

our discussion in Section 3.2 that the real payoff of a unit of capital is r

k

t+1

− δ + (1 −

µ

t+1

)αy

t+1

/k + q

k

t+1

= αy

t+1

/k − δ + q

k

t+1

.

Arbitrage relations. By no-arbitrage, all assets must yield the same expected return

at all dates t ≥ 1. Letting r

t

denote the common return on these assets for t ≥ 1, it then

follows from the above discussion that in equilibrium we must have

1 + r

t

=

1 + i

t

1 + π

t+1

(14)

15

1 + r

t

=

(¯r + σ

b

)(1 + π

t+1

)

−1

+ (1 − σ

b

)(1 + π

t+1

)

−1

q

b

t+1

q

b

t

(15)

1 + r

t

=

αy

t+1

/k − δ + q

k

t+1

q

k

t

(16)

Revaluation effects. At time-0, the returns are not necessarily equalized, reflecting

the arrival of surprise shocks. The expressions on the right-hand sides of (14), (15), and (16)

then give us realized returns at date-0 with i

−1

, q

b

−1

, and q

k

−1

at their steady state values.

At the end of period t = −1, the households in our economy had positions in short-

term bonds, long-term bonds, and equities—positions that are then revalued as the date-0

news arrives. We take this initial distribution of portfolios as given; in fact, for our later

quantitative analysis, we will match it directly to empirical evidence on household portfolios.

It follows from the above discussion of revaluation effects that the date-0 distribution of

household asset holdings inclusive of returns, Ψ

0

, depends on π

0

, q

b

0

, q

k

0

, and y

0

. We will

write this mapping as

Ψ

0

= H(y

0

, π

0

, q

b

0

, q

k

0

). (17)

Note that we can use (17) to substitute out for Ψ

0

in the consumption function (9). Lin-

earizing around the deterministic steady state yields the aggregate consumption function

b

c

c

c = C

y

b

y

y

y + C

r

b

r

r

r + C

x

b

τ

τ

τ

x

+ C

e

b

τ

τ

τ

e

+ C

m

b

m

m

m + C

Ψ

H

y

by

0

+ H

π

bπ

0

+ H

b

bq

0

b

+ H

k

bq

0

k

, (18)

where all of the derivative matrices C

•

and H

•

are evaluated at the economy’s deterministic

steady state.

3.4 Government

The final actor in our model is the government. The government collects tax revenue, pays

out lump-sum transfers, sets the nominal interest rate on the short-term bond, and issues

short- as well as long-term bonds. Letting a

g

t

denote the value of claims on the government

entering period t (inclusive of returns), the government budget constraint becomes

a

g

t+1

1 + r

t

= a

g

t

+ τ

x,t

− (τ

y

− τ

e,t

) (1 − α)y

t

| {z }

tax revenue

. (19)

Government debt maturity. We assume that the government issues both long-term as

well as short-term bonds. For all dates t ≥ 1 along the perfect foresight transition path, the

16

returns on the two bonds are equalized and so the maturity structure of the government debt

is irrelevant. At date 0, on the other hand, the maturity structure matters via revaluation,

perfectly analogously to our earlier discussion of valuation effects in household portfolios. In

particular, the revaluation effects will again be embedded in the date-0 portfolio value a

g

0

.

The aggregate bond holdings of the household sector are the liabilities of the government, and

so the revaluation of the government debt is necessarily the mirror image of the revaluation

of the household bond positions.

Policy instruments. We consider the nominal rate of interest i

t

and the exogenous

component of transfers τ

x,t

(i.e., “stimulus checks”) as the independent policy instruments of

the government, used for business-cycle stabilization policy. We assume that the endogenous

component of transfers τ

e,t

adjusts gradually to ensure long-term budget balance:

τ

e,t

= (¯r + σ

τ

)(a

g

t

− ¯a

g

), (20)

When the stock of bonds outstanding exceeds its steady state level, taxes are raised to pay

interest and a portion σ

τ

of the outstanding bonds. Given this fiscal feedback rule for taxes,

government debt then evolves according to (19).

3.5 Equilibrium

We can now define a linearized perfect-foresight transition equilibrium in this economy.

6

Definition 1. Given paths of exogenous shocks {m

t

, η

t

}

∞

t=0

, a linearized perfect foresight equi-

librium is a set of government policies {i

t

, τ

x,t

, τ

e,t

, a

g

t

}

∞

t=0

and a set of aggregates {c

t

, y

t

, a

t

, π

t

,

r

t

, q

b

t

, q

k

t

, w

t

, `

t

}

∞

t=0

such that:

1. The path of aggregate consumption {c

t

}

∞

t=0

is consistent with the linearized aggregate con-

sumption function (18), and the path of household asset holdings {a

t

}

∞

t=1

is consistent with

the budget constraint (8), aggregated across households. a

0

is determined by the existing

portfolios of households now valued at date-0 asset prices.

2. The real wage satisfies (10).

3. The paths {π

t

, y

t

, η

t

}

∞

t=0

are consistent with the Phillips curve (12).

6

All statements in Definition 1 thus refer to the linearized versions of the relevant model equations.

17

4. The paths of {`

t

, y

t

}

∞

t=0

satisfy the aggregate production function (13).

7

5. The asset returns {r

t

, q

b

t

, q

k

t

}

∞

t=0

satisfy (14), (15), and (16).

6. The evolution of government debt a

g

t

and the endogenous component of transfers τ

e,t

are

consistent with the budget constraint (19) and fiscal rule (20).

7. The output and asset markets clear, so y

t

= c

t

+ δk and (a

t+1

− a

g

t+1

)/(1 + r

t

) = q

k

t

k.

In this definition, the policy instrument paths {i

t

, τ

x,t

} are taken as given. Sections 4 and 5

will describe optimal policy problems and so discuss how these instruments are determined.

Equilibrium characterization. We can reduce Definition 1 to a small number of linear

relations. Lemma 1 provides this more compact characterization of equilibrium dynamics.

Lemma 1. Given paths of shocks {m

t

, η

t

}

∞

t=0

and government policy instruments {i

t

, τ

x,t

}

∞

t=0

,

paths of aggregate output and inflation {y

t

, π

t

}

∞

t=0

are part of a linearized equilibrium if and

only if

b

π

π

π = κ

b

y

y

y + β

b

π

π

π

+1

+ ψ

b

η

η

η, (21)

b

y

y

y =

˜

C

y

b

y

y

y +

˜

C

π

b

π

π

π +

˜

C

i

b

i

i

i +

˜

C

x

b

τ

τ

τ

x

+ C

m

b

m

m

m, (22)

where the linear maps {

˜

C

y

,

˜

C

π

,

˜

C

i

,

˜

C

x

} are defined in Appendix D.1, and

b

π

π

π

+1

= (π

1

, π

2

, . . . ).

Lemma 1 reduces the complexity of the equilibrium definition in Definition 1 to two

equations: the Phillips curve (21) (which is simply a stacked perfect-foresight version of the

original relation (12)); and the IS curve (22), which differs from the consumption function

(18) chiefly in that it imposes output market-clearing, asset revaluation effects, and feed-

back effects through the government budget to the endogenous component of transfers, τ

e,t

.

Together, these two equations fully characterize the evolution of output and inflation given

exogenous non-policy shocks {m

t

, η

t

}

∞

t=0

and policy choices {i

t

, τ

x,t

}

∞

t=0

.

Discussion. How does our model differ from the canonical representative agent New Key-

nesian models (Gal´ı, 2015; Woodford, 2003)? Positively, the main change is that a simple

7

Note that we drop the efficiency loss term d

t

since it is of second order, and thus does not affect a

first-order approximation of the production function around a zero inflation steady state (see Gal´ı, 2015).

Price dispersion will, however, affect the social welfare function in Section 5.

18

aggregate Euler equation,

by

t

= −

1

˜γ

(

b

i

t

− bπ

t+1

) + by

t+1

, (23)

is now replaced by the more general aggregate demand block (22).

8

Inequality thus affects

the aggregate dynamics of our economy in response to shocks and policy actions only through

the demand side, with supply—in particular the Phillips curve (21)—kept as in standard

representative-agent models. To arrive at this clean separation, our assumptions on union-

intermediated labor supply (see Section 3.2) are central. We adopt this approach because the

demand-side effects of household heterogeneity are the focus of the recent HANK literature

(e.g., see Kaplan et al., 2018; Auclert et al., 2018).

9

Normatively, household inequality may

affect social welfare functions and thus change policymaker objectives.

The remainder of the paper studies the implications of these two changes for optimal

policy design. First, in Section 4, we isolate the role of changes in propagation by studying a

dual-mandate optimal policy problem. Then, in Section 5, we turn to the Ramsey problem,

thus also allowing the planner objective to change.

4 Optimal dual-mandate policy

We begin our optimal policy analysis by studying the problem of a conventional dual-mandate

policymaker; that is, a policymaker that simply seeks to stabilize fluctuations in inflation and

the output gap. In the context of the structural model of Section 3, such a loss function is ad

hoc, but we nevertheless find it interesting, for two reasons. First, it is conceptually useful—

it allows us to split the effects of inequality on policy design into the role of propagation

(which we study here) and loss function (which we will study in Section 5). Second, it is

arguably policy relevant, as real-world central banks are often mandated to achieve these

types of simple objectives.

We begin in Section 4.1 by stating the optimal policy problem in linear-quadratic form.

We then in Section 4.2 characterize the problem’s solution in the form of a forecast target

criterion. Finally, in Section 4.3, we present some quantitative explorations, leveraging

in particular the connection between our optimal policy “sufficient statistic” formulas and

empirical evidence on the propagation of identified policy shocks.

8

Equation (23) combines the standard consumption Euler equation with EIS 1/γ with the log-linearized

aggregate resource constraint ˆc

t

= (¯c/¯y)ˆy

t

. The parameter ˜γ that appears in (23) is then γ¯c/¯y.

9

As an added benefit, our union structure with uniform labor rationing allows us to sidestep counterfactual

cross-sectional labor supply responses to policy interventions (see Auclert et al., 2020).

19

4.1 The optimal policy problem

We consider a policymaker with ad hoc objective function

L

DM

≡

∞

X

t=0

β

t

λ

π

bπ

2

t

+ λ

y

by

2

t

. (24)

(24) is a dual-mandate loss function: the policymaker wishes to stabilize inflation and output

around the deterministic steady state, with weights λ

π

and λ

y

, respectively.

For most of this section, we focus on the optimal setting of nominal interest rates i

t

, with

only brief reference to optimal stimulus check policy.

10

The policymaker sets nominal interest

rates to minimize (24) subject to the equilibrium constraints embedded in Definition 1. By

Lemma 1, we can reduce these two constraints to two simple relationships: the Phillips curve

(21) and the IS curve (22). This optimal policy problem is thus a minimal departure from

optimal policy analysis in conventional representative-agent environments: the loss function

(by assumption) and the supply side are unaffected, while the demand constraint changes

from a simple Euler equation as in (23) to the richer demand relation (22).

Note that so far the constraints of this policy problem take the form of our general linear

constraint (2). By the arguments in McKay & Wolf (2023), we can equivalently re-write this

constraint set in impulse response space, thus giving our alternative formulation (3).

11

For

future reference, we write the constraints in impulse response space as

b

π

π

π = Θ

π,i

b

i

i

i + Θ

π,x

b

τ

τ

τ

x

+ Θ

π,η

b

η

η

η + Θ

π,m

b

m

m

m, (25)

b

y

y

y = Θ

y,i

b

i

i

i + Θ

y,x

b

τ

τ

τ

x

+ Θ

y,η

b

η

η

η + Θ

y,m

b

m

m

m. (26)

Computational details. Solving the dual-mandate optimal policy problem is straight-

forward. Key to this computational simplicity is that the maps characterizing the linear-

quadratic problem—either the

˜

C’s in the original constraint formulation or the Θ’s in the

equivalent impulse response space formulation—can be obtained straightforwardly as a side-

product of standard sequence-space solution output, following the methods developed in

10

To be more precise, we study the optimal monetary policy problem of setting i

t

, with τ

x,t

= 0 in the

background. There are, of course, still effects of fiscal adjustments through the endogenous fiscal rule (20).

11

In McKay & Wolf (2023), we close the model with a determinacy-inducing policy rule for the policy

instruments, here i and τ

x

. The dynamic causal effect matrices in (25) - (26) are then defined as impulse

response matrices for shocks to the baseline rule. For example, if the inflation and interest rate impulse

response matrices to monetary shocks to the base rule are denoted

˜

Θ

π,i

and

˜

Θ

i,i

, then Θ

π,i

≡

˜

Θ

π,i

˜

Θ

−1

i,i

. By

the arguments of McKay & Wolf (2023) this re-writing is without loss of generality.

20

Auclert et al. (2021). It thus follows that optimal policy analysis in the dual-mandate case

comes at essentially zero additional computational cost: if a researcher can solve her HANK

model given a policy rule, then she is only a trivial linear-quadratic problem away from also

obtaining an optimal policy rule for a given quadratic loss.

4.2 Policy rule irrelevance

Our first main result is that, under mild regularity conditions on the linear map

˜

C

i

—i.e., the

mapping from nominal interest rate paths to net excess consumption demand in the gener-

alized “IS” curve (22)—, the optimal monetary policy forecast target criterion is completely

unaffected by household heterogeneity.

Proposition 1. Let

b

c

c

c be a path of household consumption with zero net present value, i.e.,

P

∞

t=0

1

1+¯r

t

bc

t

= 0. If, for any such path

b

c

c

c, we have that

b

c

c

c ∈ image(

˜

C

i

), (27)

then the optimal monetary policy rule for a dual-mandate policymaker with loss function (24)

can be written as the forecast target criterion

λ

π

bπ

t

+

λ

y

κ

(by

t

− by

t−1

) = 0, ∀t = 0, 1, . . . (28)

Recall that our expressions for general linear-quadratic policy problems derived in Sec-

tion 2 immediately yield the optimal dual-mandate policy target criterion as

λ

π

· Θ

0

π,i

·

b

π

π

π + λ

y

· Θ

0

y,i

·

b

y

y

y = 0

0

0. (29)

The proof of Proposition 1 leverages the structure of our model to turn the general expression

(29) into the simple rule (28). Intuitively, while (29) is written in terms of the absolute causal

effects of interest rate policy on output and inflation, (28) is the analogue in terms of relative

causal effects: if monetary policy moves inflation at date t by one unit, then it changes output

at t and t − 1 by

1

κ

and −β

1

κ

units, respectively. Since the policymaker herself discounts at

rate β, we find that the complicated relation (29) collapses to the simple one (28).

Importantly, the rule (28) is exactly the same as in conventional representative-agent

optimal policy analyses (Gal´ı, 2015; Woodford, 2003). The logic underlying this result is as

follows. In the familiar representative-agent policy problem, any desired path of output and

21

inflation that is consistent with the Phillips curve can be implemented through a suitable

choice of interest rates. The IS curve is thus a slack constraint: the policymaker picks the best

output-inflation pair subject to the NKPC, and then sets interest rates residually to deliver

the required time path of demand. Condition (27) is precisely enough to ensure that this logic

carries through in our environment with household heterogeneity. In words, the condition

says that, through manipulation of short-term nominal interest rates, the policymaker can

engineer any possible net excess demand path with zero net present value. The proof of

Proposition 1 reveals that this is sufficient to ensure that any desired output-inflation pair

consistent with the Phillips curve (21) is in fact implementable. But then, with the Phillips

curve as the supply side of the economy not depending on household inequality, we find that

the target criterion is the same as in conventional representative-agent models.

The implementability condition (27) is discussed further in Wolf (2021). That paper

shows—analytically in simple models, and numerically in heterogeneous-agent environments—

that interest rate policies are indeed generally flexible enough to induce every possible zero

net present value path of aggregate net excess demand. The irrelevance of household hetero-

geneity for optimal forecast criteria is thus a robust feature of HANK-type environments.

Implications for monetary policy practice. The upshot of Proposition 1 is that,

independently of the non-policy shocks hitting the economy, under optimal dual-mandate

policy, the equilibrium paths of output and inflation will be unaffected by household het-

erogeneity and thus equal to those in a standard representative-agent economy. The only

possible effect of heterogeneity is to change the instrument paths—i.e., the current and fu-

ture values of nominal interest rates—required to attain those desired output and inflation

paths. We conclude that the positive implications of household heterogeneity have a rather

limited effect on the practice of conventional dual-mandate policymakers: they can continue

to set their instruments to bring projections of macroeconomic outcomes in line with target,

exactly as done in standard practice of flexible inflation targeting.

12

Optimal stimulus checks. Proposition 1 only considers the first instrument available to

our policymaker: nominal interest rates. Results for stimulus checks follow immediately from

12

Bernanke (2015) succinctly summarizes the salience of this perspective for Federal Reserve policymaking

practice: “The Fed has a rule. The Fed’s rule is that we will go for a 2 percent inflation rate. We will go for

the natural rate of unemployment. We put equal weight on those two things. We will give you information

about our projections about our interest rates. That is a rule and that is a framework that should clarify

exactly what the Fed is doing.”

22

Wolf (2021), who identifies conditions under which interest rate and stimulus check policies

can implement the same sequences of aggregate output and inflation. More formally, it

follows from his results that, if

b

c

c

c ∈ image(

˜

C

τ

) (30)

for all sequences

b

c

c

c with zero net present value, then stimulus check policies can also im-

plement the target criterion (28), just like conventional monetary policy. This alternative

implementability condition (30) is again generally satisfied in HANK-type environments.

It follows from the previous discussion that the two policy instruments are perfect sub-

stitutes, and so that the solution to the problem of choosing both instruments to minimize

(24) is indeterminate—multiple paths of the two policy instruments are consistent with the

optimal outcomes for output and inflation. One way to break this indeterminacy is to in-

troduce further constraints on instruments, e.g. a lower bound on nominal interest rates.

Section 5 considers an alternative resolution to this indeterminacy: a richer loss function.

4.3 Quantitative analysis & connection to empirical evidence

We have seen that household heterogeneity does not affect the optimal inflation and output

gap outcomes implemented by a dual-mandate policymaker. Heterogeneity could, however,

in principle affect the time paths of nominal rates required to achieve those optimal outcomes.

This section leverages the close connection between our “sufficient statistics” characterization

of optimal policy and empirical evidence on policy shock propagation to further argue that,

in quantitatively relevant models, the effects of household heterogeneity on optimal rate paths

are likely to be modest in scope.

Exact instrument path irrelevance. We begin with another exact irrelevance result,

building closely on McKay & Wolf (2023). For this result, it will prove convenient to re-state

(5) for the optimal policy instrument path, here specialized to the policy instrument i and

for the policy targets x = (y, π)

0

, in response to some generic set of shocks ε

ε

ε:

b

i

i

i

∗

≡ −

Θ

0

x,i

(Λ ⊗ W )Θ

x,i

−1

×

Θ

0

x,i

(Λ ⊗ W )Θ

x,ε

· ε

ε

ε

. (31)

Equation (31) states that we can recover the interest rate path required to implement the

optimal policy rule (28) from the absolute causal effects of interest rate policy on output and

inflation. It thus has the following important implication. Any two models—say HANK and

RANK—that agree on (i) the effects of a given shock ε

ε

ε on output and inflation, Θ

y,ε

· ε

ε

ε and

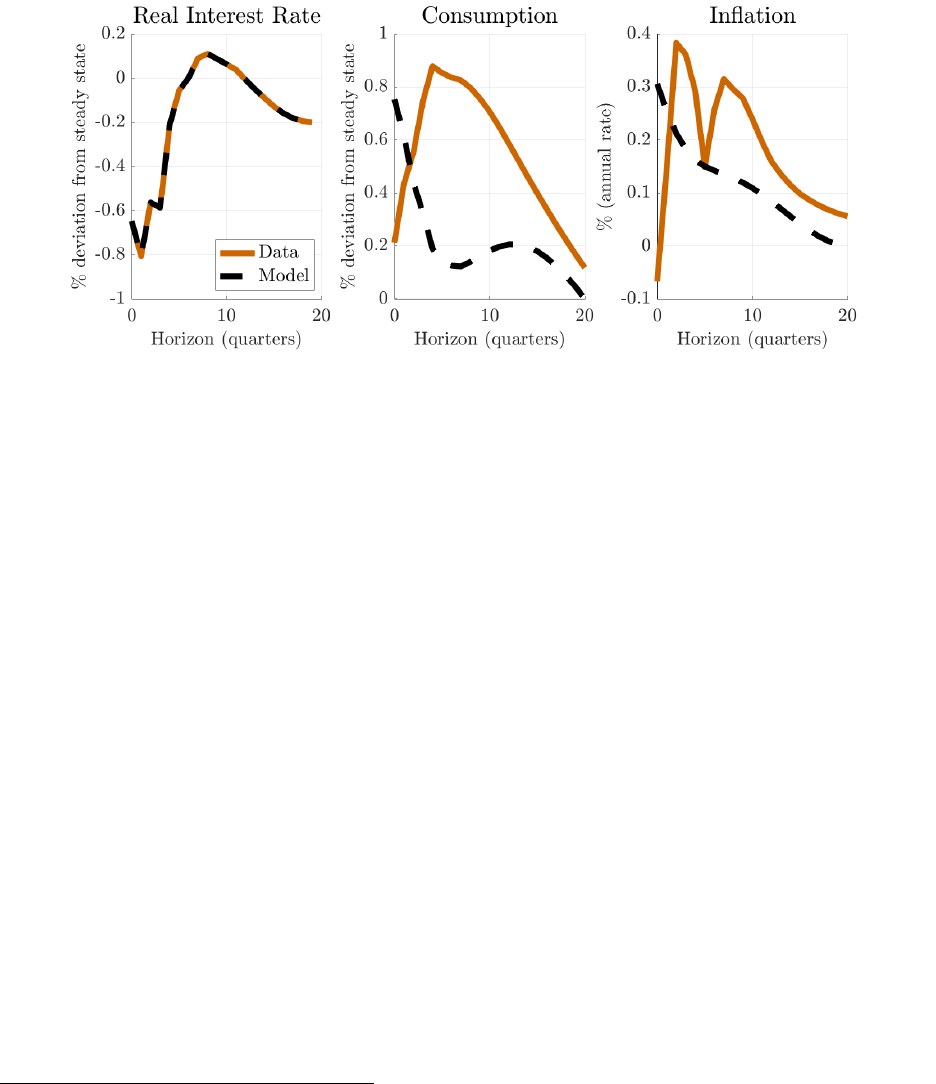

23

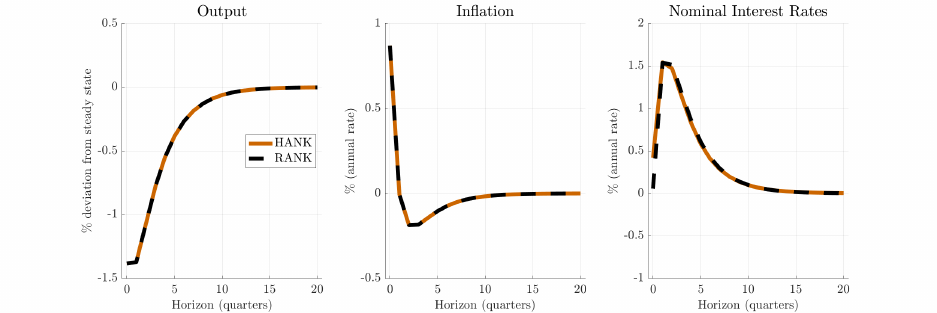

Figure 1: Optimal dual-mandate policy response to a cost-push shock. The RANK model replaces

our general “IS” curve (22) with the simple textbook Euler equation (23). We then calibrate all

parameters as in the headline HANK model (see Section 5.3), with one exception: we set the

elasticity of intertemporal substitution (EIS) to generate the same peak response of output to an

identified monetary shock as in the HANK model. In practice, the EIS is little changed.

Θ

π,ε

· ε

ε

ε, and (ii) the effects of interest rate changes on output and inflation, Θ

y,i

and Θ

π,i

,

will necessarily agree on the optimal interest rate path

b

i

i

i

∗

.

We view this irrelevance result as informative because its ingredients are measurable. In

particular, the dynamic causal effects of interest rate changes on aggregate outcomes—that

is, elements of Θ

y,i

and Θ

π,i

—are the estimands of a large empirical literature on monetary

policy shocks (Ramey, 2016). Structural models are often calibrated or estimated to be

consistent with estimates from this literature, which leads them to approximately agree for

the entire matrices Θ

y,i

and Θ

π,i

. The degree to which such quantitative models can disagree

on optimal dual-mandate interest rate paths is thus limited by the empirical evidence.

Quantitative illustration. We close with a quantitative illustration of the analytical

results presented so far. To this end, we study optimal dual-mandate monetary policy in

response to a cost-push shock η

t

in a calibrated version of our HANK model. Details of the

calibration are postponed until Section 5.3; for purposes of the discussion here, it suffices

to note that the model has been parameterized to in particular be consistent with empirical

evidence on the output gap and inflation effects of monetary policy shocks. We then contrast

aggregate outcomes in this economy with those in an analogous RANK model, calibrated

similarly to be consistent with empirical policy shock evidence.

Results are displayed in Figure 1. We emphasize the following two main takeaways, both

consistent with our analytical discussion in the earlier parts of this section. First, as shown

24

in Proposition 1, the output gap and inflation paths are exactly the same. The optimal

trade-off between inflation and output is fully governed by the Phillips curve, which itself

is not affected by household inequality. Second, the nominal interest rate path required to

implement the optimal outcome is quite similar across the two models. Intuitively, since by

construction both models match the same evidence on the transmission from interest rate

changes to output and inflation, the interest rate movements that achieve the policymaker’s

desired output and inflation responses to the shock cannot be too dissimilar.

13

5 Optimal Ramsey policy

We now turn to the optimal policy problem of a Ramsey planner. Unlike our ad hoc dual-

mandate loss function of Section 4, this planner’s objective is directly affected by household

inequality, reflecting a desire to dampen the distributional consequences of aggregate shocks.

Most of our analysis in this section again focuses on optimal monetary policy.

The remainder of the section proceeds in three steps. First, in Section 5.1, we show how

to express the optimal policy problem in our linear-quadratic form. Second, in Section 5.2

we present general analytical results and discuss some instructive analytical special cases.

Finally, in Sections 5.3 and 5.4, we turn to quantitative analysis, leveraging our analytical

“sufficient statistics” formulas to connect to empirical evidence to compare our findings with

those of prior work.

5.1 The optimal policy problem

We consider a conventional Ramsey planner that aggregates utilities of the households pop-

ulating the economy. This section presents a linear-quadratic version of this policy problem.

As is typical in the optimal policy literature (e.g. see the discussion in Giannoni & Wood-

ford, 2002), doing so requires efficiency of the steady state. In the representative agent

context, efficiency requires that the level of production is optimal. Here we also require that

the planner finds the steady-state cross-sectional distribution of consumption desirable. Our

optimal policy analysis will therefore capture an insurance motive against fluctuations in

consumption shares, but it will not seek to change the long-run distribution of consumption.

13

As discussed above, the two interest rate paths would agree exactly if the two models were to agree

on all of Θ

y,i

and Θ

π,i

. Our calibration instead only ensures that peak output and inflation responses in

response to a particular, transitory interest rate movement align. This materially limits the extent of—but

does not fully eliminate—possible disagreement in nominal rate paths.

25

Loss function. To state the loss function, it will prove convenient to describe an individ-

ual’s outcomes in terms of their history of idiosyncratic shocks; that is, we replace c

it

with

ω

t

(ζ

t

i

)c

t

where ζ

t

i

≡ (ζ

it

, ζ

it−1

, ζ

it−2

, · · · ) is individual i’s history of idiosyncratic shocks and

ω

t

(ζ

t

i

) ≡ c

it

/c

t

is their share of aggregate consumption.

14

Letting Γ(ζ) denote the (station-

ary) distribution of such histories (with ζ denoting a generic realization of a history), we can

write the social welfare function as

V

HA

=

∞

X

t=0

β

t

Z

ϕ(ζ)

"

(ω

t

(ζ)c

t

)

1−γ

− 1

1 − γ

− ν (`

t

)

#

dΓ(ζ), (32)

where ϕ(ζ) is a Pareto weight on the utility of households with history ζ.

In keeping with optimal (monetary) policy analysis in standard representative-agent en-

vironments (Woodford, 2003), our objective is to evaluate the social welfare function (32)

to second order. To this end, a first-order approximation to aggregate equilibrium dynamics

suffices only if the expansion point (i.e., the deterministic steady state) is efficient. Without

household heterogeneity, a simple production subsidy is sufficient to ensure this. With house-

hold heterogeneity, however, we now also require the consumption shares of all households

to be optimal. In principle there are two ways of ensuring this: either the steady-state fiscal

tax-and-transfer system achieves the optimal level of insurance given the planner weights

ϕ(•), or the planner weights are set residually so that the implied steady-state distribution

of consumption given a tax-and-transfer system is optimal. We adopt the second approach,

following the inverse optimal taxation literature (e.g. Heathcote & Tsujiyama, 2021). Our

preference for this approach reflects the overarching focus of this paper: we ask how cyclical

policy tools should be manipulated to respond to cyclical changes in inequality, leaving the

long-run steady state outside of the purview of our analysis.

Appendix D.3 presents our assumptions on the production subsidy and policymaker pref-

erence weights that ensure efficiency of the deterministic steady state. Given those assump-

tions, a second-order approximation of (32) around the efficient steady state then gives the

following characterization of the policymaker loss function.

Proposition 2. To second order, the social welfare function V

HA

is proportional to −L

HA

,

given by

L

HA

≡

∞

X

t=0

β

t

bπ

2

t

+

˜κ

¯η

by

2

t

+ λ

ω

Z

bω

t

(ζ)

2

¯ω(ζ)

dΓ(ζ)

, (33)

14

Note that this is without loss of generality, as individuals in our model are ex ante identical, so their

outcomes only differ due to different histories of shocks.

26

where bω

t

(ζ) = ω

t

(ζ) − ¯ω(ζ) and ¯ω(ζ) is the steady-state consumption share of an individual

with history ζ and ˜κ and λ

ω

are composite parameters defined in Appendix D.3.

Note that, in the representative-agent analogue of our economy (as discussed in Sec-

tion 3.5), the loss function would feature the same first two terms, as already well-known

from prior work (Woodford, 2003).

15

Our analysis reveals that household heterogeneity adds

a third, inequality-related term, with the planner wishing to stabilize the consumption shares

of everyone in the economy.

How does the inequality term in (33) fit into the linear quadratic framework in Section 2?

Moving to a sequence-space formulation, we can write the loss as

L

HA

= λ

π

b

π

π

π

0

W

b

π

π

π + λ

y

b

y

y

y

0

W

b

y

y

y +

Z

λ

ζ

b

ω

ω

ω(ζ)

0

W

b

ω

ω

ω(ζ)dΓ(ζ), (34)

where λ

π

= 1, λ

y

=

˜κ

¯η

, and λ

ζ

≡ λ

ω

/¯ω(ζ). The consumption share for each idiosyncratic

household history thus emerges as a separate target variable for the policymaker. We will

discuss our approach to computation of (34) later in this section.

16

Constraints. The constraints of the optimal policy problem characterize the evolution

of policymaker targets—π, y, and the consumption shares ω(ζ)—as a function of exogenous

shocks and policy choices. As we discussed in Section 4.1, the evolution of aggregate output