Unconventional Monetary Policy According to HANK

Eric Sims

Notre Dame and NBER

Jing Cynthia Wu

Notre Dame and NBER

Ji Zhang

Tsinghua PBCSF

Current draft: August 20, 2022

Abstract

This paper studies the implications of household heterogeneity for the effective-

ness of quantitative easing (QE). We consider a heterogeneous agent New Keynesian

(HANK) model with uninsurable household income risk. Financial intermediaries are

subject to an endogenous leverage constraint that allows QE to matter. We find that

macro aggregates react very similarly to a QE shock in the HANK model compared

to a representative agent (RANK) version of the model. This finding is robust across

different micro- and macro- distributions of wealth.

We are grateful to Drew Creal, Soroush Ghazi, Jasmine Xiao, as well as seminar and conference

participants at NBER Summer Institute Monetary Economics Meeting, Penn State University, Tsinghua

University, the University of Alabama, 2022 Renmin University of China School of Finance Workshop,

and Marquette University for helpful comments. Sims and Wu acknowledge support from the National

Science Foundation under Grant No. SES-1949107. Ji acknowledges support from the National Natu-

ral Science Foundation of China (No.72003102). Correspondence: [email protected], [email protected],

1 Introduction

In response to the Great Recession, the Federal Reserve (Fed) lowered its short-term pol-

icy rate to zero. With its conventional stabilization tool unavailable, the Fed resorted to

unconventional policy to provide support to the US economy. The most prominent of its

unconventional policy tools was quantitative easing (QE, also referred to as large scale as-

set purchases, or LSAPs). Purchasing longer-term Treasuries and agency mortgage-backed

securities (MBSs), the Fed more than doubled its balance sheet within the span of a few

months in late 2008. By the time it halted active asset purchases in the middle part of the

2010s, the Fed’s balance sheet had quintupled in size relative to its pre-Great Recession level.

The Fed resumed active asset purchases in 2020 in response to the COVID-19 pandemic,

doubling the size of its balance sheet in less than two years.

There is a large and still growing literature on the effectiveness of QE. Most theoretical

work in this literature is based on representative agent New Keynesian (RANK) models –

see, for example, Gertler and Karadi (2013), Sims and Wu (2020, 2021a), and Sims, Wu

and Zhang (forthcoming). At the same time, there has been significant interest in the

implications of micro-level heterogeneity for macroeconomic fluctuations in general, and in

particular with respect to the transmission of monetary policy; i.e., the heterogeneous agent

New Keynesian (HANK) literature (e.g. Kaplan, Moll and Violante 2018, McKay et al.

2016, Auclert 2019, Acharya and Dogra 2020, Alves, Kaplan, Moll and Violante 2020, Ravn

and Sterk 2020, and others). To date, however, this literature has mainly considered the

implications of heterogeneity for conventional monetary policy in the form of movements in

short-term interest rates. The goal of our paper is to marry these two literatures to investigate

whether, and to what extent, household heterogeneity matters for the effectiveness of QE.

1

1

The one exception of which we are aware is Cui and Sterk (2021). However, the underlying frictions for

QE to matter differ in the two papers. Our paper follows the QE literature and features frictions on financial

intermediaries. QE transmits through intermediaries and impacts the real economy via investment. In

contrast, Cui and Sterk (2021) follow more closely the HANK literature, with two types of assets households

can hold. The main mechanism through which QE works in their model is through household marginal

propensities to consume out of two types of assets, not via intermediaries or through firm investment.

2

We develop a quantitative general equilibrium model with household heterogeneity and

scope for QE to matter. Households face uninsurable idiosyncratic unemployment ris and

endogenously supply labor. They may save via short-term deposits with financial interme-

diaries, subject to a borrowing constraint, and receive dividends from their ownership in

production firms and financial intermediaries. Financial intermediaries engage in maturity

transformation, standing between households who save via short-term deposits, and produc-

tion firms who float long-term debt to finance investment. Financial intermediaries face an

endogenous leverage constraint, and production firms are required to finance a fraction of

their investment by issuing long-term bonds. Prices and nominal wages are sticky. Central

bank purchases of long-term assets can ease the leverage constraint facing intermediaries,

resulting in lower interest rate spreads and more investment. We refer to an exogenous

increase in central bank long-term asset holdings as a QE shock.

In our benchmark specification, we assume that all households receive the same dividend

payout each period. The responses of aggregate variables to a QE shock are nearly identical to

a representative agent (RANK) version of the model, even though the HANK version features

substantial wealth inequality due to uninsurable employment risk and a borrowing constraint.

The only noticeable difference is the consumption response of the very poorest households

in the HANK version, which increases sharply after a QE shock. But this distributional

difference has little impact on aggregate variables.

We consider robustness of our results with respect to both the micro- and macro- distri-

butions of wealth. First, regarding the micro distribution, we allow a more general dividend

distribution rule, in which dividends vary, potentially non-linearly, with household wealth.

We explore the implications of this distribution rule for popular inequality metrics, such

as the Lorenz Curve and the Gini Coefficient. With a significant gap between dividends

received by the richest and poorest households, and sufficient non-linearity in the relation-

ship between dividend receipt and wealth, our model can generate more wealth inequality

compared to our benchmark specification. However, different degrees of micro-level wealth

3

inequality matter little for aggregate dynamics. Regardless of how we specify the dividend

distribution rule, we find that the impulse responses of aggregate variables to a QE shock

are remarkably similar, and in turn almost identical to a RANK version of the model.

Next, we investigate the extent to which macro parameterizations related to the wealth

distribution influence the aggregate transmission of QE shocks. When we parameterize

the model so that a higher fraction of the population is unemployed in each period, many

more households are located at or near the borrowing constraint compared to our baseline

specification. This results in the aggregate effects of a QE shock being slightly bigger.

These differences are nevertheless not economically large, and are only visibly noticeable for

very high unemployment rates. We then investigate whether the duration of unemployment

spells matters for the aggregate transmission of QE shocks and find it is almost completely

irrelevant. We also examine the role of the unemployment benefit paid out to unemployed

households. Smaller or larger values of this parameter have modest implications for the

stationary wealth distribution, but matter little for the aggregate effects of QE. Finally, we

study the sensitivity of our results to households’ risk aversion. This parameter has little

effect on how QE impacts the economy.

There are two potentially important takeaways from our quantitative exercises. The

first is that there seems to be little gained by formally modeling household heterogeneity

if one is interested in is the aggregate effects of a QE shock. Our finding that RANK is a

good approximation to a substantially more complicated and numerically more demanding

HANK model is consistent with a recent paper by Debortoli and Gali (2022), who argue

that idiosyncratic income uncertainty is unimportant for aggregate fluctuations. Another

important takeaway from our analysis is that there seems to be little connection between

various inequality metrics and aggregate dynamics in response to a QE shock. Much of

the existing literature uses moments such as the Gini coefficient as summary statistics for

inequality. To the extent to which one is only interested in aggregate dynamics, our results

suggest that this focus on inequality metrics might be misplaced.

4

In addition to these substantive issues, our paper also makes a methodological con-

tribution. Though our model features idiosyncratic income risk, wealth inequality, and a

borrowing constraint, we are able to solve the model using perturbation methods in Dynare,

a popular program for solving, simulating, and estimating RANK models. Our paper is sim-

ilar in this respect to Winberry (2018), who also solves a heterogeneous agent model with

perturbation methods in Dynare. Substantively, our model features nominal rigidities and

other frictions common in the New Keynesian literature, whereas his model fits into a real

business cycle framework. Methodologically, we depart from him in that we follow Young

(2010) to approximate the cross-sectional distribution with a non-parametric histogram,

whereas Winberry (2018) follows Algan et al. (2008) to approximate this distribution within

a parameteric family. The advantage of our approach is that it does not involve numerical

optimization, which slows the calculation when done repeatedly and does not guarantee con-

vergence. Our method is not limited to the QE application on which we focus in this paper,

nor is it specific to the exact form of household heterogeneity.

The remainder of the paper is organized as follows. Section 2 lays out our model. Section 3

discusses our method for solving the model. Section 4 compares and contrasts impulse

responses to an exogenous QE shock with and without household heterogeneity. Section 5

discuss our model’s implications for popular inequality metrics and considers a more general

form of the dividend distribution rule to study how that affects the aggregate dynamics in

response to a QE shock. Section 6 considers changing macro parameters and investigates

the extent to which they matter for aggregate dynamics in response to a QE shock. The

final section concludes.

2 Model

Our model features financial frictions, a banking sector, and has scope for central bank

asset purchases to matter. In addition, households are heterogeneous and face uninsurable

5

unemployment risk. In this section,we provide detail on key elements of the model and

relegate remaining details to Appendix A.

2.1 Households

The household sector is similar to Krusell and Smith (1998), except that labor supply is

endogenous. There are a continuum of households indexed by j ∈ [0, 1]. Each maximizes

the present discounted value of lifetime flow utility:

E

0

∞

X

t=0

β

t

log c

j,t

− χ

l

1+η

j,t

1 + η

!

, (2.1)

where c

j,t

and l

j,t

are an individual household’s consumption and labor supply. β ∈ (0, 1) is

a discount factor, χ > 0 is a scaling parameter, and η is the inverse Frisch elasticity.

Each household faces an exogenous idiosyncratic labor productivity shock, ε

j,t

∈ {0, 1}.

This productivity shock can be interpreted as an employment shock, where ε

j,t

= 0 indicates

unemployed and consequently l

j,t

= 0, while ε

j,t

= 1 means that the household will earn

a positive market wage and will hence choose to work, l

j,t

> 0. ε

j,t

evolves stochastically

according to a two-state Markov process with the transition matrix

p(ε

j,t+1

= 0|ε

jt

= 0) p(ε

j,t+1

= 1|ε

jt

= 0)

p(ε

j,t+1

= 0|ε

jt

= 1) p(ε

j,t+1

= 1|ε

jt

= 1)

=

p 1 − p

U

1−U

(1 − p) 1 −

U

1−U

(1 − p)

. (2.2)

The aggregate unemployment rate is U = p(ε

j,t

= 0) and is fixed. Total labor supply is

L

t

=

R

1

0

l

j,t

dj.

Household j saves via deposits, d

j,t

, with financial intermediaries, which earn the gross

interest rate, R

d

t

, from t to t + 1. Deposits are the only asset the household can accumulate.

A household faces the following flow budget constraint:

6

d

j,t

=

R

d

t−1

Π

t

d

j,t−1

+ mrs

t

[(1 − τ)l

j,t

ε

j,t

+ µ(1 − ε

j,t

)] − c

j,t

− T

t

+ div

j,t

− X, (2.3)

where Π

t

is the gross inflation rate, mrs

t

is the real wage, τ is a tax rate on labor income,

µ × mrs

t

is an unemployment benefit, T

t

is a lump-sum tax, and X is a real transfer paid

out to new financial intermediaries, to be discussed below. div

j,t

is a dividend transfer from

all firms. This dividend is taken as given by households; we will discuss how it is distributed

across agents in Section 4 and Section 5. d

j,t

, c

j,t

,and l

j,t

are endogenous choice variables.

Each household faces a borrowing constraint and a constraint on its time endowment:

d

j,t

≥ d (2.4)

l

j,t

≤

¯

l. (2.5)

The first order conditions are

c

−1

j,t

≥ βR

d

t

E

t

c

−1

j,t+1

Π

t+1

(2.6)

l

η

j,t

≤

(1 − τ)mrs

t

χc

j,t

. (2.7)

The equalities hold when the constraints in (2.4) and (2.5) do not bind.

2.2 Labor Market

We introduce wage rigidity into our model via labor unions. Unions are indexed by h ∈

[0, 1]. These unions purchase labor from households at real wage mrs

t

, repackage it into

L

d,t

(h), and sell it to a representative labor contractor at nominal wage, W

t

(h). The labor

contractor combines differentiated labor into final labor available for production, L

d,t

via a

CES technology. Final labor is sold to a representative production firm at nominal wage,

7

W

t

.

Unions are subject to a Calvo-style nominal rigidity. Each period, a union can adjust

its wage, W

t

(h), with probability 1 − ϕ

w

, where ϕ

w

∈ [0, 1]. Non-updated wages can be

indexed to lagged aggregate inflation via the parameter γ

w

∈ [0, 1]. This setup gives rise to

a conventional wage Phillips curve. See the Appendix for details.

2.3 Production

There are four different types of firms in our model. A representative capital goods producer

transforms raw investment goods into new physical capital subject to a convex adjustment

cost. A competitive final good producer aggregates retail output into final output via a

CES technology and sells it at nominal price, P

t

. A continuum of retail firms, indexed

by f ∈ [0, 1], repackage wholesale output and sell it to the final good producer at P

t

(h).

Retailers have market power and are subject to a Calvo-style nominal rigidity, updating

their prices with probability 1 − ϕ

p

each period. Non-updated prices can be indexed to

lagged inflation via the parameter γ

p

∈ [0, 1]. The representative wholesale firm accumulates

its own capital, purchases new capital from the capital goods producer, and hires labor from

the labor contractor. It produces wholesale output, Y

m,t

, from capital and labor, and sells

this output to retail firms at P

m,t

. The wholesale firm can choose the intensity with which

it utilizes physical capital, u

t

, the cost of which is faster depreciation.

With the exception of the wholesale firm, the production side of the model is reasonably

standard, and details are relegated to an appendix. The wholesale firm accumulates its own

physical capital, K

t

. It purchases new physical capital,

b

I

t

, from the capital goods producer

at nominal price P

k

t

. We require that the wholesale firm finance a fraction, ψ ∈ [0, 1], of

its purchases of new physical capital by issuing long-term bonds. As in Woodford (2001),

these long-term bonds take the form of perpetuities with decaying coupon payments. Let

κ ∈ [0, 1] denote the decay parameter for coupon payments. A bond in period t is sold for

Q

t

dollars and obligates the issuer to a coupon payment of one dollar in t + 1, κ dollars

8

in t + 2, κ

2

dollars in t + 3, and so on. The total nominal coupon liability due in t from

all past issuances is denoted by F

m,t−1

; new issuance of bonds in t is therefore denoted by

F

m,t

− κF

m,t−1

, which generates Q

t

dollars for the issuer. The “loan in advance” constraint

facing the wholesale firm is:

ψP

k

t

b

I

t

≤ Q

t

(F

m,t

− κF

m,t−1

). (2.8)

Equation (2.8) distorts standard first order conditions related to capital investment and bond

issuance. It therefore generates “investment” and “financial” wedges. Fluctuations in these

wedges are the mechanism through which QE-type policies transmit to the real economy.

2.4 Financial Intermediaries

Financial intermediaries are structured similarly to Gertler and Karadi (2011, 2013), and

Sims and Wu (2021a,b). Each period there is a fixed mass of intermediaries indexed by i.

Intermediaries finance themselves with net worth, N

i,t

, and deposits taken from households,

D

i,t

. Each period, a fraction 1 − σ, with σ ∈ [0, 1], stochastically exit and return their net

worth to their household owner. They are replaced by an equal number of new intermediaries

that begin with real start up funds of X given to them by their household owner.

Intermediaries hold privately issued bonds, F

i,t

; government issued nominal bonds, B

i,t

;

and interest-bearing reserves, RE

i,t

, which are held on account with the central bank. Gov-

ernment bonds are structured similarly to private long-term bonds and are priced at Q

B,t

.

The balance sheet condition of a typical intermediary is:

Q

t

F

i,t

+ Q

B,t

B

i,t

+ RE

i,t

= D

i,t

+ N

i,t

(2.9)

A financial intermediary accumulates net worth until stochastically exiting. Net worth

9

for surviving intermediaries evolves according to:

N

i,t

=

R

F

t

− R

d

t−1

Q

t−1

F

i,t−1

+

R

B

t

− R

d

t−1

Q

B,t−1

B

i,t−1

+

R

re

t−1

− R

d

t−1

RE

i,t−1

+R

d

t−1

N

i,t−1

(2.10)

R

re

t−1

is the (gross) interest rate on reserves, which is set by the central bank and known at

t−1. R

d

t−1

is the deposit rate, which is determined in equilibrium. (R

F

t

−R

d

t−1

), (R

B

t

−R

d

t−1

),

and (R

re

t−1

−R

d

t−1

) are, respectively, the excess returns from holding private bonds, government

bonds, and reserves relative to the cost of funding via deposits. The term R

d

t−1

N

i,t−1

measures

the cost-savings from financing via net worth as opposed to deposits. R

F

t

and R

B

t

are the

realized holding period returns on private and government bonds and satisfy:

R

F

t

=

1 + κQ

t

Q

t−1

(2.11)

R

B

t

=

1 + κQ

B,t

Q

B,t−1

(2.12)

The objective of an intermediary is to maximize its expected terminal net worth, where

discounting is by the stochastic discount factor for households who are not at the borrowing

constraint

2

Λ

t,t+1

=

Π

t+1

R

d

t

. (2.13)

Consider the problem of an intermediary continuing after period t. There is a 1 − σ

probability that it will exit after t + 1, a (1 − σ)σ probability that it will exit after t + 2, and

so on. Accordingly, its objective is

V

i,t

= max (1 − σ)E

t

∞

X

j=1

σ

j−1

Λ

t,t+j

n

i,t+j

, (2.14)

where n

i,t

= N

i,t

/P

t

is real net worth, with P

t

the price of final output.

2

Note that while consumption levels will differ for unconstrained households, since (2.6) will hold with

equality, they all have the same stochastic discount factor.

10

A financial intermediary faces a costly enforcement constraint as in Gertler and Karadi

(2011, 2013). A financial intermediary can choose to abscond with some assets at the end of a

period rather than continuing as an intermediary. If an intermediary does this, depositors can

recover a fraction of the intermediary’s assets, with the intermediary retaining the rest. For

depositors to be willing to lend to intermediaries, it must not be optimal for the intermediary

to divert funds in this way, which we refer to as going into bankruptcy. Accordingly:

V

i,t

≥ θ(Q

t

f

i,t

+ ∆Q

B,t

b

i,t

) (2.15)

In (2.15), the right hand side of the inequality represents the (real) funds that a financial

intermediary can keep should it choose to enter bankruptcy, while the left hand side is the

value of continuing as an intermediary.

3

Should it choose to divert, an intermediary can keep

a fraction of its private bonds, θ, and a fraction of government bonds, θ∆, where 0 ≤ ∆ ≤ 1.

We assume that the third type of asset held by intermediaries – reserves – is fully recoverable

by depositors in the event of bankruptcy.

All financial intermediaries will behave in the same way with identical optimality condi-

tions. These are

E

t

Λ

t,t+1

Ω

t+1

Π

−1

t+1

R

F

t+1

− R

d

t

=

λ

t

1 + λ

t

θ (2.16)

E

t

Λ

t,t+1

Ω

t+1

Π

−1

t+1

R

B

t+1

− R

d

t

=

λ

t

1 + λ

t

θ∆ (2.17)

E

t

Λ

t,t+1

Ω

t+1

Π

−1

t+1

R

re

t

− R

d

t

= 0, (2.18)

where

Ω

t

= 1 − σ + σθϕ

t

(2.19)

ϕ

t

=

1 + λ

t

θ

t

E

t

[Λ

t,t+1

Ω

t+1

Π

−1

t+1

]R

d

t

. (2.20)

3

f

i,t

= F

i,t

/P

t

and b

i,t

= B

i,t

/P

t

are real private and government bond holdings, respectively.

11

(2.16) - (2.18) are the key equilibrium conditions. λ

t

≥ 0 is the multiplier on the costly

enforcement constraint. If this constraint does not bind, then to first order expected returns

on all three types of assets must equal the cost of funds (i.e. the deposit rate). If the costly

enforcement constraint binds, then there will be excess returns of long-term private and

public bonds over the deposit rate. Because reserves are fully recoverable in the event of

liquidation, arbitrage requires that the interest rate on deposits equal the interest rate on

reserves. (2.19) is an auxiliary variable introduced to simplify the analysis.

The value of an intermediary satisfies

V

i,t

= θϕ

t

n

i,t

. (2.21)

When the constraint in (2.15) binds,

ϕ

t

=

Q

t

f

i,t

+ ∆Q

B,t

b

i,t

n

i,t

, (2.22)

which is an endogenous leverage ratio, whose equilibrium condition is in (2.20). The con-

straint makes the financial intermediary less levered than it would find optimal. This en-

dogenous leverage constraint is ultimately what can give rise to excess returns.

One can show from (2.20) that:

θϕ

t

≥ 1 + λ

t

(2.23)

If (2.15) does not bind, then λ

t+j

= 0 for all j, which implies that θ

t

ϕ

t

= 1.

4

Intuitively,

this means that net worth is as valuable to a household as to an intermediary. In this case,

returns on all assets would be equal. Hence, whether an intermediary invests in F

i,t

, D

i,t

or

RE

i,t

would be irrelevant. When the costly enforcement constraint binds, then λ

t

> 0 and

θϕ

t

is larger than one. In this case, there exist excess returns on holding long-term assets

4

In this circumstance, Ω

t

= 1.

12

(private and government bonds).

2.5 Fiscal authority

A fiscal authority finances its expenditure by levying lump sum taxes and a labor income tax

on households, from receipt of a transfer, T

cb,t

, from the central bank, and by issuing long-

term bonds. Its expenditure includes purchases of output, G

t

, and unemployment benefits.

For simplicity, we assume that the government has a fixed real stock of long-term bonds

issued,

¯

b

G

. The government’s budget constraint is:

G

t

+ Π

−1

t

¯

b

G

+ mrs

t

µU = T

t

+ T

cb,t

+ Q

B,t

¯

b

G

(1 − κΠ

−1

t

) + τmrs

t

L

t

(2.24)

2.6 Monetary policy

The central bank controls the interest on reserves R

re

t

, which evolves according to a Taylor

(1993)-type interest rate rule:

ln R

re

t

= (1 − ρ

r

) ln R

re

+ ρ

r

ln R

re

t−1

+

(1 − ρ

r

) [ϕ

π

(ln Π

t

− ln Π) + ϕ

y

(ln Y

t

− ln Y

t−1

)] + σ

r

ϵ

r,t

, (2.25)

where 0 ≤ ρ

r

< 1, ϕ

π

> 1, and ϕ

y

≥ 0. ϵ

r,t

is a policy shock. We do not formally analyze

the implications of the ZLB in our analysis, but it would be straightforward to do so.

In addition to setting the interest rate on reserves, the central bank can buy and sell long-

term bonds (either privately issued bonds or government bonds). It finances these holdings

via reserves, which are held in the banking system. The central bank’s balance sheet, in

nominal terms, is:

Q

t

F

cb,t

+ Q

B,t

B

cb,t

= RE

t

(2.26)

13

The central bank’s remittance to the fiscal authority amounts to

T

cb,t

= (1 + κQ

t

) Π

−1

t

f

cb,t−1

+ (1 + κQ

B,t

) Π

−1

t

b

cb,t−1

− R

re

t−1

Π

−1

t

re

t−1

(2.27)

We model a QE shock as an exogenous and persistent change in central bank bond

holdings. In particular, we assume that real central bank holdings of privately issued bonds,

f

cb,t

, follow a stationary AR(1) process (and similarly for holdings of real government bonds,

b

cb,t

):

ln f

cb,t

= (1 − ρ

f

)f

cb

+ ρ

f

ln f

cb,t−1

+ σ

f

ϵ

f,t

, (2.28)

where 0 ≤ ρ

f

< 1 and f

cb

denotes steady state real bond holdings.

If financial intermediaries are unconstrained (i.e. (2.15) does not bind), then fluctuations

in central bank bond holdings are irrelevant. But if intermediaries are constrained, then

increases in central bank bond holdings ease the endogenous leverage constraint, resulting in

higher long-term bond prices (equivalently, lower long-term yields). This filters through to

the real economy by relaxing the loan in advance constraint on wholesale producers, leading

to more investment and higher aggregate demand.

3 Solution Method and Calibration

In this section, we outline our solution method and discuss the parameterization of our

model.

3.1 Solution Method

We solve our model using perturbation methods with the popular software Dynare. Com-

pared to a global solution, perturbation methods can accommodate a large number of state

variables and require less computational time. Though it is standard practice to solve a

14

RANK model using Dynare, it is not straightforward to do so when there is household

heterogeneity.

Solving the aggregate part of the model via Dynare is straightforward. The key step

we take is to map the equilibrium conditions of individuals’ policy functions and the cross-

sectional distribution into Dynare. We approximate the conditional expectation, the right-

hand side of (2.6), using Chebyshev polynomials (see, for example, Judd 1998):

5

βR

d

t

E

t

c

−1

t+1

Π

t+1

≡ T(d

t−1

, ε

t

) ≈ exp

(

N

X

n=0

θ

n,t

(ε

t

)T

n

(ξ(d

t−1

))

)

(3.1)

where T

n

are Chebyshev polynomials and θ

n,t

are loadings. T(d

t−1

, ε

t

) gives the inverse of

consumption in period t if the borrowing constraint does not bind. We then solve for the

policy function for deposits, labor, and consumption as follows:

d

t

= max

(

R

d

t−1

Π

t

d

t−1

+ mrs

t

[(1 − τ )l

t

ε

t

+ µ(1 − ε

t

)] − T(d

t−1

, ε

t

)

−1

− T

t

+ div

t

− X, d

)

(3.2)

l

t

= min

(

(1 − τ )mrs

t

χc

t

1

η

,

¯

l

)

(3.3)

c

t

=

R

d

t−1

Π

t

d

t−1

+ mrs

t

[(1 − τ )l

t

ε

t

+ µ(1 − ε

t

)] − d

t

− T

t

+ div

t

− X (3.4)

Iterating the policy functions one period forward, we can further express c

t+1

as a function

of T(d

t

, ε

t+1

) and hence θ

n,t+1

. Therefore, (3.1) becomes the dynamic equation for θ

n,t

. For

details, see Appendix B.

Next, we update the cross-sectional distribution from t to t+1. We use the non-parametric

method proposed by Young (2010) by approximating the joint distribution p(d

t

, ε

t+1

) with

a histogram over the grid {d

m

}

M

m=0

and ε

t+1

= {0, 1}. The transition dynamics for the

cross-sectional distribution are given by:

p(d

t

, ε

t+1

) =

X

ε

t

X

d

t−1

p(d

t

|d

t−1

, ε

t

)p(ε

t+1

|ε

t

)p(d

t−1

, ε

t

), (3.5)

5

For brevity, we drop j subscript hereafter.

15

where p(ε

t+1

|ε

t

) is given in (2.2).

We know d

t

(d

t−1

, ε

t

) from the policy function. However, even with d

t−1

on a discrete

grid, d

t

does not necessarily fall on a grid point. We follow Young (2010) and approximate

p(d

t

|d

t−1

, ε

t

) with the d

m

grid: find the two neighboring grids d

m

′

, d

m

′

+1

that are closest to

d

t

, where m

′

= 0, ...., M − 1. Assign weights to them using

p(d

t

= d

m

′

|d

t−1

= d

m

, ε

t

) = 1 −

d

t

− d

m

′

d

m

′

+1

− d

m

′

p(d

t

= d

m

′

+1

|d

t−1

= d

m

, ε

t

) =

d

t

− d

m

′

d

m

′

+1

− d

m

′

. (3.6)

With the transition probabilities in (3.6) and (2.2), (3.5) characterizes the dynamics equa-

tions for the joint probability p(d

t

, ε

t+1

). See Appendix C for the full set of equilibrium

conditions that we feed into Dynare.

For the stationary equilibrium without aggregate shocks, we solve a fixed-point problem

over aggregate deposits, d, and labor supply, L (aggregate consumption is then determined

given the resource constraint). We proceed in steps. First, given guesses of d and L, we

can compute stationary equilibrium values of all aggregate variables. Then we solve for the

stationary equilibrium values of the Chebyshev coefficients; this step is also a fixed point

problem. Third, we solve the stationary distribution p(d, ε) by iterating (3.5) forward on

the discretized grid until convergence. Once we have the distribution from this step and

the policy functions from the Chebyshev step, we can compute updated values of aggregate

deposits,

e

d, and labor,

e

L. We then iterate over these steps until d ≈

e

d and L ≈

e

L. For

details of solving the stationary equilibrium, see Appendix D.

Our solution method is related to Winberry (2018). He also proposes a methodology

to solve a model with heterogeneous agents in Dynare. The main difference relative to our

approach is that he approximates the cross-sectional distribution following Algan, Allais and

Haan (2008), who use a parametric family. This methodology requires a large number of

numerical optimizations when solving the stationary equilibrium. The optimization routines

16

do not guarantee convergence and the computational burden is high. The numerical behavior

of their approach becomes problematic when the distribution is far away from a normal

distribution, which is the case for our application.

We, instead, follow Young (2010), who uses a histogram over a fixed grid to construct

the cross-sectional distribution. In his approach, updating the approximate cross-sectional

distribution is analytical and does not require numerical optimization. Therefore, it works

well with highly skewed distributions like the ones in our paper. One downside of Young’s

(2010) approach is to accurately approximate the distribution, it requires a large number

of state variables in Dynare, which makes adding additional idiosyncratic states difficult, if

not infeasible. Our solution method is also related to Reiter (2009) in the sense that he also

approximates the cross-sectional distribution with a histogram and employ a perturbation

method.

3.2 Calibration

Table 1 lists the parameter values that are unique to the HANK setup. We set U = 0.05,

which is the fraction of households with low productivity (ε = 0), and hence can be inter-

preted as the aggregate unemployment rate. Conditional on being unemployed, the prob-

ability of remaining unemployed, p, is 0.5. This means that the expected unemployment

duration is two quarters. The scaling parameter governing the disutility of labor, χ, is cho-

sen so that steady state labor supply in a representative agent version of the model would

be L

RANK

= 0.95.

6

The unemployment benefit is set to 40 percent the wage, µ = 0.4, which

follows Shimer (2005). The labor income tax rate is 30% following Kaplan et al. (2018).

d = 0 implies agents are not allowed to borrow, and

¯

l = 1.5 implies the time endowment for

work is 150% of l

RANK

= 1. If we interpret l

RANK

= 1 to eight hours a day,

¯

l = 1.5 means

the maximum amount someone can work is 12 hours a day. For other parameters, we follow

the calibration from Sims and Wu (2021a); see details in Table E.1 of Appendix E.

6

This could be interpreted as 95 percent of the population supplying l

RANK

= 1 unit of labor each, which

17

Table 1: Calibration of HANK parameters

Parameters Value Target Description

U 0.05 Fraction unemployed

p 0.5 unemployment duration two quarters Probability of staying unemployed

χ L

RANK

= 1 − U Labor disutility scaling parameter

µ 0.4 Unemployment benefit / wage

τ 0.3 Labor income tax rate

d 0 Borrowing constraint

¯

l 1.5 Time endowment

4 HANK vs RANK

In this section, we compare and contrast impulse responses to a QE shock under both a

RANK and a baseline HANK specification.

7

In the baseline HANK model, we assume

dividends are equally distributed across households; we explore the implications of different

distribution rules in Section 5.

Even with this equal distribution rule, there remains significant household wealth het-

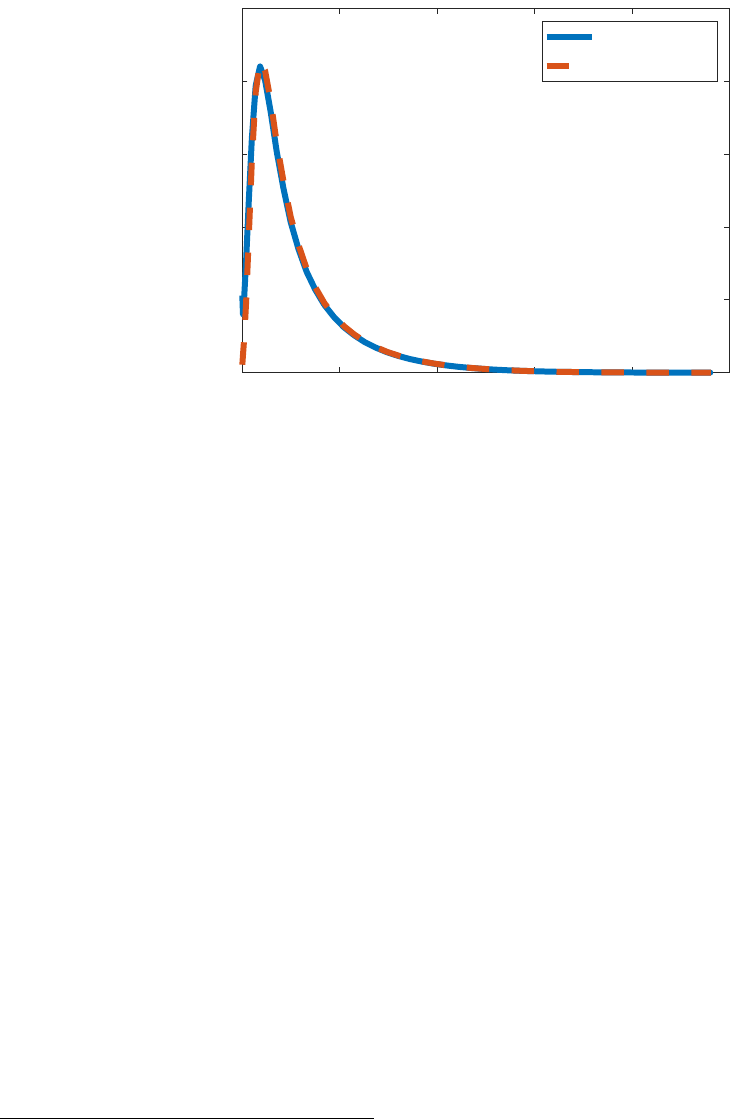

erogeneity that arises from uninsurable employment/productivity risk. Figure 1 plots the

stationary distribution of wealth across households, where wealth is normalized by the av-

erage steady state labor income. We do so for both unemployed households (solid blue line)

and employed households (dashed red line). Few households are located at the borrowing

constraint in the stationary distribution.

8

Nevertheless, most households are relatively poor,

with the distribution of wealth highly right skewed. There are a decent number of house-

holds who are quite wealthy and far away from the borrowing constraint. The distribution of

unemployed households is slightly towards the left of that for employed households, implying

that the former are, on average, less wealthy than the latter.

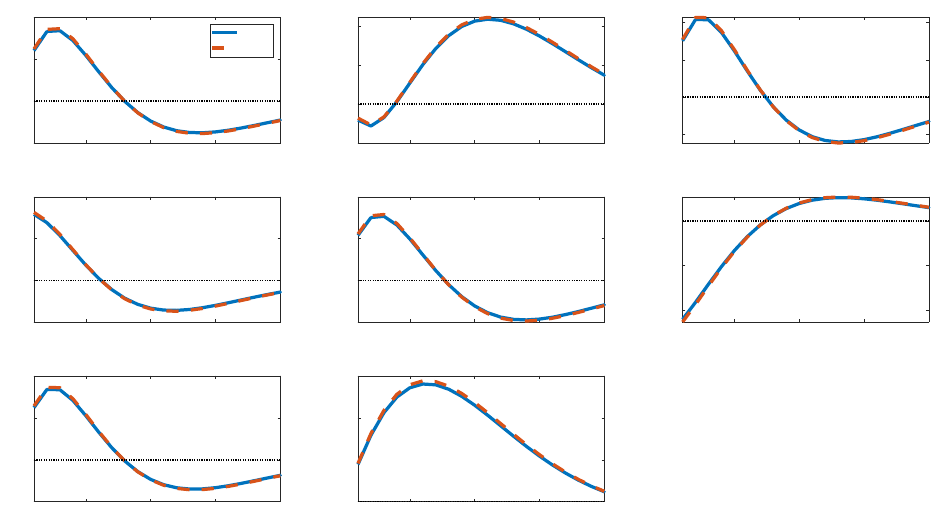

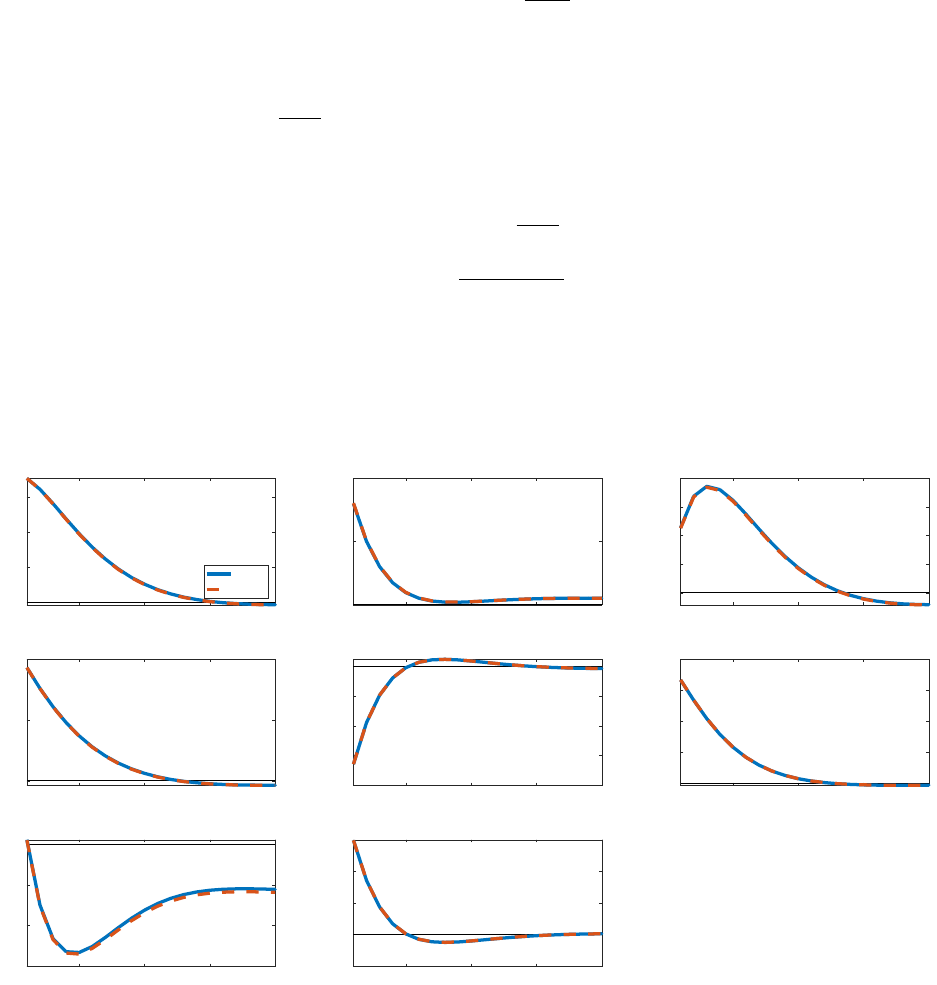

Figure 2 plots impulse responses to a persistent, private QE shock. The shock is scaled to

is comparable to the targeted 5 percent unemployment rate in the HANK specification.

7

The representative household of the RANK model is standard; we discuss the problem facing the house-

hold, and the associated first order optimality conditions, in Appendix F.

8

We do not include the borrowing constraint in the plot because its probability density is infinity by

construction.

18

Figure 1: Stationary Distribution

0 20 40 60 80 100

deposit/labor income

0

0.02

0.04

0.06

0.08

0.1

unemployed

employed

Notes: Blue solid line: unemployed households; red dashed line: employed households. We do not plot the

mass for constrained households. The x-axis measures the ratio between deposits and average steady state

labor income.

represent a four-percent increase in central bank bond holdings.

9

The solid blue lines show

responses under a RANK version of the model, while the dashed red lines are responses

generated from the HANK specification.

The responses of aggregate variables to a shock to central bank bond-holdings in the

RANK specification (blue) are similar to Sims and Wu (2021a). Bond purchases ease the

leverage constraint on intermediaries, which results in declining interest rate spreads. This,

in turn, results in more investment. Higher aggregate demand results in output, labor, and

inflation all rising temporarily.

For all aggregate variables, the responses under the HANK specification (dashed red lines)

are qualitatively and quantitatively similar to the RANK version of the model. Some vari-

ables, including consumption, output, inflation, and labor, rise slightly more in the HANK

specification on impact, but these differences are small and short-lived.

9

This shock generates a similar-sized response of output as to a conventional shock to the policy rule

for the short-term interest rate with a size of 25 basis points; see Figure G.1 in the appendix. As noted in

Appendix E, we assume an autoregressive parameter of 0.8. Responses to a public QE shock (i.e. a purchase

of long-term government bonds, instead of privately-issued bonds), would produce the same-shaped impulse

responses, albeit at a smaller scale.

19

Figure 2: Impulse responses to a QE shock: RANK vs. HANK

5 10 15 20

-0.5

0

0.5

1

output

RANK

HANK

5 10 15 20

-0.1

0

0.1

0.2

consumption

5 10 15 20

-2

0

2

4

investment

5 10 15 20

-0.05

0

0.05

0.1

inflation

5 10 15 20

-0.05

0

0.05

0.1

policy rate

5 10 15 20

-0.2

-0.1

0

corp. bond spread

5 10 15 20

-0.5

0

0.5

1

labor

5 10 15 20

0

0.5

1

1.5

deposit

Notes: This figure plots the impulse responses of aggregate variables under a 4% QE shock. The blue solid

lines are for the RANK model, and the red dashed lines are for the HANK model. The x-axis is time in

quarters, and the y-axis is the percentage change from steady state.

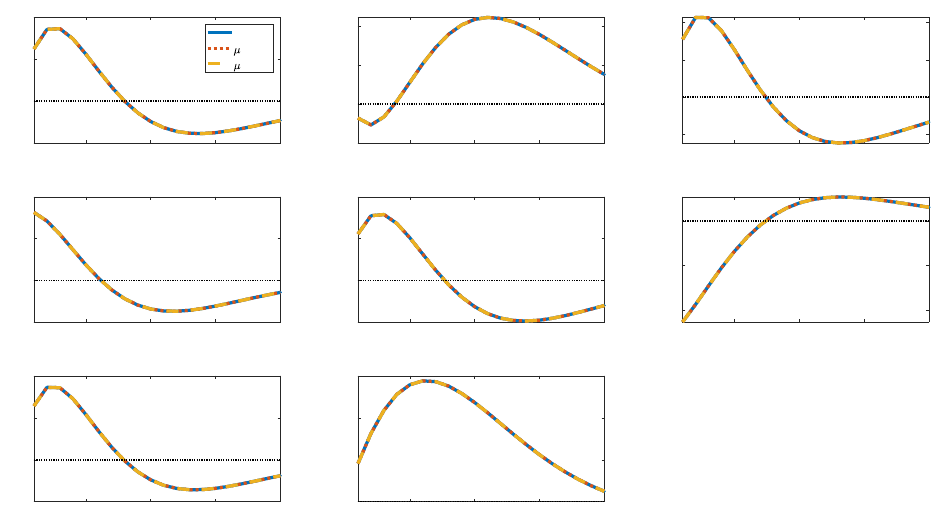

We next inspect the reasons for the slight differences in aggregate responses in the HANK

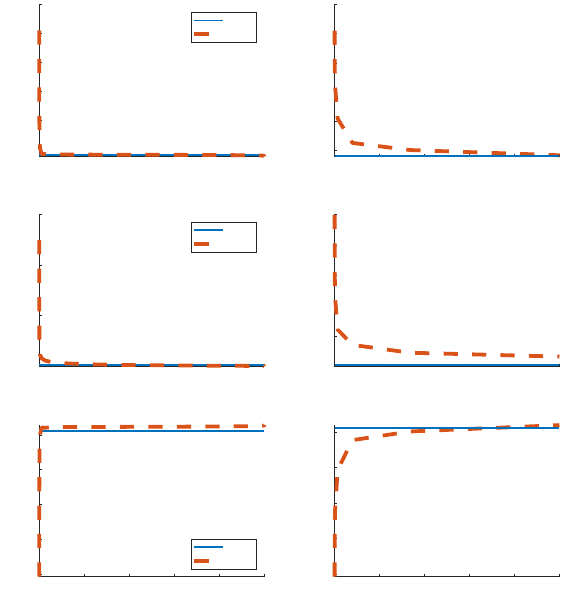

vs. RANK setups. Figure 3 plots the first-period responses of individual choice variables to

a QE shock against the percentile of the wealth distribution. We do so both for a RANK

version of the model (solid blue) and our baseline HANK version (dashed red lines). In the

left panel, we plot the first-period responses across the full wealth distribution. To increase

readability, in the right panels we zoom in on responses for households in the bottom one

percent of the wealth distribution. In the RANK model, all households behave identically,

so the figures simply show flat lines.

For all but the very poorest households, the first-period individual responses for con-

sumption, deposits, and labor are almost identical to the RANK counterpart. The poorest

households, in contrast, behave quite differently. These households increase their consump-

tion and deposits, and reduce their labor supply, following a QE shock. What drives these

results? Households located near the borrowing constraint are working more and consuming

20

Figure 3: First period individual responses to a QE shock: RANK vs. HANK

0 20 40 60 80 100

0

0.2

0.4

0.6

0.8

1

consumption

RANK

HANK

0 20 40 60 80 100

0

20

40

60

deposit

RANK

HANK

0 20 40 60 80 100

deposit percentile

-0.2

0

0.2

0.4

0.6

labor

RANK

HANK

0 0.2 0.4 0.6 0.8 1

0

0.2

0.4

0.6

0.8

1

consumption

0 0.2 0.4 0.6 0.8 1

0

10

20

30

40

50

deposit

0 0.2 0.4 0.6 0.8 1

deposit percentile

-0.2

0

0.2

0.4

0.6

labor

Notes: This figure plots the impulse responses of (employed) individual decision variables (consumption,

deposits, and labor supply) in the period when a 4% positive QE shock hits. The blue solid lines and red

dotted lines are for the RANK and baseline HANK models, respectively. The x-axis measures the wealth

fraction from poor to rich, and the y-axis is the percentage relative to steady state. The left panel plots

first-period responses across the full wealth distribution, while the right panel zooms in on the bottom one

percent.

less than they would find optimal absent a borrowing constraint. The extra income from

the QE shock allows them to move towards the unconstrained optimal allocation. They also

take advantage of the income windfall by significantly increasing deposits, which moves them

further from the borrowing constraint. The fact that only few households behave differently

helps to explain why there is very little difference in the aggregate responses to a QE shock

in the HANK and RANK models.

We conclude from the analysis in this section that the aggregate responses to an expan-

sionary QE shock are quite similar in the HANK and RANK specifications, at least for the

equal distribution rule. Though there are micro-level differences in behavior for the poorest

households, overall they do not have much impact on the dynamics of macro aggregates.

21

In the next sections, we investigate whether this conclusion holds up when dividends are

distributed differently across households or when we vary some macro parameters.

5 Implications of the Micro-Distribution of Wealth

In this section, we explore the implications of the micro wealth distribution for our main

results discussed in Section 4. First, we specify a more general distribution for dividends

in Subsection 5.1. Next, we show the role of different rules for popular metrics of wealth

inequality, such as the Lorenz Curve or the Gini Coefficient in Subsection 5.2. Finally, in

Subsection 5.3, we circle back to the main question of interest of the paper and examine how

the micro wealth distribution influences the macro responses to a QE shock.

5.1 Distribution Rules

In Section 4, we assumed dividends from production firms are equally distributed among

households. We now assume a more general dividend distribution rule:

div

j,t

div

t

= a

t

+ b

t

d

ϑ

j,t−1

. (5.1)

In (5.1), d

j,t−1

corresponds to household j’s wealth level (in the form of deposits). a

t

and b

t

are time-varying parameters that govern how household j’s share of dividends vary with its

wealth. ϑ ≥ 1 allows for a household’s dividends to vary non-linearly with its own wealth.

Taking ϑ as given, the parameters a

t

and b

t

are chosen so that the following two equations

hold each period:

Z

1

0

a

t

+ b

t

d

ϑ

j,t−1

dj = 1, (5.2)

a

t

+ b

t

¯

d

ϑ

a

t

+ b

t

d

ϑ

= n. (5.3)

22

(5.2) imposes that the sum of dividends received by individual households must equal aggre-

gate dividends each period. (5.3) says that the ratio of the dividends received by the richest

household (i.e. the household on the largest point on our deposit grid,

¯

d) to the dividends

received by the poorest household (i.e. the household on the lowest point on our deposit

grid, d = 0) is equal to n.

10

In Section 4, we implicitly imposed n = 1.

11

In this section, we

experiment with different values of n and ϑ.

To get a better sense of how different values of n and ϑ impact households in the model,

Figure 4 plots the relative weight of dividends received by individuals with different wealth

levels in the model’s stationary distribution,

a+bd

ϑ

j

a

=

1 +

b

a

d

ϑ

j

, where we take the poorest

household, with d = 0, as the reference point. By construction, the poorest household always

has a relative weight of unity, and the richest household always has a relative weight of n.

The notation we use is that the letter standards for ϑ; we consider three values, L for linear

(ϑ = 1), S for squared (ϑ = 2), and C for cubic (ϑ = 3). The number after the letter

corresponds to the assumed value of n. We consider values of n = 10 and n = 100; our

baseline case, which we label “HANK,” can also be labeled L1 (ϑ = 1 (linear) and n = 1).

The left panel considers linear distribution schemes (ϑ = 1), while the right panel compares

the linear distribution scheme to the squared and cubic schemes by fixing n = 10.

In our baseline HANK specification (blue line, left panel) all households receive the same

dividends, and the relative weights are therefore constant at unity. When we increase n but

remain in the linear specification, all other households receive a higher share of dividends

relative to the poorest household. The relative weight of a household at a fixed percentile in

the wealth distribution is bigger the larger is n.

Even though a larger n means the richest household receives more dividends than the

poorest, the linear scheme has the effect of allocating more dividends to the middle of the

10

Note that we solve the model with fixed grid points for deposits, so

¯

d is always the same. In other words,

the wealth gap between the richest and poorest household is always fixed.

11

Focusing on (5.3), when n = 1, given that d ̸=

¯

d it must be the case that b

t

= 0. But then from (5.2),

it follows that a

t

= 1. When n ̸= 1, then b

t

̸= 0 and will be time-varying. This also means that a

t

̸= 1 and

will also be time-varying.

23

Figure 4: Relative distribution weight

0 20 40 60 80 100 120 140

deposit

1

20

40

60

80

100

HANK

L10

L100

0 20 40 60 80 100 120 140

deposit

1

5

10

L10

S10

C10

Notes: This figure plots the relative weight of dividend obtained by people at different wealth level at the

stationary distribution (1 +

b

a

d

ϑ

j

). The blue solid lines, red dotted lines, and the yellow dashed lines on

the left(right) column are for the baseline HANK(L10), L10(S10), and L100(C10) models, respectively. The

x-axis is the wealth level, and the y-axis is the relative weight.

wealth distribution when n is bigger. This has the effect of reducing overall inequality. This

implication is illustrated in the left panel of Figure 5, which plots the stationary wealth

distribution from our model under the same dividend distribution rules as the left panel of

Figure 4. From Figure 5, we can see that higher values of n shift more mass in the stationary

distribution to the right, although this mass remains concentrated away from the far-right

tail.

In the right panel of Figure 4, we compare a linear distribution scheme (solid blue line)

to squared and cubic schemes (dotted-red and dashed-orange lines, respectively). While

the endpoints are the same in all cases, more curvature will increase inequality. We show

this result with the right panel of Figure 5. Relative to a linear distribution scheme, more

curvature has the effect of concentrating much more mass near the borrowing constraint,

which has the effect of increasing overall wealth inequality. For example, in both the squared

and cubic specifications, there are roughly 1.5 times as many households at the peak of the

stationary distribution relative to the linear scheme.

5.2 Inequality Measures

The exact form of the dividend distribution rule has important implications for the model’s

Lorenz curve as well as its Gini coefficient, both of which are important measures of inequality

24

Figure 5: Stationary distribution

0 20 40 60 80 100

deposit/labor income

0

0.02

0.04

0.06

0.08

0.1

HANK

L10

L100

0 20 40 60 80 100

deposit/labor income

0

0.02

0.04

0.06

0.08

0.1

0.12

L10

S10

C10

Notes: This figure plots the stationary distribution generated by different models. The blue solid lines, red

dotted lines, and the yellow dashed lines on the left(right) are for the baseline HANK(L100), L10(S100), and

L100(C100) models, respectively. The x-axis is the ratio between wealth and labor income, and the y-axis

is the density.

Figure 6: Lorenz curve

0 20 40 60 80 100

population percentile

0

10

20

30

40

50

60

70

80

90

100

deposit percentile

HANK

L10

L100

45 degree line

0 20 40 60 80 100

population percentile

0

10

20

30

40

50

60

70

80

90

100

deposit percentile

L10

S10

C10

45 degree line

Notes: This figure plots the Lorenz curve of stationary wealth distribution when the dividends are distributed

according to different functions. The blue solid lines, red dotted lines, and the yellow dashed lines on the

left(right) column are for the baseline HANK(L10), L10(S10), and L100(C10) models, respectively, the thin

black solid lines are the 45 degree line. The x-axis is the fraction of population, and the y-axis is the fraction

of wealth.

on which the extant literature has often focused.

Figure 6 plots Lorenz curves for different dividend distribution schemes. A Lorenz curve

plots the cumulative fraction of overall wealth against the population percentile. In our

model, household wealth takes the form of deposits. Points along the 45-degree line represent

perfect equality; points below the 45-degree line indicate that wealth is unequally distributed,

with more wealth held by a small fraction of households.

25

Table 2: Gini coefficient

HANK L10 L100 S10 C10

Gini coeff. 0.44 0.39 0.34 0.48 0.51

Notes: This table reports the Gini coefficients in different models.

The left panel plots the Lorenz curves for linear distribution rules. The blue line corre-

sponds to our baseline specification (labeled HANK, with equal dividend distribution). The

dotted red curve and the dashed orange curve show the Lorenz curves associated with linear

distribution schemes with larger values of n (10 and 100). Consistent with the shapes of

the stationary distributions, a larger value of n reduces observed inequality and shifts the

Lorenz curves upward. In the right panel, we plot Lorenz Curves conditioning on n = 10,

but for different values of ϑ. Here we observe that larger values of ϑ shift the Lorenz curve

down, meaning there is more inequality.

Table 2 corroborates the results depicted graphically in Figure 6 by showing Gini co-

efficients for different dividend distribution rules. The Gini coefficient is the ratio of the

area between the 45-degree line and the Lorenz curve to the total area under the 45-degree

line. A larger Gini coefficient indicates higher inequality. Our baseline HANK specification

produces a Gini coefficient of 0.44. Focusing on a linear distribution scheme with higher

values of n, the model’s Gini coefficient falls. A squared or cubic specification, in contrast,

results in more observed inequality.

5.3 Macro Aggregates

Our analysis above suggests that our model is capable of generating sizable wealth inequality

with alternative dividend distribution rules. However, the question we are interested in is

not whether the model can match moments of the wealth distribution. Rather, the key

question of the paper is whether a model featuring more (or less) inequality matters for the

transmission of QE shocks into aggregate variables. We show in this subsection that there is

little economically meaningful connection between the dividend distribution rule, inequality

26

Figure 7: Impulse responses to a QE shock: HANK with different distribution

rules

5 10 15 20

0

0.5

1

output

HANK

L10

L100

5 10 15 20

0

0.1

0.2

consumption

HANK

L10

L100

5 10 15 20

-2

0

2

4

investment

HANK

L10

L100

5 10 15 20

0

0.05

0.1

inflation

HANK

L10

L100

5 10 15 20

0

0.5

1

output

L10

S10

C10

5 10 15 20

0

0.1

0.2

consumption

L10

S10

C10

5 10 15 20

-2

0

2

4

investment

L10

S10

C10

5 10 15 20

0

0.05

0.1

inflation

L10

S10

C10

Notes: This figure plots the impulse responses of aggregate variables with linear distribution under a positive

QE shock. The blue solid lines, red dotted lines, and the yellow dashed lines in the left(right) column are

for the baseline HANK(L10), L10(S10), and L100(C10) models, respectively. The x-axis is time, and y-axis

is the percentage change from steady state.

moments, and aggregate effects of QE shocks.

Figure 7 plots impulse responses to a QE shock under different dividend distribution

specifications. The picture is divided into two panels, with responses in the HANK, L10, and

L100 specifications in the left panel, and responses for the L10, S10, and C10 specifications

in the right panel. We focus only on responses of output, consumption, investment, and

inflation here, but the responses are otherwise generated in the same manner as in Figure 2.

The responses of aggregate variables to a QE shock are remarkably similar under all

specifications; this means they are all, in turn, very close to the RANK specification as well.

There are some small differences for the response of aggregate consumption, but the inflation,

output, and investment responses are almost identical across all specifications. These results

27

suggest that the exact form of the dividend distribution rule – though relevant for inequality

moments like the Gini coefficient – is unimportant for the aggregate transmission of a QE

shock. This, in turn, suggests that the literature’s heavy focus on these inequality statistics

may be misplaced, at least to the extent to which one focuses on dynamics of aggregate

variables.

6 Implications of the Macro-Distribution of Wealth

In this section, we investigate how some parameters related to the macro-distribution of

wealth impact our results. In particular, we are interested in how parameters such as the

unemployment rate, the unemployment benefit, the unemployment duration, and households’

risk aversion affect the stationary wealth distribution, and in turn the aggregate transmission

of QE shocks.

6.1 Unemployment Rate

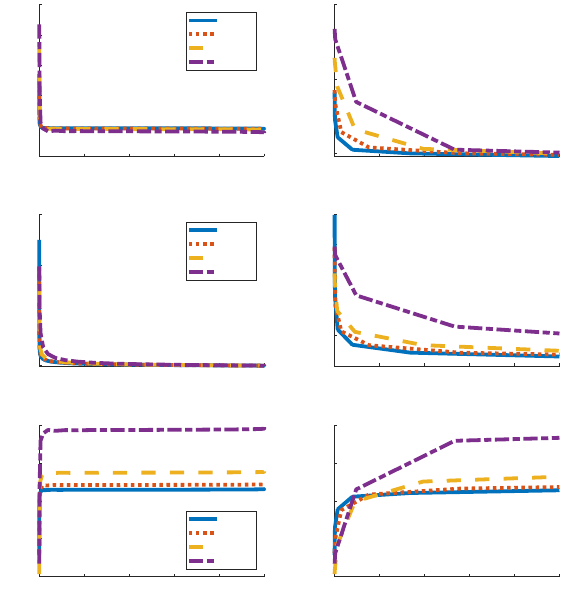

In our baseline calibration, we set the unemployment rate to five percent. While consistent

with the data, this relatively low unemployment rate means that households face a small

probability of job loss. In this section, we allow a higher unemployment rate, which means

households face more uninsurable income risk, and study its implications for the behavior of

aggregate consumption, and hence other aggregate variables, in response to a QE shock.

Figure 8 plots the stationary wealth distribution in our model with four different targets

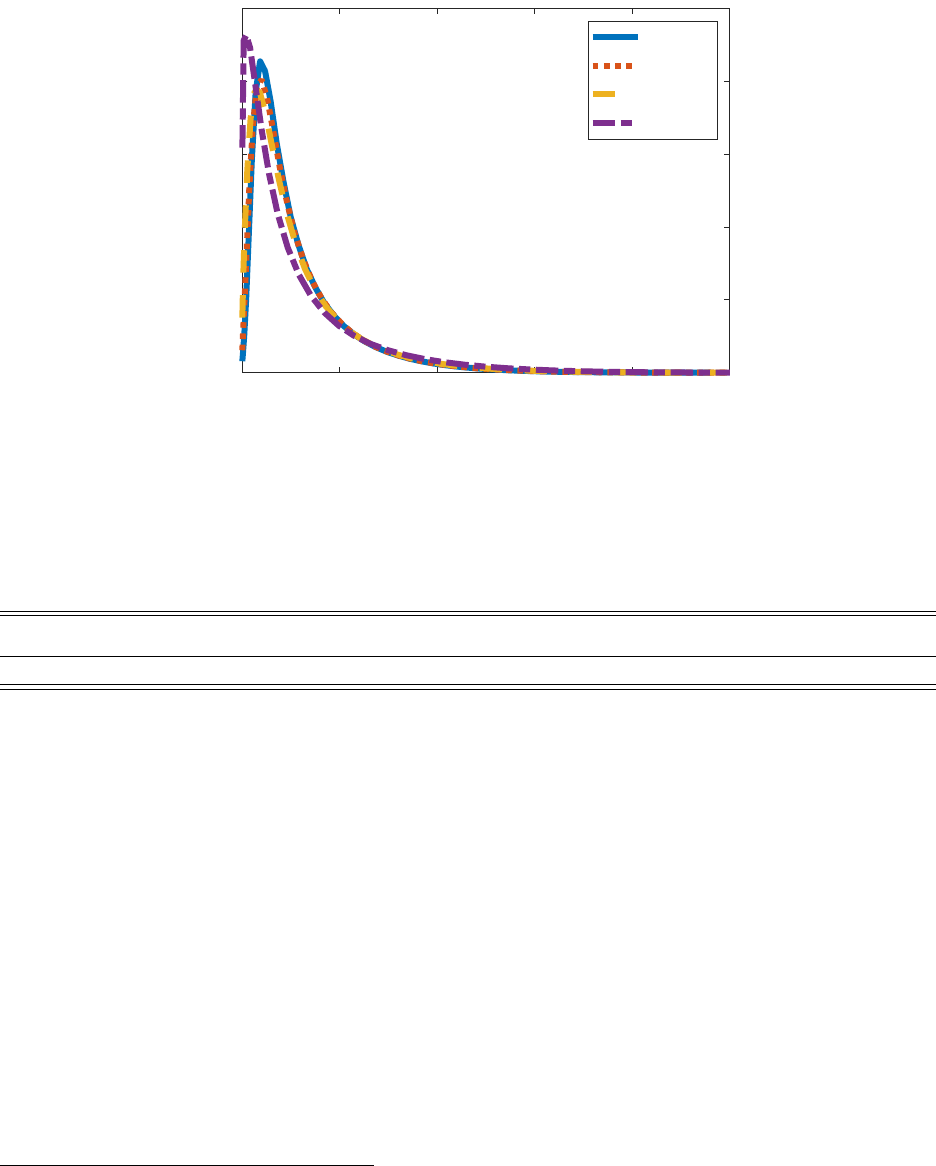

for the unemployment rate – our baseline specification of five percent, labeled HANK (solid

blue line), 10 percent (dotted red line), 20 percent (dashed orange line), and 40 percent

(dashed purple line). While a 40 percent unemployment rate is clearly unrealistic, it is not

unreasonable compared to labor force non-participation rates. Increasing the unemployment

rates shifts mass in the stationary distribution towards the borrowing constraint.

28

Figure 8: Stationary Distribution: HANK vs. U = 10%, 20% and 40%

0 20 40 60 80 100

deposit/labor income

0

0.02

0.04

0.06

0.08

0.1

HANK

U=10%

U=20%

U=40%

Notes: This figure plots the stationary distribution of the population. The blue solid line is for the HANK

model, the red dotted line is for the model with 10% unemployment rate, the yellow dashed line is for the

model with 20% unemployment rate, and the purple dash-dotted line is for the model with 40% unemploy-

ment rate. The x-axis is the ratio between wealth and average steady state labor income, and the y-axis is

the density.

Table 3: Households At and Near the Borrowing Constraint

HANK U = 10% U = 20% U = 40% µ = 30% µ = 50%

7.80 5.81 5.94 19.60 4.76 13.22

Notes: This table reports the percentage of households near the borrowing constraint (defined as having

deposits less than two quarters’ worth of average steady-state labor income) in different models.

Table 3 shows the percentage of households located at or near the borrowing constraint in

different specifications of our model. We define households as near the borrowing constraint

if their accumulated wealth amounts to less than two quarters’ worth of average steady-state

labor income. In our baseline HANK model, just under 8 percent of households are near

the borrowing constraint. When the unemployment rate is 40 percent, nearly 20 percent of

households have fewer than two quarters’ worth of labor income saved. It appears as though

fewer households are located near the constraint for intermediate values of unemployment

of 10 and 20 percent. This is an artifact of the way we discretize the deposit grids.

12

The

12

Since lower unemployment results in higher average labor income, fewer deposit grid points satisfy the

condition that deposits are less than two quarters’ steady-state labor income.

29

Figure 9: Impulse responses to a QE shock: HANK vs. RANK for U = 10%, 20%,

and 40%

5 10 15 20

0

0.5

1

output

RANK--U=10%

HANK--U=10%

5 10 15 20

0

0.1

0.2

consumption

RANK--U=10%

HANK--U=10%

5 10 15 20

-2

0

2

4

investment

RANK--U=10%

HANK--U=10%

5 10 15 20

0

0.05

0.1

inflation

RANK--U=10%

HANK--U=10%

5 10 15 20

-0.5

0

0.5

1

output

RANK--U=20%

HANK--U=20%

5 10 15 20

0

0.1

0.2

consumption

RANK--U=20%

HANK--U=20%

5 10 15 20

-2

0

2

4

investment

RANK--U=20%

HANK--U=20%

5 10 15 20

0

0.05

0.1

inflation

RANK--U=20%

HANK--U=20%

5 10 15 20

0

1

2

output

RANK--U=40%

HANK--U=40%

5 10 15 20

0

0.2

0.4

consumption

RANK--U=40%

HANK--U=40%

5 10 15 20

0

5

10

investment

RANK--U=40%

HANK--U=40%

5 10 15 20

0

0.1

0.2

inflation

RANK--U=40%

HANK--U=40%

Notes: This figure plots the impulse responses of aggregate variables under a 4% QE shock. The blue

solid lines and red dotted lines on the left/middle/right column are for the HANK and RANK models with

10%/20%/40% unemployment rate, respectively. The x-axis is time, and the y-axis is the percentage change

from steady state.

extreme value of 40 percent unemployment gives a clearer sense of how the wealth distribution

varies with the unemployment rate. Note further, these numbers tend to underestimate

the true fraction of households that are located near the borrowing constraint because poor

people tend to work more and hence have a higher steady-state income than richer households

via a wealth channel, but we are defining being near the borrowing constraint based on

average labor income, not the income of individual households. This makes the denominator

smaller and the overall wealth/income larger.

Figure 9 plots impulse response to a QE shock in these scenarios. The left/middle/right

panel considers an unemployment target of 10/20/40 percent. Solid blue lines refer to re-

sponses in a RANK version of our model, calibrated to have a comparable steady state labor

input as the corresponding HANK model. Dotted red lines are impulse responses in a HANK

model. Compared to a RANK model, aggregate variables react more the higher is the unem-

ployment rate. These differences are small and mostly not visible for a 10 percent and even

30

Figure 10: First period individual responses to a QE shock: HANK vs. U = 10%,

20%, and 40%

0 20 40 60 80 100

-0.5

0

0.5

1

1.5

2

consumption

HANK

U=10%

U=20%

U=40%

0 20 40 60 80 100

0

20

40

60

deposit

HANK

U=10%

U=20%

U=40%

0 20 40 60 80 100

deposit percentile

-0.5

0

0.5

1

1.5

labor

HANK

U=10%

U=20%

U=40%

0 0.2 0.4 0.6 0.8 1

0

0.5

1

1.5

2

consumption

0 0.2 0.4 0.6 0.8 1

0

10

20

30

40

50

deposit

0 0.2 0.4 0.6 0.8 1

deposit percentile

-0.5

0

0.5

1

1.5

labor

Notes: This figure plots the impulse responses of (employed) individual decision variables (consumption,

deposits, and labor supply) in the period when a 4% positive QE shock hits. The blue solid lines, red dotted

lines, yellow dashed lines, and purple dash-dotted lines are for the baseline HANK model and the models

with U = 10%, U = 20%, and U = 40%, respectively. The x-axis is the wealth fraction from poor to rich,

and the y-axis is the percentage change from steady state. The left panel plots first-period responses across

the full wealth distribution, while the right panel zooms in on the bottom one percent.

a 20 percent unemployment target. There are somewhat more meaningful differences when

we target unemployment of 40 percent. Consumption rises, rather than falls, with output

and investment reacting about 20 percent more on impact to an expansionary QE shock

compared to a RANK model. Still, the responses with this extreme value of unemployment

are nevertheless qualitatively similar to the RANK specification as well as to our benchmark

HANK model.

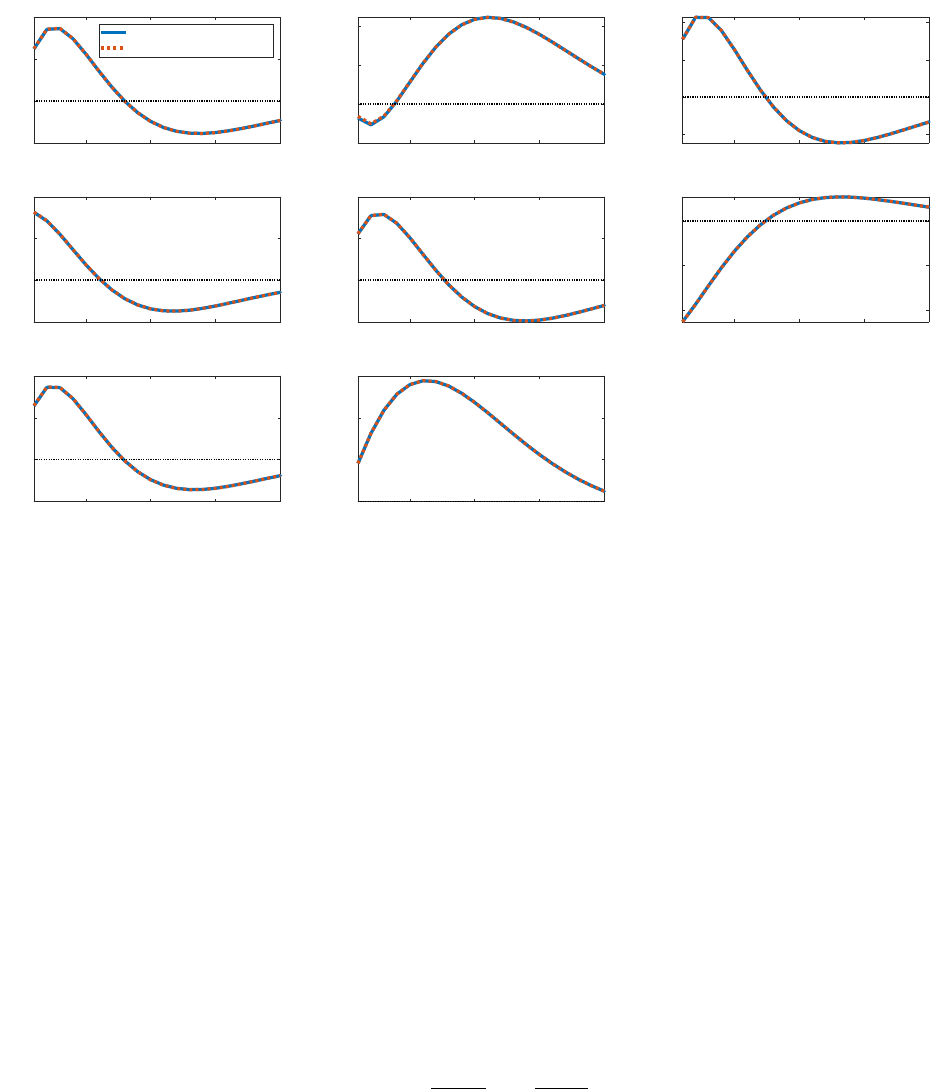

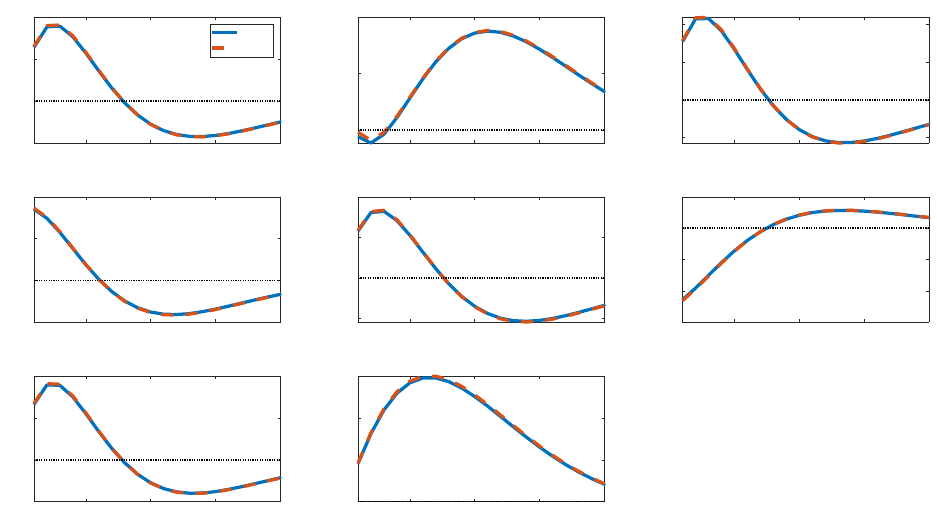

To provide some intuition, Figure 10 plots the first-period individual choice variable

responses to a QE shock as a function of wealth. The figure is analogous to Figure 3, but

compares HANK responses with different unemployment rates. The main differences are for

31

Figure 11: Stationary Distribution: HANK vs µ = 30% and 50%

0 20 40 60 80 100

deposit/labor income

0

0.02

0.04

0.06

0.08

0.1

HANK

=30%

=50%

Notes: This figure plots the stationary distribution of the population. The blue solid lines are for the HANK

model, the red dotted lines are for the model with 30% unemployment benefits, and the yellow dashed lines

are for the model with 50% unemployment benefits. The x-axis is the ratio between wealth and labor income,

and the y-axis is the density.

the poorest households, who increase their consumption and savings, and decrease labor,

by more the higher is the unemployment rate. It remains the case that households located

further from the borrowing constraint behave similarly with respect to consumption and

saving choices across different specifications, and in turn, similarly to the representative

agent counterpart from a RANK specification.

6.2 Unemployment Benefit

We next consider the role played by the unemployment benefit, µ in our model. We consider

both a smaller (µ = 0.30) and larger (µ = 0.50) value of this parameter compared to our

benchmark specification (µ = 0.40). Figure 11 plots the stationary distributions of wealth

for these three different values of the unemployment benefit. The bigger is µ, the more

mass is concentrated in the left tail near the borrowing constraint. The reason for this is

straightforward – with a bigger unemployment benefit, the cost of unemployment is smaller,

and households consequently have less incentive to self-insure against unemployment by

32

Figure 12: Impulse responses to a QE shock: HANK vs. µ = 30% and 50%

5 10 15 20

-0.5

0

0.5

1

output

HANK

=30%

=50%

5 10 15 20

-0.1

0

0.1

0.2

consumption

5 10 15 20

-2

0

2

4

investment

5 10 15 20

-0.05

0

0.05

0.1

inflation

5 10 15 20

-0.05

0

0.05

0.1

policy rate

5 10 15 20

-0.2

-0.1

0

corp. bond spread

5 10 15 20

-0.5

0

0.5

1

labor

5 10 15 20

0

0.5

1

1.5

deposit

Notes: This figure plots the impulse responses of aggregate variables under a 4% QE shock. The blue solid

lines are for the HANK model, the red dotted lines are for the model with 30% unemployment benefits, and

the yellow dashed lines are for the model with 50% unemployment benefits. X-axis is time in quarters, and

Y-axis is the percentage change from steady state.

saving. We see this channel at play in the right columns of Table 3, which show that with a

higher value of µ, a larger percentage of households are located near the borrowing constraint.

Figure 12 plots the impulse responses of aggregate variables to a QE shock with these

different values of the unemployment benefit. The responses with µ = 0.30 or µ = 0.50 are

virtually identical to the responses in our benchmark HANK specification.

6.3 Unemployment Duration

The duration of unemployment spells, governed in our model by the parameter p, is another

parameter of interest. In our benchmark model, we set this parameter to p = 1/2, implying

an average duration of unemployment spells of two quarters. We consider now a value of

p = 9/10, which implies a typical duration of unemployment of 10 quarters. The model is

re-parameterized with this new value of p to still target our benchmark unemployment rate

33

Figure 13: Impulse responses to a QE shock: unemployment duration = 2 vs. 10

quarters

5 10 15 20

-0.5

0

0.5

1

output

Unemployment duration=2

Unemployment duration=10

5 10 15 20

-0.1

0

0.1

0.2

consumption

5 10 15 20

-2

0

2

4

investment

5 10 15 20

-0.05

0

0.05

0.1

inflation

5 10 15 20

-0.05

0

0.05

0.1

policy rate

5 10 15 20

-0.2

-0.1

0

corp. bond spread

5 10 15 20

-0.5

0

0.5

1

labor

5 10 15 20

0

0.5

1

1.5

deposit

Notes: This figure plots the impulse responses of aggregate variables under a 4% QE shock. The blue solid

lines are for the RANK model, and the red dashed lines are for the HANK model. X-axis is time in quarters,

and Y-axis is the percentage change from steady state.

of five percent. Figure 13 plots aggregate responses to a QE shock for both our baseline

HANK specification as well as this new specification with a lower value of p. The aggregate

impulse responses are virtually identical.

6.4 Risk Aversion

Finally, we investigate the role played by households’ degree of risk aversion. Instead of

assuming log utility over consumption as in (2.1), we allow for a more general isoelastic

utility function, with lifetime flow utility now given by:

E

0

∞

X

t=0

β

t

c

1−σ

i,t

1 − σ

− χ

l

1+η

j,t

1 + η

!

,

where σ measures the coefficient of relative risk aversion. Log utility is a special case with

σ = 1.

34

Figure 14: Impulse responses to a QE shock: RANK vs. HANK for CRRA utility

5 10 15 20

-0.5

0

0.5

1

output

RANK

HANK

5 10 15 20

0

0.05

0.1

consumption

5 10 15 20

-2

0

2

4

investment

5 10 15 20

-0.05

0

0.05

0.1

inflation

5 10 15 20

-0.05

0

0.05

0.1

policy rate

5 10 15 20

-0.3

-0.2

-0.1

0

0.1

corp. bond spread

5 10 15 20

-0.5

0

0.5

1

labor

5 10 15 20

0

0.5

1

1.5

deposit

Notes: This figure plots the impulse responses of aggregate variables under a 4% QE shock. The blue solid

lines are for the RANK model, and the red dashed lines are for the HANK model. X-axis is time in quarters,

and Y-axis is the percentage change from steady state.

We consider a higher value of σ = 3, implying substantially more risk aversion than in

the case of log utility. Figure 14 plots impulse responses for a RANK version of our model

with σ = 3 (solid blue) and the HANK version with the same risk aversion (dashed red).

There is practically no difference between the two specifications.

7 Conclusion

We developed a quantitative DSGE model to study the aggregate implications of central bank

asset purchases when there is substantial household wealth heterogeneity. The financial

and production sides of the model are similar to Sims and Wu (2021a), which features

constrained financial intermediaries and scope for QE to matter. We model households

similarly to Krusell and Smith (1998): they are heterogeneous with respect to wealth, face

uninsurable unemployment risk, and are subject to a borrowing constraint. Different from

35

them, households endogenously choose labor supply. We developed a solution method that

is compatible with Dynare and uses perturbation methods to solve and simulate the model.

We find that the aggregate responses to central bank asset purchases are very similar in

a HANK specification compared to a RANK version of the model. We consider alternative

assumptions about the micro- and macro-distributions of wealth. For the former, we vary

how dividends are distributed across households. While different dividend distribution rules

can generate different amounts of wealth inequality based on popular metrics, they have

little discernible impact on how aggregate variables like output react to a QE shock. For the

latter, we examine how the unemployment rate, the unemployment benefit, the duration of

unemployment, and the degree of relative risk aversion impact the aggregate transmission of

QE shocks. For reasonable values of macro parameters, we find no discernible differences in

the impact of QE shocks between HANK and RANK models. We conclude that a RANK