Working Paper Series

Who gets jobs matters: monetary

policy and the labour market in HANK

and SAM

Uroš Herman, Matija Lozej

Disclaimer: This paper should not be reported as representing the views of the European Central Bank

(ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

No 2850

Abstract

This paper first provides empirical evidence that labour market outcomes for the less ed-

ucated, who also tend to be poorer, are substantially more volatile than labour market

outcomes for the well-educated, who tend to be richer. We estimate job finding rates and

separation rates by educational attainment for several European countries and find that

job finding rates are smaller and separation rates larger at lower educational attainment

levels. At cyclical frequencies, fluctuations of the job finding rate explain up to 80% of

the unemployment fluctuations for the less educated. We then construct a stylised HANK

model augmented with search and matching and ex-ante heterogeneity in terms of ed-

ucational attainment. We show that monetary policy has stronger effects when the job

market for the less educated and hence poorer is more volatile. The reason is that these

workers have the most procyclical income coupled with the highest marginal propensity

to consume. An expansionary monetary policy shock that increases labour demand dis-

proportionally affects the labour market segment for the less educated, causing a strong

increase in their consumption. This further amplifies labour demand and increases labour

income of the poor even more, amplifying the initial effect. The same mechanism carries

over to forward guidance.

JEL classification: E40, E52, J64

Keywords: Heterogeneous agents, Search and matching, Monetary policy, Business cycles, Employ-

ment

ECB Working Paper Series No 2850

1

Non-technical summary

In this paper we first provide a set of new empirical estimates of job finding and separation

rates by educational attainment, and their cyclical properties for several European countries.

We find that job finding rates for the less educated (and more likely poor) workers are lower,

highly procyclical, and more volatile than for the better educated (more likely better well-

off) workers. We also find that separation rates are higher, tend to be more volatile, and

often acyclical for the less educated workers. There are considerable differences across Eu-

ropean countries, with some countries where the labour market displays fewer differences

by educational attainment than in others. In all cases, fluctuations in job finding rates seem

to contribute the most to fluctuations in unemployment of the less educated at cyclical fre-

quencies, with the contribution of job finding rate fluctuations exceeding 80% in countries

like Germany and France. We report similar evidence for the US. In all cases, the evidence

suggests that agents with low educational attainment face higher employment risk over the

business cycle than agents with high educational attainment.

We then build a stylised model with the search and matching framework embedded in

a HANK framework that attempts to capture these empirical properties. The model con-

siders the economy as composed of different labour market segments, where workers can

either stay in the same market segment and face its income risk, or exogenously switch to an-

other labour market segment, with different characteristics regarding wage fluctuations and

(un)employment risk. These exogenous switches between labour market segments are rare

but persistent and can be thought of as persistent changes in the desirability for a particular

skill.

Labour market segments differ with respect to wage level, job finding probabilities, and

their cyclical properties. Each segment functions as a separate labour market with search

and matching frictions. This means that each labour market segment has an endogenous job

finding probability, which depends on firms’ incentives to create vacancies in that segment,

which in turn varies with economic conditions. Cyclical income fluctuations for households

that stay in the same labour market segment occur because search frictions, combined with

wage rigidities, lead to an increased vacancy posting following an expansionary shock, which

increases job finding rates and therefore expected labour income within each labour market

segment. Because the intensity of vacancy posting differs across labour market segments,

the differences between labour market segments change over the business cycle and affect the

idiosyncratic labour income risk for households. In other words, the income loss/gain due to

exogenous shifts from one labour market segment to the other differs over the business cycle.

We use this framework to investigate the implications of such heterogeneous labour mar-

kets for monetary policy. We show that if poor workers obtain relatively more jobs after a

monetary expansion, which is consistent with empirical evidence for most countries we con-

sider, they also spend a larger proportion of the additional income, because their marginal

propensity to consume is higher. This amplifies the aggregate demand increase, which leads

to more labour demand from firms that have to produce in order to meet consumption de-

ECB Working Paper Series No 2850

2

mand. Because the labour market for the poor is more sensitive to the business cycle, this

leads to a relatively stronger increase in employment of poorer households, which again leads

to a stronger increase in consumption. This works as an amplification mechanism that makes

monetary policy more potent.

What turns out to be important for the amplification is the asymmetry of the labour

market, in the sense that the labour market segment of the poor reacts more procyclically

than the labour market segments further to the right of the wealth distribution. We show that

this can be brought about by two mechanisms that amplify vacancy posting in the labour

market segment with lower educational attainment. One such mechanism is a relatively low

and hence more volatile firm surplus from hiring a worker from this labour market segment,

and the other is a higher wage rigidity in the segment. Either or both lead to more volatile

hiring for workers with lower educational attainment.

ECB Working Paper Series No 2850

3

1 Introduction

The distribution of wealth and the riskiness of income matter substantially for macroeco-

nomic fluctuations in the standard heterogeneous agent New Keynesian (HANK) models

(Kaplan et al., 2018). An important issue in the literature has been the so-called earnings het-

erogeneity channel (Auclert, 2019), which has focussed on the incidence of a particular type

of earnings such as interest, dividends, labour income and taxation (Werning (2015), Broer

et al. (2018), and Hagedorn et al. (2018)). There was less emphasis on the incidence of labour

income itself over the business cycle for different households, even though labour income is

typically the most important source of income for the majority of households.

Labour literature tends to find that workers face heterogeneous employment prospects

and, thus, income risk over the business cycle. For example, Elsby et al. (2010) document that

males, younger, less educated workers, and individuals from ethnic minorities experience

steeper rises in unemployment during all recessions. Similarly, Patterson (2023) finds that

earnings of individuals with higher marginal propensities to consume (i.e., young, black,

and poor) are more exposed to recessions.

1

Relatedly, Haltiwanger et al. (2018) document

that during the downturns, less educated and younger workers are more likely to exit to

nonemployment and less likely to get out of nonemployment. Hoynes et al. (2012) come

to a similar conclusion using individual-level Current Population Survey (CPS) and Merged

Outgoing Rotation Group (MORG) data.

2

Workers with such characteristics are more likely

to be poor. For example, in the Households Finance and Consumption Survey, the typical

finding is that younger and less educated households are more likely to be credit constrained

(see HFC (2016)).

Who is rich and who is poor matters in HANK models because households differ in

terms of their marginal propensities to consume. In this setting, it is important whether

household income (and income risk) is pro- or countercyclical because this matters for aggre-

gate demand, which in turn matters for general equilibrium effects on households’ incomes

(Werning (2015), Acharya and Dogra (2018), Bilbiie (2018)). Moreover, economic policies may

affect various segments of the wealth distribution differently, with the left tail typically being

more strongly affected (Amberg et al. (2022) and Broer et al. (2022)). Using administrative

data for the US, Guvenen et al. (2017) investigate how individual earnings vary across the

wealth distribution, and find that the sensitivity of the workers to the business cycle, the

so-called “worker betas”, is higher at the bottom and at the top of the earnings distribution.

Kramer (2022) finds that the sensitivity is substantially higher at the bottom of the earnings

distribution (but not at the top) using German data. Moreover, he can attribute this to the

fluctuations in the extensive margin rather than to wages. Auclert and Rognlie (2018) use

1

Mueller (2017) finds that during recessions, the pool of unemployed shifts towards high-wage workers.

Elsby et al. (2015) observe similar regularity, and they attribute it to compositional effect; during recessions,

the composition of the unemployment pool becomes skewed towards more attached individuals (i.e. male,

prime-aged, more educated) because they are less likely to exit the labour force.

2

Den Haan and Sedlacek (2014) develop a model where the least productive workers lose jobs first during

the recession, and the most productive workers tend to get jobs first during the boom.

ECB Working Paper Series No 2850

4

the results from Guvenen et al. (2017) to calibrate a function that rations labour of partic-

ular groups of households when wages are sticky, but the deeper underlying reasons why

and who gets/loses jobs in the boom/recession have been less thoroughly investigated. A re-

cent example of an approach that provides more micro-foundations for heterogeneous labour

market outcomes has been to use capital-skill complementarities (Dolado et al., 2021).

This paper first provides new empirical evidence on job finding and separation rates by

educational attainment for several European countries, which is novel and of independent

interest. We find that job finding rates for the less educated (and more likely poor) workers

are lower, highly procyclical, and more volatile than for the better educated (more likely

rich) workers. We also find that separation rates are higher, tend to be more volatile, and

often acyclical for less educated workers. There are considerable differences across European

countries, with some countries where the labour market seems more homogeneous (with

fewer differences by educational attainment) than in others. In all cases, fluctuations in job

finding rates contribute most to fluctuations in unemployment of the less educated at cyclical

frequencies, with the contribution of job finding rate fluctuations exceeding 80% in countries

like Germany and France. We report similar evidence for the US. In all cases, the evidence

suggests that agents with low educational attainment face higher employment risk over the

business cycle than agents with high educational attainment.

We then build a stylised model with the search and matching framework embedded in

a HANK framework that attempts to capture the above empirical regularities. The model

considers the economy as composed of different labour market segments, where workers can

either stay in the same market segment and face its income risk, or exogenously switch to

another labour market segment, with different characteristics regarding wage fluctuations

and (un)employment risk. These exogenous switches between labour market segments are

rare but persistent and can be thought of as persistent changes in desirability for a particular

skill.

3

Labour market segments differ with respect to wage level, job finding probabilities,

and their cyclical properties. Each segment functions as a separate labour market with search

and matching frictions. This means that each labour market segment has an endogenous job

finding probability, which depends on firms’ incentives to create vacancies in that segment,

which in turn varies with economic conditions. Cyclical income fluctuations for households

that stay in the same labour market segment occur because search frictions, combined with

wage rigidities, lead to an increased vacancy posting following an expansionary shock, which

increases job finding rates and therefore expected labour income within each labour market

segment. Because the intensity of vacancy posting differs across labour market segments,

the differences between labour market segments change over the business cycle and affect

the idiosyncratic labour income risk for households (the income loss/gain due to exogenous

shifts from one labour market segment to the other).

3

For instance, one can think of one incidence of such a switch looking at the data from a major job finding

intermediary, Indeed (Adrjan (2019)). These indicate that upon the announcement that the plant of British Steel

was scheduled to close, workers from that plant searched for jobs that were below their qualification level. That

is, they searched for a job in what is effectively a different labour market segment.

ECB Working Paper Series No 2850

5

We use this framework to investigate the implications of such heterogeneous labour

markets for monetary policy. We show that if poor workers obtain jobs after a monetary

expansion (which is consistent with empirical evidence), they spend a larger proportion of

the additional income, because their marginal propensity to consume is higher. This amplifies

aggregate demand, which leads to more labour demand from firms that have to produce

in order to meet consumption demand. Because the labour market for the poor is more

sensitive to the business cycle, this leads to a relatively stronger increase in employment of

poorer households, which again leads to a stronger increase in consumption. This works as

an amplification mechanism that makes monetary policy more potent. What turns out to be

important for the amplification is the asymmetry of the labour market, in the sense that the

labour market segment of the poor reacts more procyclically than the labour market segments

further to the right of the wealth distribution. We show that this can be brought about by

two mechanisms that amplify vacancy posting in the labour market segment with lower

educational attainment. One such mechanism is a relatively low and hence more volatile

firm surplus from hiring a worker from this labour market segment, and the other is a higher

wage rigidity in the segment. Either or both lead to more volatile hiring for workers with

lower educational attainment.

Our paper is most closely related to papers analysing economic fluctuations in het-

erogeneous agents models with labour market frictions (see, for example, Den Haan et al.

(2017), Ravn and Sterk (2017)). However, our paper differs from the others in focusing on the

differences between labour market segments and their implications for shock transmission.

Compared to Ravn and Sterk (2016) and Ravn and Sterk (2017), we consider the interplay

between several labour market segments and allow agents to save. Den Haan et al. (2017)

allow agents to save in two assets and solve the model fully globally, but they analyse a

unified labour market. Gornemann et al. (2016) do not differentiate between the structure of

labour market segments and focus mostly on systematic monetary policy and the distribution

of incomes from assets and labour, while our focus is on labour market segments. Kramer

(2022) models the transition between labour market segments as endogenous using directed

search, while our setting, where educational attainment is predetermined, considers switches

between labour markets that require different levels of educational attainment as exogenous

(and slow relative to the business cycle frequency). Differently from Dolado et al. (2021), our

model generates different labour market outcomes by only relying on labour market search

frictions without the need for capital-skill complementarity.

The remainder of the paper is structured as follows. Section 2 presents the empirical

evidence on who obtains jobs and when. Section 3 describes the model, Section 4 discusses

the results, and Section 5 concludes.

ECB Working Paper Series No 2850

6

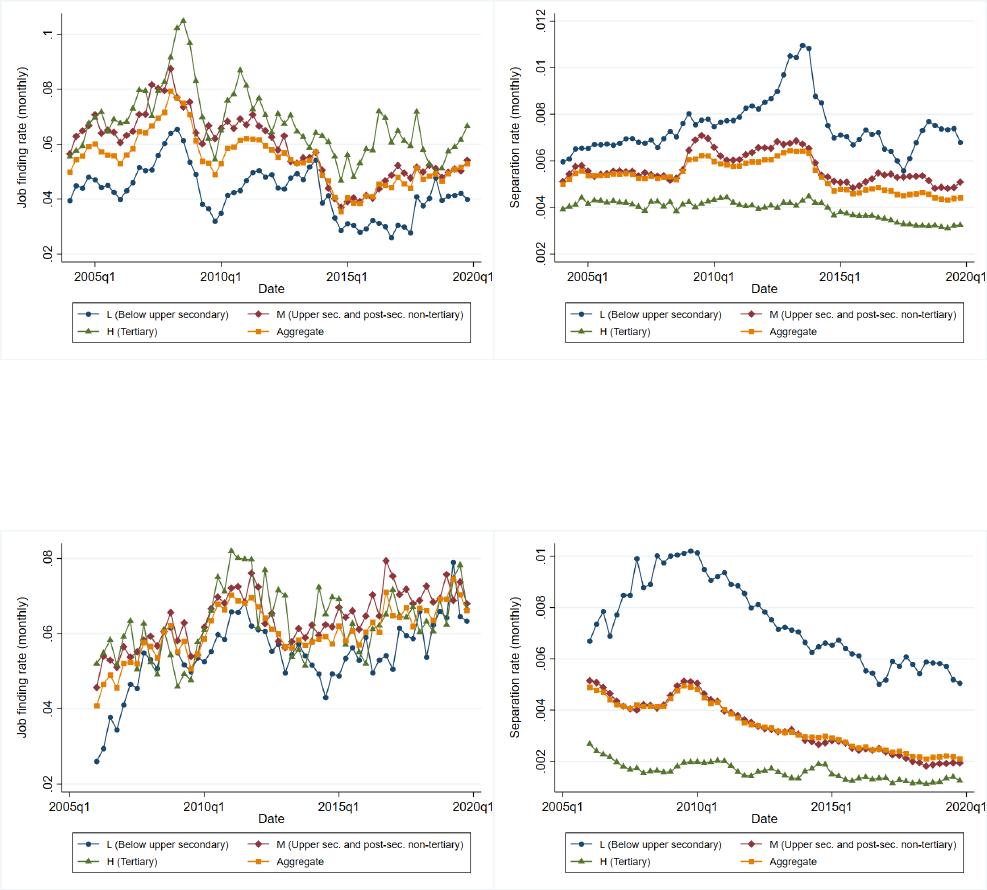

2 Who gets and who loses jobs

Employment outcomes of the well and less educated workers can differ markedly over the

business cycle. Education level can also serve as a proxy for income and wealth, and the

literature has shown that economic policies may affect households at a different point in the

wealth distribution differently (see, for example, Amberg et al. (2022) or Broer et al. (2022)).

This section provides novel empirical evidence for several European countries and the US

on who gets and who loses jobs at business cycle frequencies across educational attainment

levels, and what are the main driving forces behind it.

Before looking into the driving forces of unemployment fluctuations, it is instructive

to examine the variability of unemployment rates across educational attainment levels for

selected European countries. Table 1 shows that the unemployment rate at the lowest educa-

tional attainment level is much more volatile than the aggregate unemployment rate and the

unemployment rates at higher education levels for all countries considered, indicating that

those with lower educational attainment are much more exposed to business cycle fluctua-

tions. The remainder of this section examines the underlying forces that drive fluctuations

in unemployment rates, focussing on job finding and separation rates and their behaviour at

business cycle frequencies.

Table 1: Variability of unemployment rates over business cycles

Volatility Relative volatility

σ(u

i

) σ(u

i

)/σ(u)

Country Sample Agg. L M H L M H

France 2003Q1-2019Q4 0.35 0.57 0.36 0.28 1.60 1.00 0.80

Germany 2005Q1-2019Q4 0.25 0.36 0.28 0.16 1.41 1.11 0.64

Greece 1998Q1-2019Q4 1.39 1.55 1.60 1.00 1.12 1.15 0.72

Italy 2001Q1-2019Q4 0.47 0.61 0.43 0.35 1.31 0.92 0.75

Spain 1998Q1-2019Q4 1.23 1.57 1.23 0.85 1.27 0.99 0.69

UK 2000Q1-2019Q4 0.37 0.61 0.41 0.25 1.65 1.11 0.66

Notes: The table reports standard deviations of cyclical components of unemployment rates u

i

, and relative

volatilities with respect to the aggregate unemployment rate u , by educational attainment. Agg. = aggregate,

L = Less than primary, primary, and lower secondary education, M = Upper secondary and post-secondary

non-tertiary education, and H = Tertiary education. We end the sample in Q4 2019 to exclude the COVID-19

period.

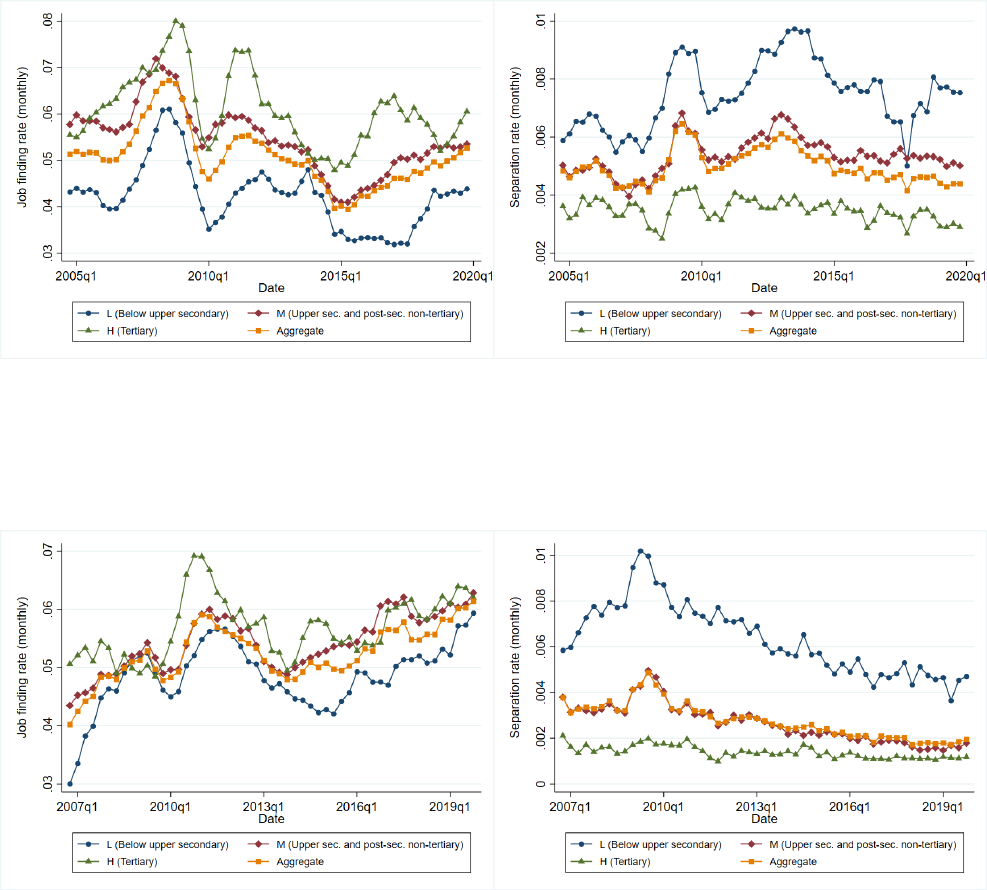

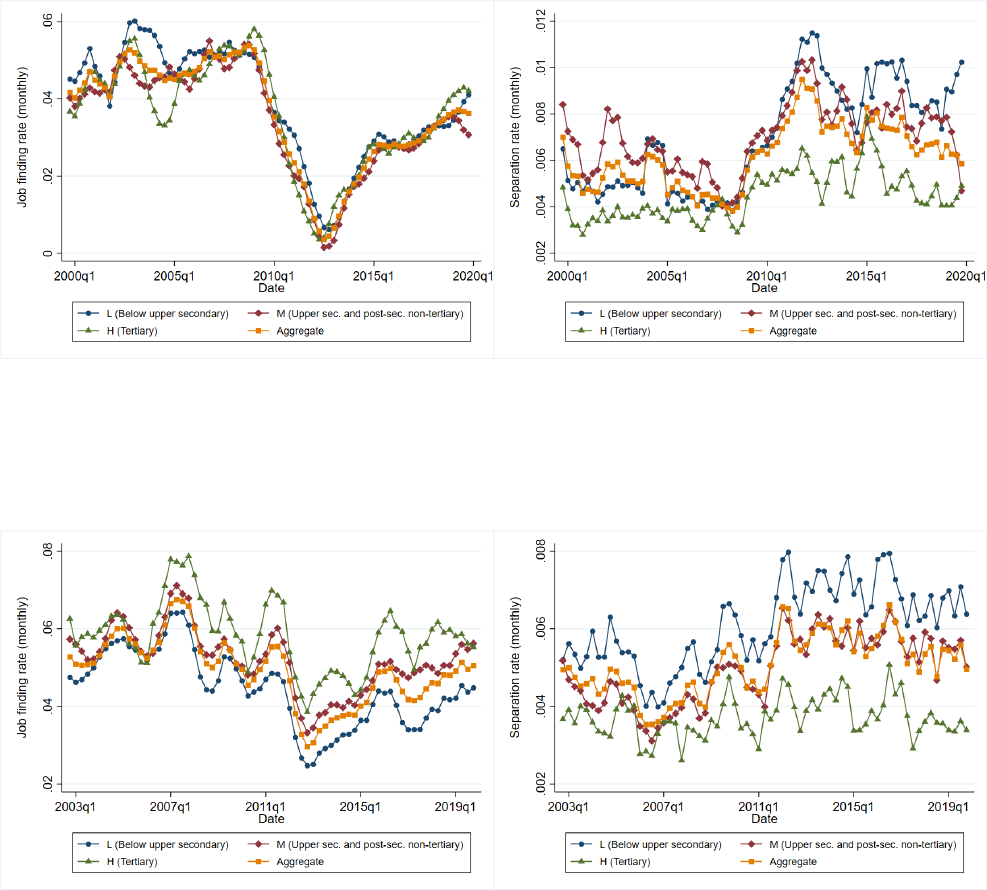

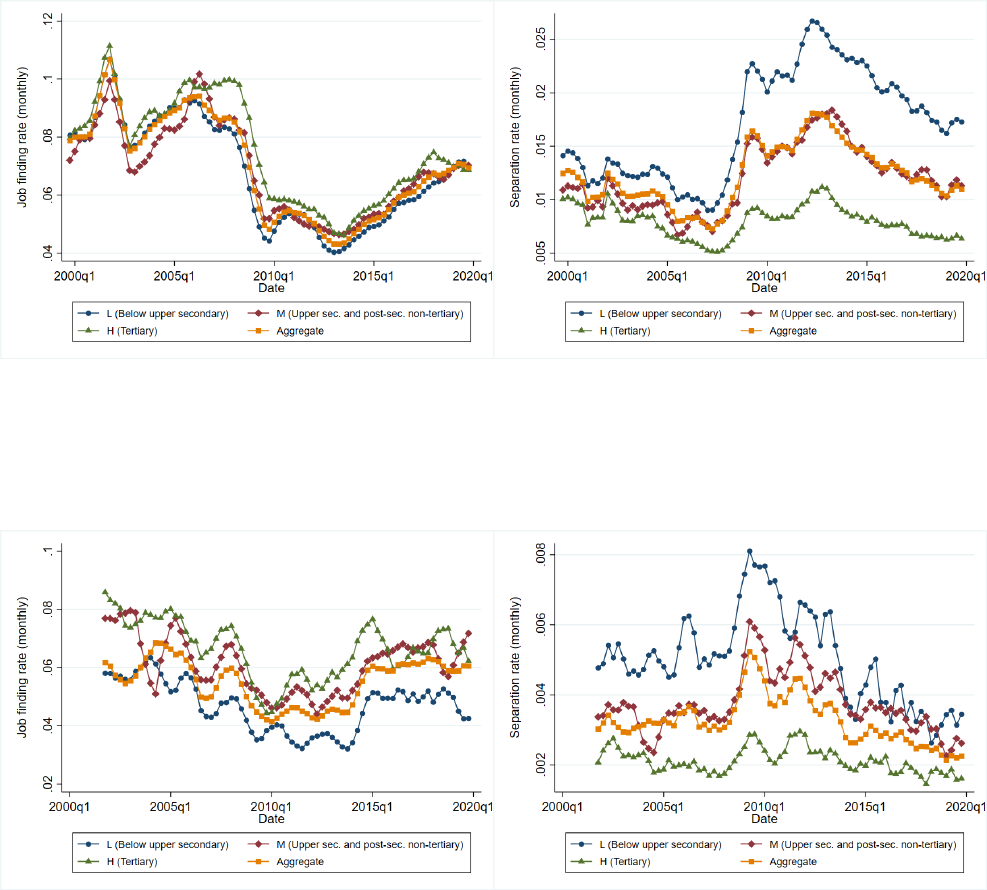

2.1 Job finding rates and separation rates by educational attainment in

Europe

To estimate job finding rates by educational attainment, we use data on unemployment spell

duration by educational attainment, available in European Union Labour Force Survey (EU–

LFS). In general, we follow the method by Shimer (2012), and its extension by Elsby et al.

(2013). The difference compared to Elsby et al. (2013) is that we have quarterly data on the

ECB Working Paper Series No 2850

7

duration of unemployment, so we can more directly relate outflows from unemployment to

Shimer’s approach (which is based on monthly data).

4

Using the approach in Shimer (2012), the monthly change in unemployment can be

written as follows

u

t+1

− u

t

= u

<1

t+1

− F

t

u

t

, (1)

where u

t

is unemployment at monthly frequency, u

<1

t+1

is the stock of unemployed with un-

employment duration of less than one month, and F

t

u

t

is the flow out of unemployment.

Rearranging and solving for outflow probability F

t

, one obtains:

F

t

= 1 −

u

t+1

− u

<1

t+1

u

t

, (2)

which can be used to get the (monthly) outflow hazard rate f

<1

t

f

<1

t

= −ln

(

1 − F

t

)

. (3)

Following Shimer (2012), we refer to f

t

as the job finding rate and to F

t

as the correspond-

ing job finding probability. The computation of this rate requires monthly data. However, as

pointed out by Elsby et al. (2013), one can use data at lower frequencies, and this may be more

convenient in labour markets that are less fluid than the US labour market, as is typically the

case in Continental Europe. In particular, one can compute

F

<d

t

= 1 −

u

t+d

− u

<d

t+d

u

t

, (4)

where d is the number of months, and compute the (monthly) outflow hazard rate as

f

<d

t

= −ln

1 − F

<d

t

/d. (5)

We follow this approach, using quarterly data on unemployment by educational at-

tainment collected by Eurostat, and EU–LFS data on unemployment duration spells, also by

educational attainment.

5

We do so for d ∈ {3, 6, 12}, and for three levels of educational attain-

ment: (L) Less than primary, primary, and lower secondary education, (M) Upper secondary

and post-secondary non-tertiary, and (H) Tertiary education. We focus on large countries in

Europe. The reason for this is twofold. First, we have relatively few observations for shorter

unemployment spells due to the relatively less fluid labour markets in Continental Europe,

as pointed out by Elsby et al. (2013). Second, the data is quarterly, and we distinguish by edu-

4

As pointed out by Elsby et al. (2013), there could be an issue of duration dependence for data at a lower

frequency, if the labour market is very fluid, so that job finding rates and separation rates are high. However,

they note that this is less of a problem for most Continental European countries, where labour markets tend to

be less vibrant than in the US, and for which Elsby et al. (2013) find no evidence for duration dependence.

5

Data are seasonal, so we first compute 4-quarter moving averages to remove seasonal fluctuations. The

advantage of this over seasonal adjustment of each series is that it preserves additivity, i.e., moving averages of

unemployed by educational attainment add up to the moving average of total unemployed; moving averages of

the employed and unemployed sum to the moving average of the total labour force.

ECB Working Paper Series No 2850

8

cational attainment, which further reduces the sample. This means that for smaller countries

with a relatively small sample of the Labour Force Survey, we have only a few observations,

especially in the group with the highest educational attainment. We focus on d = 3 in the

main text but also report additional estimates for d = 6 and d = 12.

Table 2: Monthly job finding rates

f

<3

f

<6

f

<12

Country Sample L

M H L M H L M H

France 2003Q1-2019Q4 0.043 0.059

0.068 0.044 0.059 0.067 0.042 0.055 0.061

Germany 2005Q1-2019Q4 0.055 0.064 0.063 0.055 0.063 0.064 0.049 0.054 0.057

Greece 1998Q1-2019Q4 0.032 0.026 0.031 0.040 0.033 0.035 0.039 0.035 0.036

Italy 2001Q1-2019Q4 0.054 0.063 0.077 0.054 0.063 0.073 0.045 0.052 0.058

Spain 1998Q1-2019Q4 0.081 0.081 0.089 0.080 0.080 0.087 0.068 0.069 0.075

UK 2000Q1-2019Q4 0.049 0.068 0.077 0.052 0.070 0.079 0.047 0.061 0.066

Notes: The table reports monthly job finding rates f

t

using (5). L = Less than primary, primary, and lower

secondary education, M = Upper secondary and post-secondary non-tertiary education, and H = Tertiary edu-

cation. Values are sample averages. We end the sample in Q4 2019 to exclude the COVID-19 period.

Table 2 reports monthly job finding rates based on our estimates that can be compared

to those in Elsby et al. (2013).

6

Three main results stand out in these estimates. First, there

are considerable differences across countries, with job finding rates ranging from less then

0.03 in Greece to above 0.08 in Spain. Second, the job finding rate rises with educational

attainment and is the highest for those with tertiary education and above (H). However, there

are exceptions, such as Greece and Spain, where the job finding rate does not increase (or

only mildly increases) with the level of educational attainment.

7

Finally, and consistently

with Elsby et al. (2013), we find that duration dependence does not seem to play a role - our

estimates of levels and volatilities are similar for various durations.

With the estimates of job finding rates f

t

, it is possible to back out the corresponding

separation rates s

t

(and the corresponding separation probability S

t

). Shimer (2012) advocates

using the following formula, which accounts for the fact that a worker who loses a job can

find a new one within the same period:

u

t+1

=

1 − e

−

(

f

t

+s

t

)

s

t

f

t

+ s

t

l

t

+ e

−

(

f

t

+s

t

)

u

t

, (6)

where l

t

is labour force and e

t

is employment (and l

t

= e

t

+ u

t

).

8

This equation allows

us to solve for the separation rate implicitly. We apply it to each educational attainment

6

Table 12 in appendix reports quarterly job finding probabilities F

<d

t

that we use in Section 3 to calibrate the

model.

7

This may be due to public-sector employment reductions during the sovereign debt crisis, which might

have affected relatively more educated workers in the public sector, although we cannot verify this based on

our data.

8

Accounting for the possibility that workers can lose and find a job within the period could in principle be

important in our case because of the quarterly data frequency. However, because we find for all countries in our

sample that hazard rates f

t

and s

t

are low (as in Elsby et al. (2013)), this is less of a concern.

ECB Working Paper Series No 2850

9

level, using our estimates of job finding rates by educational attainment and by duration of

unemployment. The results are reported in Table 3.

Table 3: Monthly separation rates

s

<3

s

<6

s

<12

Country Sample L

M H L M H L M H

France 2003Q1-2019Q4 0.007 0.006

0.004 0.007 0.006 0.004 0.007 0.005 0.004

Germany 2005Q1-2019Q4 0.007 0.003 0.002 0.007 0.003 0.002 0.006 0.003 0.001

Greece 1998Q1-2019Q4 0.005 0.006 0.004 0.006 0.007 0.005 0.006 0.007 0.005

Italy 2001Q1-2019Q4 0.007 0.006 0.005 0.007 0.006 0.005 0.006 0.005 0.004

Spain 1998Q1-2019Q4 0.020 0.014 0.010 0.020 0.014 0.010 0.018 0.012 0.008

UK 2000Q1-2019Q4 0.005 0.004 0.003 0.005 0.004 0.003 0.005 0.004 0.002

Notes: The table reports monthly separation rates s

t

using (6). L = Less than primary, primary, and lower

secondary education, M = Upper secondary and post-secondary non-tertiary education, and H = Tertiary edu-

cation. Values are sample averages. We end the sample in Q4 2019 to exclude the COVID-19 period.

Separation rates in Table 3 are higher for lower educational attainments than for higher

educational attainment levels, except in Greece, where the separation rates are relatively

close for all three educational attainment groups. Overall, the evidence from job finding and

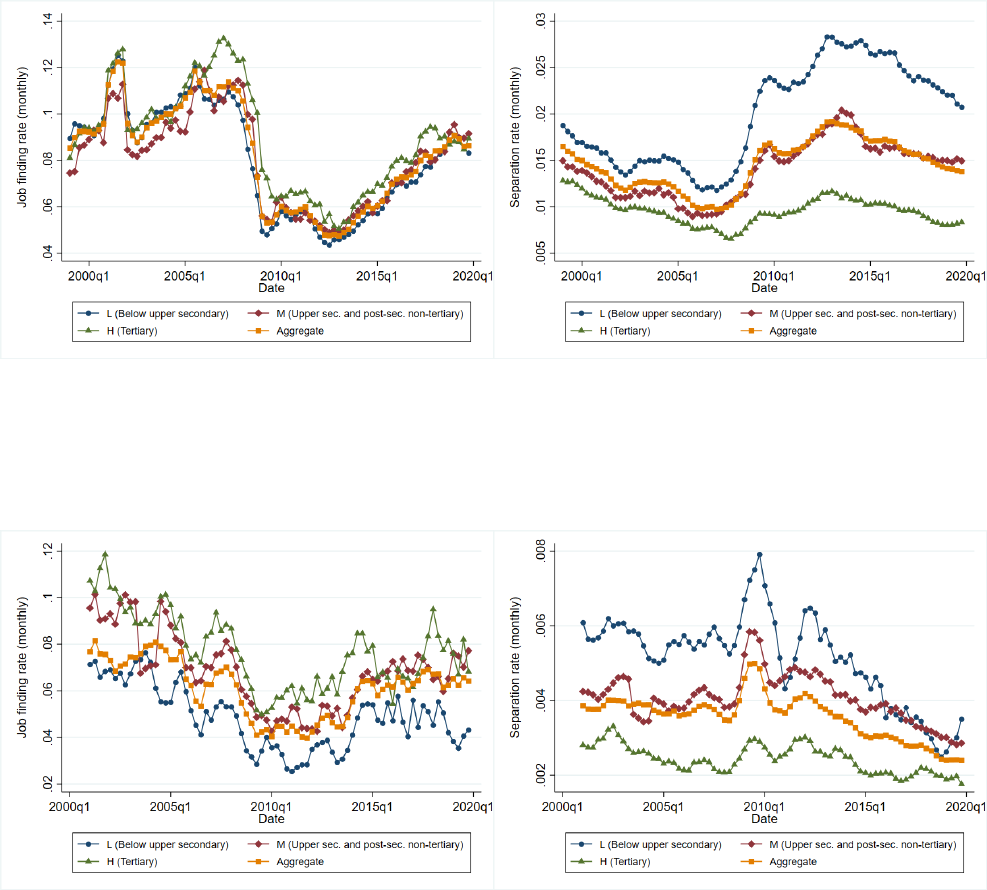

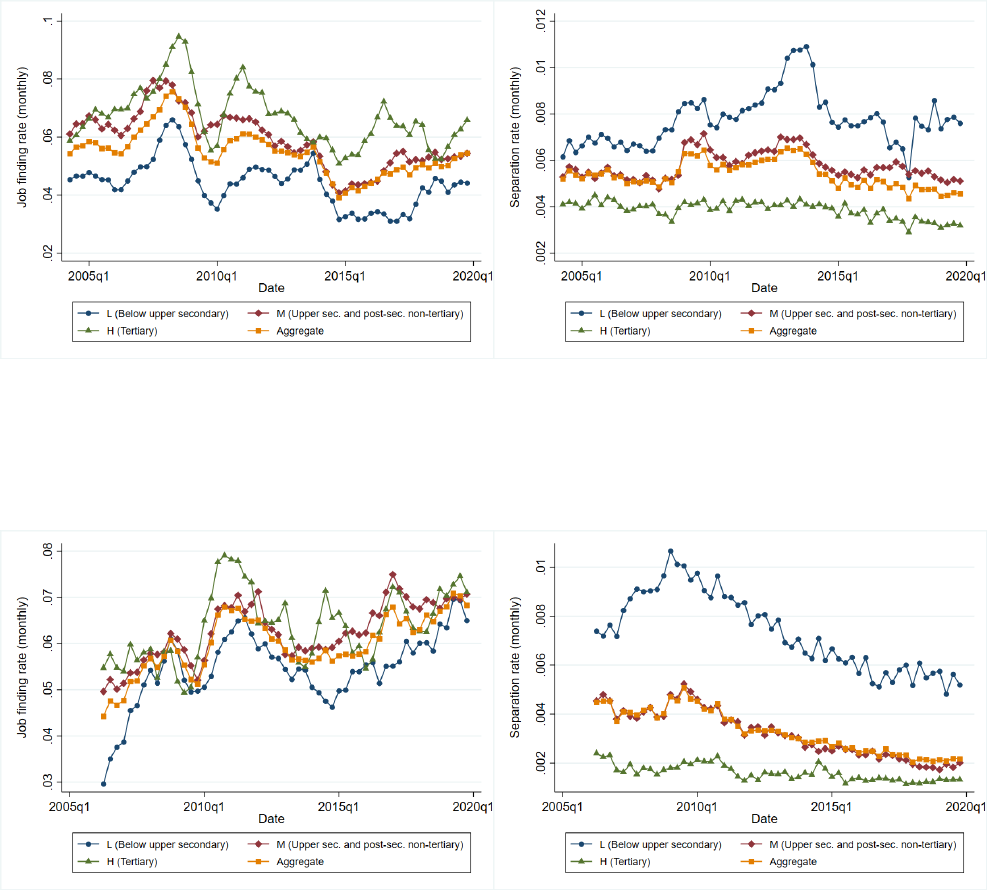

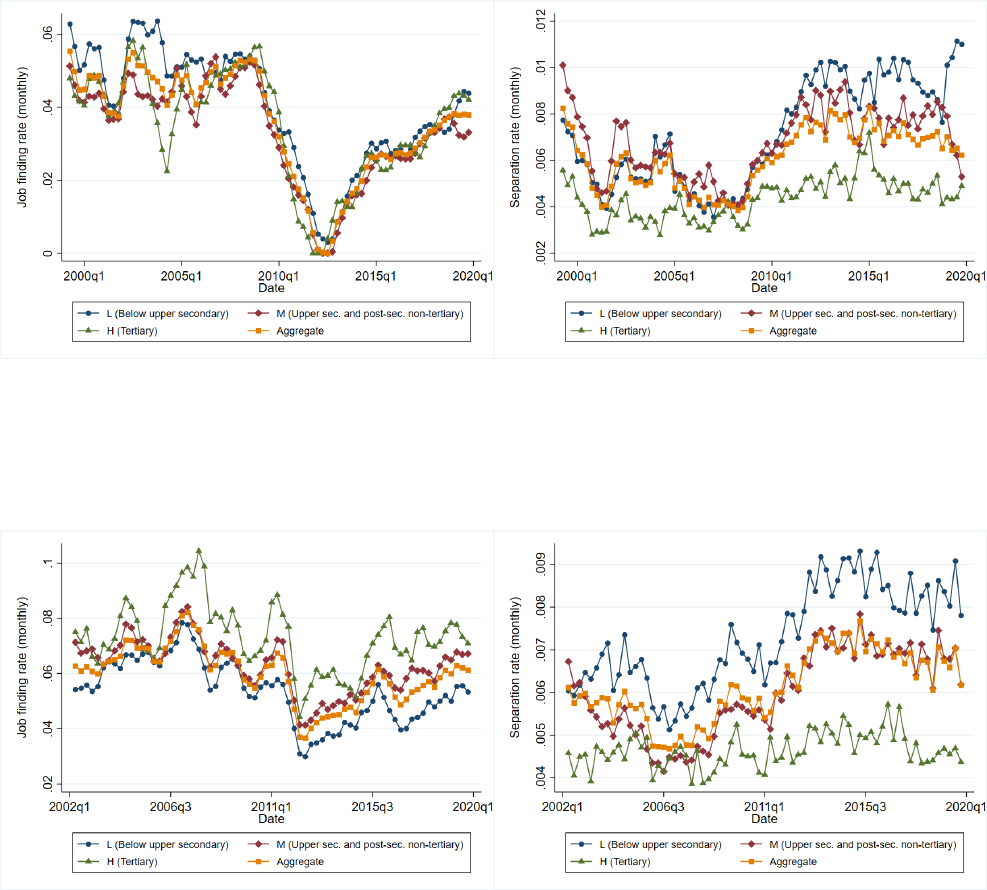

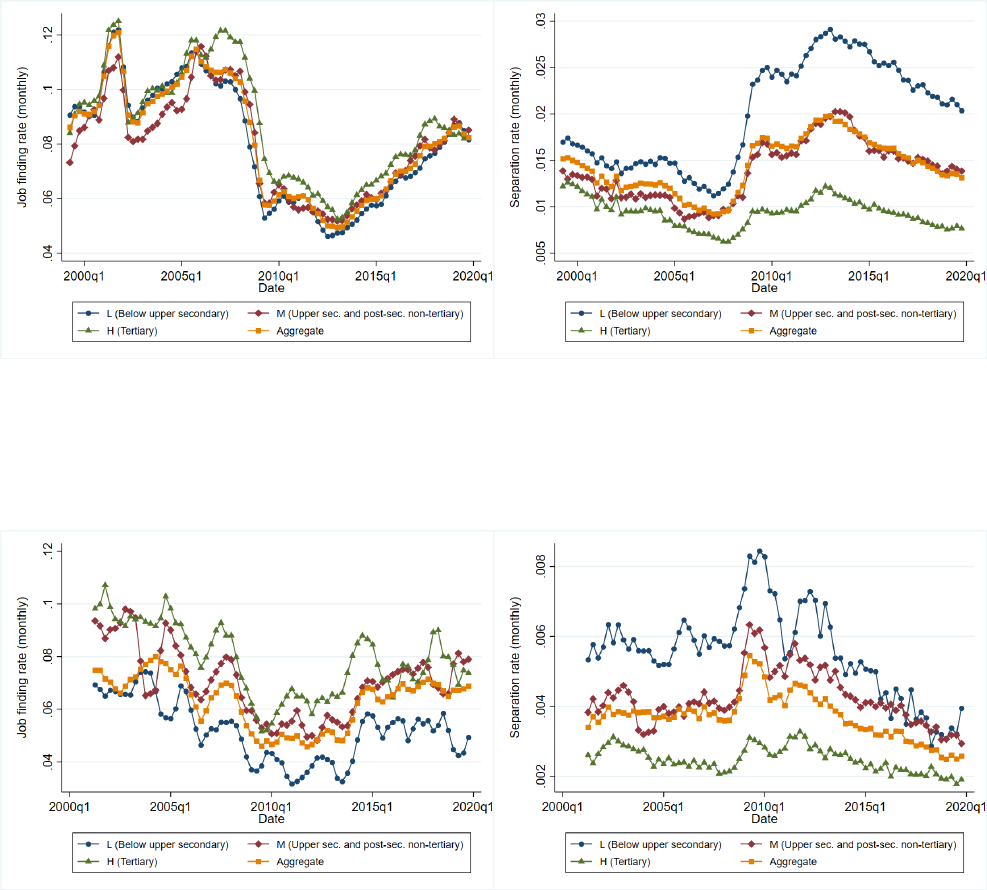

separation rates is consistent with the notion that the risk of becoming unemployed, and

not finding a job quickly once unemployed, is higher for workers with lower educational

attainment.

9

2.1.1 Cyclical properties of job finding and separation rates

Further characteristics that are of interest are the volatility and cyclical behaviour of the

estimated job finding and separation rates.

Table 4 reports the standard deviation and correlation of the cyclical components of the

estimated job finding rates with the cyclical component of the total unemployment rate.

10

Three characteristics stand out. First, the job finding rates of the least educated (L) tend

to be more volatile in some countries (France, Germany, the UK) than job finding rates of

those with better education, especially when considering unemployment for each particular

educational attainment level (note that the highest education level, H, is quite volatile mainly

because of very small samples for this segment, so the results should be interpreted with cau-

tion).

11

Second, job finding rates at all educational levels are procyclical (they are negatively

correlated with unemployment). Third, there is considerable heterogeneity across countries

regarding the cyclical properties across educational attainment levels. In Germany, the M and

9

In Appendix A.1, we also plot monthly job finding f

<d

t

and separation rates s

<d

t

by educational attainment

across selected European countries for different unemployment duration spells.

10

Cyclical components were obtained using the Hodrick-Prescott filter with the smoothing coefficient of 1600,

applied to average monthly rates in the quarter, as in Fujita and Ramey (2009).

11

While we do not emphasise this aspect here, job finding rates for the least educated tend to also be highly

seasonal, especially in countries of Southern Europe. This is another indication that this segment of the labour

market features more risky jobs than the other segments.

ECB Working Paper Series No 2850

10

H educational levels are almost acyclical; in Italy, L is mildly procyclical, and M and H are

more procyclical than L. Similarly, procyclicality tends to increase mildly with educational at-

tainment in Spain, while in Greece, all educational levels are similarly procyclical. In France,

Germany, and the UK, lower educational attainment levels tend to be more procyclical.

Table 4: Cyclical properties of job finding rates

Rel.

own v

ol. Rel. aggregate vol. Corr. with agg.

σ( f

i

)/σ(U

i

) σ( f

i

)/σ(U) unemployment

Countr

y Sample L

M H L M H L M H

France

2003Q1-2019Q4 13.93 11.38

14.19 14.96 11.80 19.01 -0.61 -0.43 -0.56

Germany 2005Q1-2019Q4 16.51 12.58 16.03 15.86 13.99 22.98 -0.46 -0.19 -0.08

Greece 1998Q1-2019Q4 8.08 5.92 9.15 7.75 6.37 9.69 -0.39 -0.42 -0.41

Italy 2001Q1-2019Q4 11.38 12.12 16.67 11.83 12.04 19.17 -0.23 -0.41 -0.50

Spain 1998Q1-2019Q4 8.52 10.46 10.84 9.08 9.84 10.84 -0.59 -0.71 -0.80

UK 2000Q1-2019Q4 12.76 12.28 11.21 11.36 13.78 15.40 -0.34 -0.42 -0.26

Notes: The table reports standard deviations of cyclical components of monthly job finding rates relative to the

standard deviation of the cyclical component of each group’s unemployment U

i

, aggregate unemployment U,

and correlations of cyclical components of monthly job finding rates with the cyclical component of aggregate

unemployment, all based on d = 3 estimates. L = Less than primary, primary, and lower secondary education,

M = Upper secondary and post-secondary non-tertiary education, and H = Tertiary education. We end the

sample in Q4 2019 to exclude the COVID-19 period.

The same set of cyclical statistics as for the job finding rates is reported in Table 5 for

separation rates. Several results stand out. First, separation rates are less volatile than job

finding rates relative to all unemployment measures. Second, separation rates for the lowest

educational attainments tend to be much more volatile than those for higher educational

attainment levels. Third, in particular for Germany and France and to a lesser degree for the

UK, separation rates at the lower educational attainment levels are acyclical.

2.1.2 Contributions of job finding and separation rates to unemployment fluctuations

An important question is which rate, the job finding rate or the separation rate, contributes

more to the unemployment rate fluctuations over the business cycle. Following Fujita and

Ramey (2009), we decompose unemployment variability into contributions from the job find-

ing and separation rates.

12

Specifically, Shimer (2012) shows that if the job finding and separa-

tion rates are constant during a period t, then the corresponding equilibrium unemployment

rate can be computed using job finding and separation rates as u

ss

t

= s

t

/(s

t

+ f

t

). If trend

components are denoted by a bar, then the deviations of unemployment from the trend can

be written as

ln

u

ss

t

u

ss

t

= (1 − u

ss

t

)ln

s

t

s

t

− (1 − u

ss

t

)ln

f

t

f

t

!

+ ε

t

, (7)

12

The implicit assumption is that the educational attainment of workers does not change materially at business

cycle frequencies.

ECB Working Paper Series No 2850

11

Table 5: Cyclical properties of separation rates

Rel. own vol. Rel. aggregate vol. Corr. with agg.

σ(s

i

)/σ(U

i

) σ(s

i

)/σ(U) unemployment

Country Sample L M H L M H L M H

France 2003Q1-2019Q4 1.02 0.83 0.29 1.10 0.86 0.39 -0.08 0.06 0.26

Germany 2005Q1-2019Q4 1.47 0.74 0.32 1.41 0.83 0.46 0.01 0.65 0.52

Greece 1998Q1-2019Q4 0.71 0.91 0.58 0.68 0.98 0.52 0.41 0.34 0.21

Italy 2001Q1-2019Q4 0.65 0.51 0.44 0.67 0.51 0.51 0.66 0.69 0.44

Spain 1998Q1-2019Q4 1.27 0.93 0.50 1.36 0.87 0.50 0.82 0.81 0.81

UK 2000Q1-2019Q4 0.81 0.50 0.28 0.72 0.56 0.38 0.23 0.47 0.66

Notes: The table reports standard deviations of cyclical components of monthly separation rates relative to the

standard deviation of the cyclical component of each group’s unemployment U

i

, aggregate unemployment U,

and correlations of cyclical components of monthly separation rates with the cyclical component of aggregate

unemployment, all based on d = 3 estimates. L = Less than primary, primary, and lower secondary education,

M = Upper secondary and post-secondary non-tertiary education, and H = Tertiary education. We end the

sample in Q4 2019 to exclude the COVID-19 period.

where ε

t

is the residual term. The above equation can be more compactly written as

du

ss

t

= du

sr

t

+ du

j f r

t

+ ε

t

, (8)

where du

sr

t

and du

j f r

t

are the contributions of the separation rate and the job finding rate,

respectively. The variance of du

ss

t

is then

Var(du

ss

t

) = Cov(du

ss

t

, du

sr

t

) + Cov(du

ss

t

, du

j f r

t

) + Cov(du

ss

t

, ε

t

). (9)

This can be used to attribute the share of cyclical variation in unemployment rate that

is explained by the cyclical variations of the job finding rate β

j f r

, the cyclical variation of the

separation rate β

sr

, and the cyclical variation of the residual β

ε

:

β

j f r

=

Cov(du

ss

t

, du

j f r

t

)

Var(du

ss

t

)

, β

sr

=

Cov(du

ss

t

, du

sr

t

)

Var(du

ss

t

)

, and β

ε

=

Cov(du

ss

t

, ε

t

)

Var(du

ss

t

)

. (10)

Table 6 reports the estimates of the contributions of the job finding rate and the separa-

tion rate to cyclical fluctuations of unemployment rates (note that β

j f r

+ β

sr

+ β

ε

= 1). The

key finding is that in all countries, fluctuations in the job finding rate are the main contributor

to cyclical fluctuations in the unemployment rate. Moreover, this is overwhelmingly the case

for all countries at the lowest education level, where fluctuations in the job finding rate typi-

cally explain more than half (and often more than 80%) of the fluctuations in unemployment

rates, and more than the share explained by the cyclical fluctuations of the separation rate.

These findings are broadly in line with the empirical evidence for Europe. Slacalek et al.

(2020) suggest that, based on unconditional estimates, the elasticities of employment responses

of hand-to-mouth households, and in particular of poor hand-to-mouth households, tend to

be large. While the estimates vary across countries, the sensitivity of employment of poor

ECB Working Paper Series No 2850

12

Table 6: Contributions to cyclical variation of unemployment

β

j f r

β

sr

Country Sample L M H L M H

France 2003Q1-2019Q4 0.96 0.69 0.92 0.01 0.32 0.07

Germany 2005Q1-2019Q4 0.87 0.48 0.55 0.09 0.49 0.44

Greece 1998Q1-2019Q4 0.39 0.41 0.40 0.19 0.18 0.05

Italy 2001Q1-2019Q4 0.80 0.85 0.86 0.14 0.17 0.10

Spain 1998Q1-2019Q4 0.52 0.60 0.68 0.41 0.35¸ 0.28

UK 2000Q1-2019Q4 0.64 0.64 0.63 0.31 0.33 0.35

Notes: The table reports contributions of the fluctuations of the job finding rate β

j fr

and of the separation rate

β

sr

to cyclical fluctuations of the unemployment rate. All is based on d = 3 estimates. L = Less than primary,

primary, and lower secondary education, M = Upper secondary and post-secondary non-tertiary education, and

H = Tertiary education. β

j fr

and β

sr

do not add up to 1 due to the variance contribution of the residual.

hand-to-mouth households is at least 1.5-times larger than the aggregate employment. A sim-

ilar finding is reported by Dossche and Hartwig (2019), who look at “worker betas” across

the income distribution and find significantly higher worker betas in the lowest household

income quintile. This elasticity can be up to four times higher in the lowest quintile than

in the highest quintile. Kramer (2022) studies the procyclicality of earnings growth in Ger-

many and finds that the procyclicality is mostly driven by transitions from nonemployment

to employment (i.e. job finding rates), especially at the bottom of the income distribution.

Moreover, he finds that individuals at the bottom of the income distribution have lower job

finding rates than wealthy individuals and are more exposed to business cycle fluctuations.

Both findings are in line with what we find for Germany based on the aggregate data. Em-

pirical evidence conditional on a monetary policy shock (Lenza and Slacalek (2018) and Broer

et al. (2022)) also suggests that in Europe, incomes of poor households tend to react more

strongly to a monetary policy than the incomes of wealthier households.

2.2 Evidence from the US

For the US, compared to European countries, we have more detailed data along several di-

mensions. First, we have more granular data in terms of educational attainment level. Second,

data on new hires includes hires from inactivity. Finally, we also have some evidence that

wages at lower educational attainment are more rigid than wages at higher educational at-

tainment levels.

13

The latter will turn out to be important for the quantitative results in the

model.

We use publicly available Longitudinal Employer-Household Dynamics (LEHD) data

from the US Census Bureau. The LEHD database is constructed from various administra-

tive sources, such as Quarterly Census of Employment and Wages, Unemployment Insurance

earnings data, surveys and censuses. All the data we use are quarterly, seasonally adjusted

13

This is the main reason why we report the empirical evidence for the US in a separate subsection.

ECB Working Paper Series No 2850

13

and cover period between 2000Q2 and 2017Q3. If not otherwise stated, (net) hires and sepa-

rations are expressed as a share of employment.

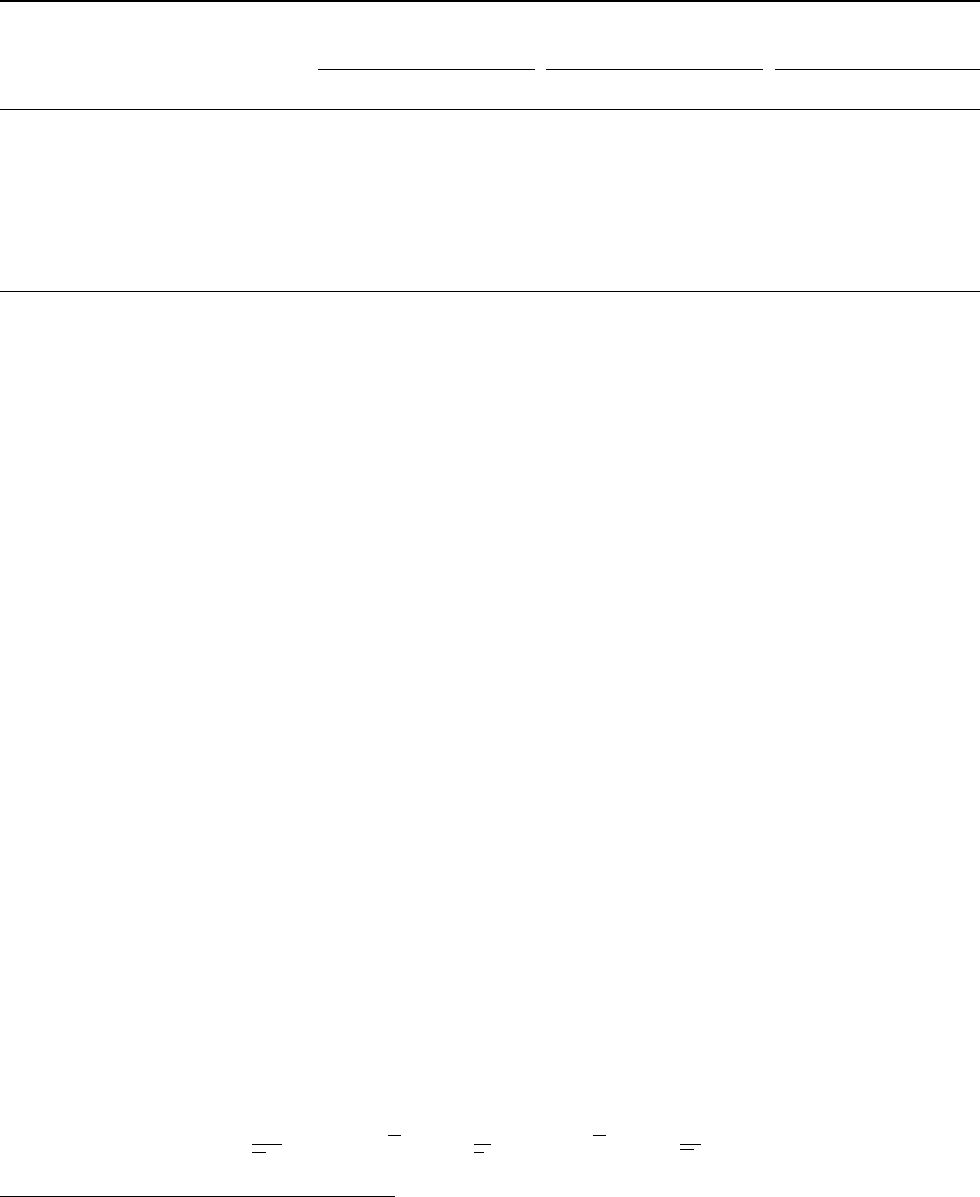

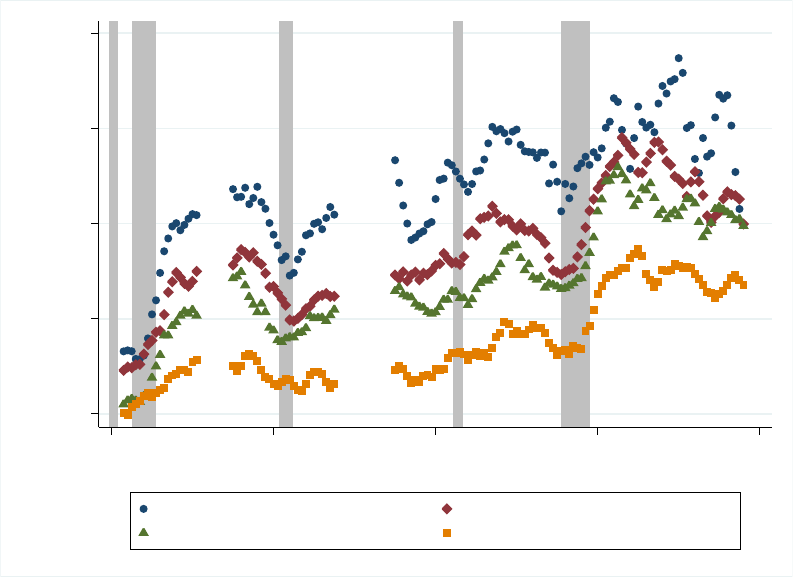

Figures 1a and 1b plot hires from, and separations to, persistent nonemployment across

education groups. One can observe that the hiring rate and separation rate are inversely

related to educational attainment, i.e., less educated workers have larger inflow and outflow

rates to persistent nonemployment.

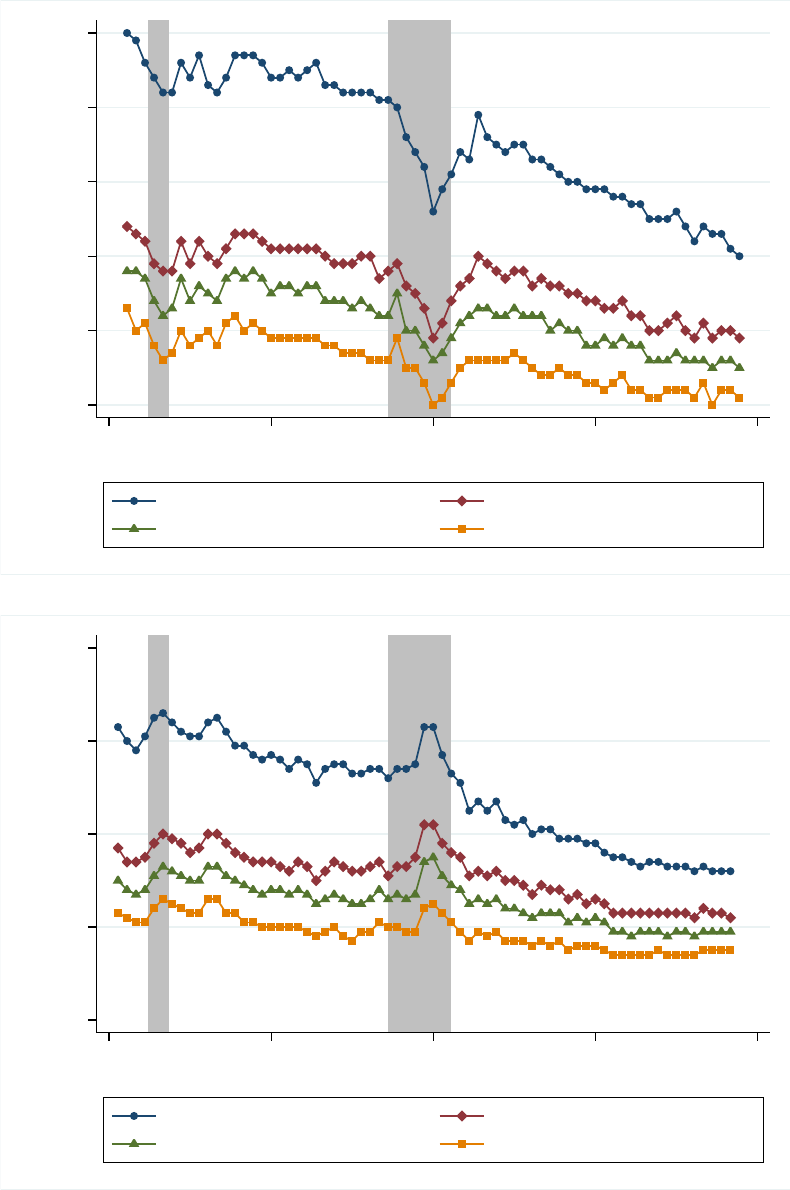

To get a clearer picture of who is more affected by business cycle fluctuations, we look

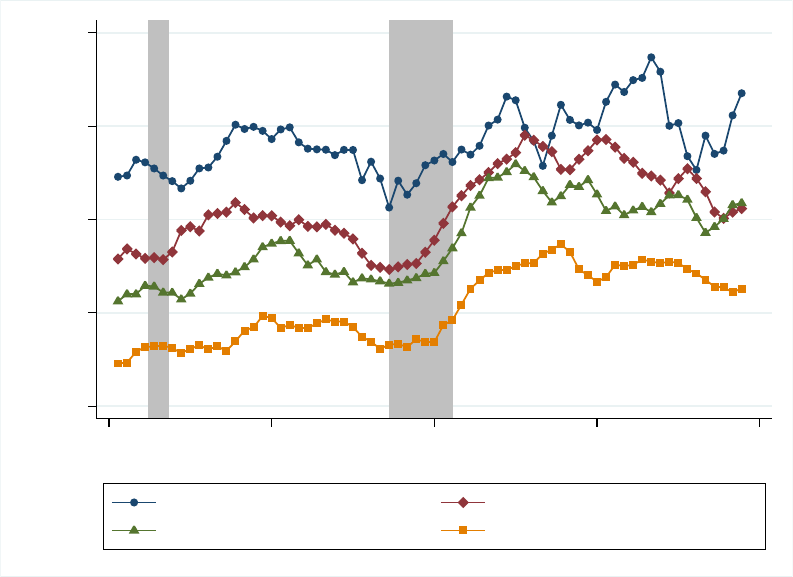

at the difference between the two rates. Figure 2 shows net worker flows—hires minus

separations—by educational attainment. It shows that during the recession, net hiring for

the group of workers with the lowest educational attainment declined much more than for

the group with the highest educational attainment; during downturns, the less educated

segments of the labour market experience more adverse developments than segments for the

more educated. This pattern is particularly notable during the Great Recession when the

net hiring for the group with less than high school dropped by more than twice as much as

for the group with the bachelor’s or higher degree. While less extreme, the same pattern is

observed during the milder 2001 recession.

Notably, at the onset of recovery, the net hiring in the groups with the lowest educational

attainment is also the one that exhibits the largest jump upwards. Again the pattern is such

that the upward jumps are more extreme for the less educated groups, and the magnitudes of

the increases decrease with education. This indicates that the groups with lower education,

while being those that are most exposed to the net job loss in the recession, are also the

groups who are the most exposed to net job gain when the recession is over.

Table 7 shows summary statistics for our sample. Less educated workers experience

larger inflow and outflow rates to nonemployment, and these rates are also more volatile.

This confirms that less educated workers face a higher risk of going to, or coming from,

nonemployment. For example, the rate of hires and separations for the workers in the lowest

education group is two to three times larger than for the workers in the highest education

group, and the volatilities of these rates are about three times higher for the least educated

than for the most educated.

With the LEHD data, we, unfortunately, cannot calculate job finding rates, but only their

proxies across education groups. The reason is that a job finding rate is defined as a ratio

of unemployed workers who find a job over the number of unemployed. However, in the

LEHD data, we observe only hires from nonemployment, which is a broader concept than

unemployment, as it also includes workers who are not in the labour force. Nevertheless, we

report these ”rates” (expressed as a share of an average employment within the education

group) in the last row of Table 7, as they at least give some notion of the ranking of these

rates between education groups. Note that these proxies for job finding rates are increasing

with educational attainment (except for the group of less than high school, but this group is

very small in the data).

To further investigate whether workers with low(er) educational attainment face larger

ECB Working Paper Series No 2850

14

Figure 1: Hires and Separations to persistent nonemployment

(a) Hires

.03 .04 .05 .06 .07 .08

Hires from NonE

2000q1 2004q3 2009q1 2013q3 2018q1

date

Less than high school High school or equivalent, no college

Some college or Associate degree Bachelor’s or advanced degree

(b) Separations

.02 .04 .06 .08 .1

Separations to NonE

2000q1 2004q3 2009q1 2013q3 2018q1

date

Less than high school High school or equivalent, no college

Some college or Associate degree Bachelor’s or advanced degree

Notes: A worker is defined as being a Hire from Persistent Nonemployment in quarter t, if she or he had no

main job in the beginning of the quarter t-1 and t, but had one at the end of quarter t. A worker is defined as

undergoing a Separation to Persistent Nonemployment in quarter t, if she or he, had a main job in the beginning

of quarter t, and not at the end of quarter t or quarter t+1. Everything is expressed as a share of an average

employment within the education group. Shaded areas denote NBER recessions.

ECB Working Paper Series No 2850

15

Figure 2: Net hires from persistent nonemployment

-.03 -.02 -.01 0 .01

Hires less Separations to NonE

2000q1 2004q3 2009q1 2013q3 2018q1

date

Less than high school High school or equivalent, no college

Some college or Associate degree Bachelor’s or advanced degree

Notes: Net hires is calculated as the difference between hires from and separations to persistent nonemploy-

ment, and it is expressed as a share of an average employment within the education group. Shaded areas denote

NBER recessions.

Table 7: Summary statistics

High

school or S

ome college or Bachelor’s degree or

Less than high school equivalent, no college Associate degree advanced degree

mean

sd mean sd

mean sd mean sd

Hir

es 0.066 0.0084 0.046

0.0043 0.041 0.0038 0.035 0.0032

Separations 0.069 0.011 0.051 0.0056 0.045 0.0045 0.038 0.0035

Hires less Separations -0.0025 0.0062 -0.0042 0.0045 -0.0035 0.0037 -0.0029 0.0030

Job finding rate proxy 0.782 0.218 0.614 0.187 0.714 0.294 0.776 0.350

Notes: (Net) hires and separations are rates and are expressed as a share of an average employment within the

education group.

ECB Working Paper Series No 2850

16

countercyclical employment risk, we estimate the following equation

Y

i,t

= γ

t

+ β

1

educ

i

+ β

2

educ

i

× X

t

+ ϵ

i,t

, (11)

where Y

i,t

is either the (net) hire or separation rate, X

t

is the cyclical component of GDP,

14

educ

i

is workers’ educational attainment, γ

t

are time dummies to control for common shocks,

and ϵ

i,t

is the residual term. What we are interested in is the coefficient on the interaction

term, which measures the differential responsiveness - across education groups - of net hiring

rate to a business cycle. Note that results have to be interpreted relative to the highest

education group.

15

Table 8: Worker flows over the business cycle

(1)

(2) (3)

VARIABLES Net

hires Hires Separations

Less

than high school 0.000

0.030*** 0.030***

(0.000) (0.001) (0.001)

High school or equivalent, no college -0.001*** 0.011*** 0.012***

(0.000) (0.000) (0.000)

Some college or Associate degree -0.001** 0.006*** 0.007***

(0.000) (0.000) (0.000)

Less than high school × GDP cycle 0.123*** 0.079** -0.018

(0.036) (0.037) (0.056)

High school or equivalent, no college × GDP cycle 0.070*** 0.018 -0.044

(0.024) (0.019) (0.029)

Some college or Associate degree × GDP cycle 0.037 0.003 -0.031

(0.025) (0.020) (0.032)

T

ime FE X X

X

Observations 272 276 276

R-squared 0.9028 0.9713 0.9468

Robust

standard err

ors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Notes: (Net) hires, and separations are rates and are expressed as a share of an average employment within the

education group.

Table 8 reports the results from estimating Equation 11. Column 1 shows that the net hir-

ing rate of less educated workers is more sensitive to business cycles than the net hiring rate

of workers with the highest level of educational attainment. This implies that (countercycli-

cal) employment risk is the largest for the least educated workers, and it falls with increasing

educational attainment. Results are in line with Haltiwanger et al. (2018), who find that

during recessions, workers with lower education are more likely to exit to nonemployment.

They also find that conditional on firm productivity groups, hires and separations are more

cyclically sensitive for less educated workers. In columns 2 and 3, we separate the net hiring

14

We obtain it after applying the Hodrick-Prescott filter to a logarithm of seasonally adjusted real GDP. In

Appendix B.2, we also consider other business cycle measures, i.e. NBER recession episodes and the cyclical

component of the level of unemployment. The results do not materially change.

15

That is, relative to workers with a bachelor’s degree or an advanced degree.

ECB Working Paper Series No 2850

17

rate into hires and separations to see which margin is more important. We find that only

hires are significantly different across education levels; the hiring rate for the least educated

workers is more cyclically sensitive than for the workers with the highest education.

16

In

Appendix Table 18, we also estimate the sensitivity of changes in (net) hires and separation

rates to changes in GDP across education groups. Results confirm our previous findings that

changes in (net) hiring rates of workers with lower education tend to be more sensitive to

changes in GDP, implying that they face larger employment and, therefore, income risk than

more educated workers.

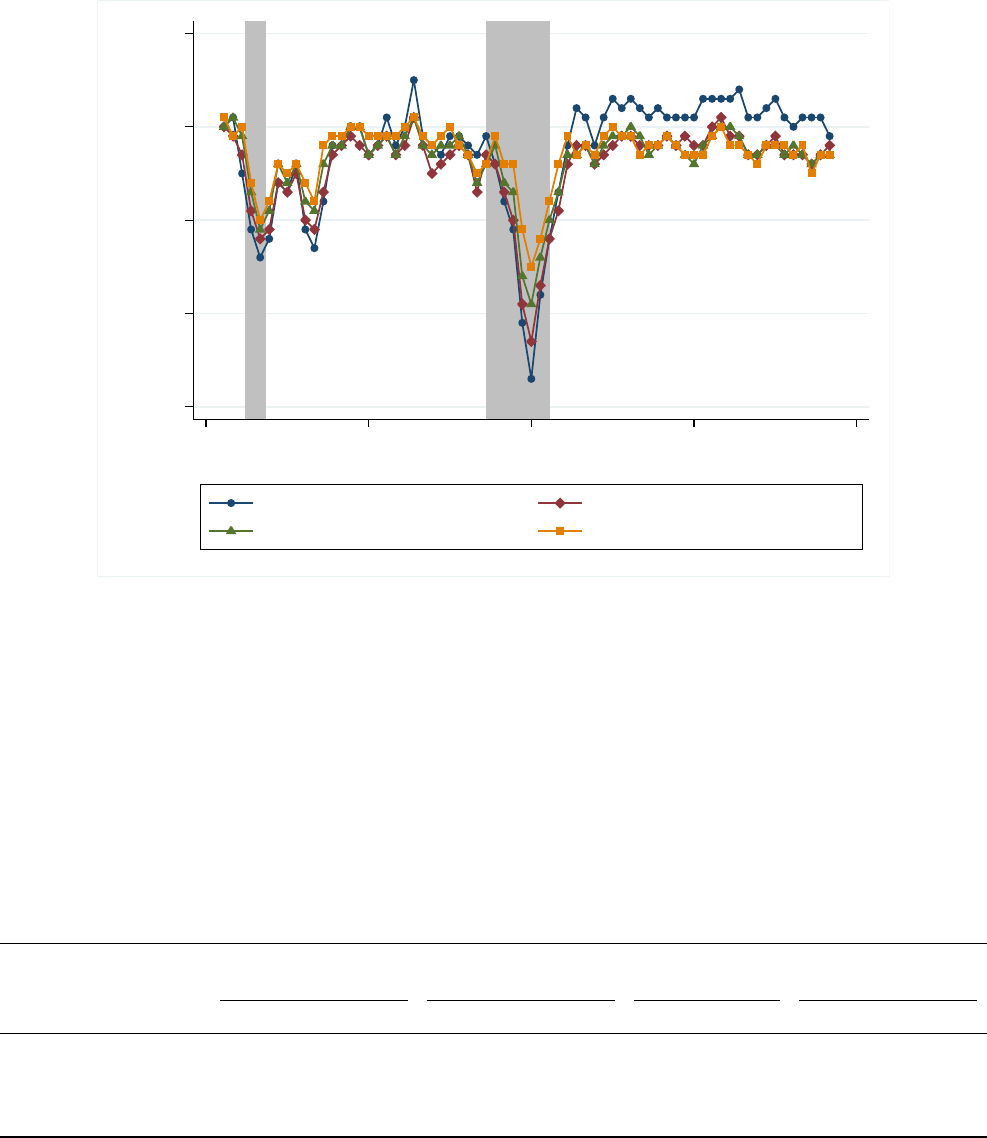

2.2.1 Wage rigidity

For the US, we also have some evidence of differential wage rigidity across educational at-

tainment levels, which we lack for European countries.

Figure 3 plots the data from the matched Current Population Survey dataset (see Daly

et al. (2012)). The figure shows the percentage of workers who reported no change in their

wages over the past year by educational attainment. It shows that wages of less educated

workers tend to be stickier than wages of more educated workers. This regularity holds over

all business cycle phases and over a long time span.

17

While these data do not cover new

hires, they indicate that labour market segments by educational attainment have different

properties. More recent evidence of differential wage rigidity for new hires across education

levels is Doniger (2019), who finds (i) wages for new hires of least educated workers to

be acyclical, and that (ii) wage (pro)cyclicality increases with the educational attainment.

She also finds that after a monetary policy shock, less educated workers respond on the

employment margin while the more educated respond on the wage margin.

18

3 Model

To capture the characteristics of labour market segments described above and to investigate

their influence on the effectiveness of monetary policy, we build a small stylised model.

The core of the model is the heterogeneous agents New Keynesian model of McKay and

Reis (2016) and McKay et al. (2016), which we augment with search frictions on the labour

market. To account for the different labour market prospects faced by individual households,

we model each labour income level as its own labour market segment.

We assume that each labour market segment is populated by a continuum of households

and a continuum of labour firms. Labour firms post vacancies and households decide how

16

Interestingly, when we run regression on NBER recession episodes (see Table 16 in Appendix B.2), we find

a statistically significant difference in separation rates among education groups; low educated workers have

larger separation rates during downturn(s) relative to highly educated workers.

17

See Figure 31 in Appendix B.1 for the full sample.

18

In contrast, Haefke et al. (2013) and Kudlyak (2014) find no evidence of nominal wage rigidity for new

hires, however as pointed out by Doniger (2019), they investigate a representative agent setting and do not

differentiate across educational attainment.

ECB Working Paper Series No 2850

18

Figure 3: Wage rigidity by educational attainment

5 10 15 20 25

Nominal wage rigidity

2000q1 2004q3 2009q1 2013q3 2018q1

date

Less than high school High school or equivalent, no college

Some college or Associate degree Bachelor’s or advanced degree

Notes: Percentage of workers who saw no change in their wage over the past year by educational attainment.

Source: https://www.frbsf.org/economic-research/indicators-data/nominal-wage-rigidity/

many workers to send searching for jobs. Job search is subject to search frictions, and firms

and households take matching probabilities as given when deciding on how many vacancies

to post or how many workers to send to the market.

Markets are incomplete, and there is heterogeneity between households, but full insur-

ance within each household. Each household consists of a continuum of workers who have

the same level of labour productivity (educational attainment) and can be either employed or

unemployed. At the end of each period, workers bring their incomes home and the house-

hold as a whole decides on how much to consume and save, subject to prices and job finding

probabilities. This simplification allows us that, within a household type, we can use the av-

erage rates of employment, unemployment, matching probabilities, and wages. In addition,

if there are no unemployment benefits available, this assumption also prevents households

with no assets from having zero consumption. Note that this assumption still preserves the

cyclical risk of household income as a whole.

The household sends its workers to search for work at the beginning of each period.

They either find work, in which case they bring home earnings, or they remain unemployed

and receive unemployment benefits (if any). At the end of the period, all jobs terminate, and

the search starts again in the next period. This assumption allows us to avoid an additional

state variable (employment) for each labour market segment. Because we have three labour

market segments, this would add three additional endogenous state variables to the already

existing one endogenous continuous variable (asset holdings) and one exogenous (labour

ECB Working Paper Series No 2850

19

productivity process). Note that even in this case, the persistence of employment is implied

by the job finding probability in the labour market segment. That is, in segments with higher

job finding probabilities, employed workers are more likely to remain employed, even if they

separate every period, because they are more likely to find a new job at the beginning of the

next period. That is, we can mimic income risk (and its fluctuations) in each labour market

segment by the level and fluctuations of the job finding probability.

The remainder of the model is similar to McKay et al. (2016). In the main text, we only

report the equations related to the search and matching frictions on the labour market in the

model, while the remaining equations are reported in Appendix C. The economy is populated

by a continuum of ex-ante identical households who face the following decision problem:

V

t

(b

h,t

, z

h,t

) = max

c

h,t

,b

h,t+1

,s

h,t

,l

h,t

,u

h,t

c

1−γ

h,t

1 − γ

− η

1

s

1+η

2

h,t

1 + η

2

+ β

∑

z

h,t+1

P

(

z

h,t+1

|z

h,t

)

V

t+1

(b

h,t+1

, z

h,t+1

)

subject to

c

h,t

+

b

h,t+1

1 + r

t

= b

h,t

+ Bu

h,t

+ w

h,t

l

h,t

− τ

z

h

,t

+ Π

z

h

,t

, (12)

s

h,t

= l

h,t

+ u

h,t

, (13)

l

h,t

= p

W

z

h

,t

s

h,t

, (14)

u

h,t

= (1 − p

W

z

h

,t

)s

h,t

, (15)

and

b

h,t+1

≥ 0. (16)

Here, c

h,t

is consumption of household with the educational attainment h at time t, b

h,t

are

its bond holdings at time t, r

t

is the real interest rate, s

h,t

is the number of searching workers

within household h at time t, l

h,t

is the number of employed workers within household h at

time t, u

h,t

is the number of unemployed workers within household h at time t, w

h,t

is the

real wage, and B are unemployment benefits. τ

z

h

,t

are taxes (levied as lump-sum depending

on the household’s labour endowment, and Π

z

h

,t

are profits from intermediate goods firms

and labour firms.

19

P

(

z

h,t+1

|z

h,t

)

is the (exogenous) probability of transitioning between

labour market segments, and it follows a Markov process. The households take prices, taxes,

dividends, and unemployment benefits as given.

We assume that all intermediate goods firms are held by an investment fund managed by

a risk-neutral manager, who collects profits and distributes them as dividends to households

(households cannot trade in equities). Households are allowed to save by holding and trading

19

We assume that profits from labour firms are given back to households as lump-sum but in proportion to

employment.

ECB Working Paper Series No 2850

20

riskless real bonds issued by the government. These bonds are in positive and constant net

supply, so households can partially self-insure by saving.

A household’s optimisation gives the following first-order conditions with respect to the

choice variables

c

h,t

−γ

− λ

h,t

= 0, (17)

−

c

h,t

−γ

1 + r

t

+ β

∑

z

h,t+1

P

(

z

h,t+1

|z

h,t

)

V

′

t+1

(b

h,t+1

, z

h,t+1

) = 0, (18)

−η

1

s

η

2

h,t

+ p

W

h,t

q

h,t

− µ

h,t

+ (1 − p

W

h,t

)ξ

h,t

= 0, (19)

−q

h,t

+ µ

h,t

+ λ

h,t

w

h,t

= 0, (20)

−ξ

h,t

+ µ

h,t

+ λ

h,t

B = 0, (21)

where λ

h,t

is the multiplier on (12), µ

h,t

on (13), q

h,t

on (14), and ξ

h,t

on (15).

By eliminating the Lagrange multiplier on the budget constraint and applying the enve-

lope theorem, we get the standard Euler equation

c

h,t

−γ

= β(1 + r

t

)

∑

z

h,t+1

P

(

z

h,t+1

|z

h,t

)

(c

h,t+1

−γ

). (22)

3.1 Labour market

Labour market segments. There is a separate labour market for each productivity type

of households (in total, there are three labour market segments). On each labour market

segment, indexed by the productivity type z

h

, we have a separate matching function and

matching probabilities:

m

z

h

,t

= ϕ

z

h

s

µ

z

h

z

h

,t

v

1−µ

z

h

z

h

,t

, (23)

where m

z

h

,t

is the number of matches in the market z

h

, ϕ

z

h

is the labour-market-segment-

specific matching efficiency, s

z

h

,t

is the number of searching workers, and v

z

h

,t

is the number

of vacancies. µ

z

h

is the elasticity of the matching function with respect to the number of

searching workers.

The matching probability for the worker, p

W

z

h

,t

, is

p

W

z

h

,t

=

m

z

h

,t

s

z

h

,t

= ϕ

z

h

v

z

h

,t

s

z

h

,t

1−µ

z

h

= ϕ

z

h

(

θ

z

h

,t

)

1−µ

z

h

, (24)

and the matching probability for the firm, p

F

z

h

,t

, is

ECB Working Paper Series No 2850

21

p

F

z

h

,t

=

m

z

h

,t

v

z

h

,t

= ϕ

z

h

v

z

h

,t

s

z

h

,t

−µ

z

h

= ϕ

z

h

(

θ

z

h

,t

)

−µ

z

h

. (25)

Households’ labour supply. Households send workers to search until the cost of searching

(measured in monetary terms) is equal to the expected earnings from searching. Rearranging

(17), (19), (20) and (21) delivers

η

1

(l

h,t

+ u

h,t

)

η

2

c

−γ

h,t

= p

W

h,t

w

h,t

+ (1 − p

W

h,t

)B, (26)

where (l

h,t

+ u

h,t

) ≡ s

h,t

is the total amount of workers the household sends in the beginning

of the period to the labour market to search for jobs, c

−γ

h,t

is the marginal utility of consump-

tion, p

W

z

h

,t

is a fraction of workers who find a job and earn real wage w

z

h

,t

, and (1 − p

W

z

h

,t

) is a

fraction of workers who do not find a job, but receive unemployment benefits B. Condition

26 says that in equilibrium, the disutility of searching (measured in monetary terms) has to

be equal to the expected earnings from searching. The latter are weighted average of the ex-

pected real wage and unemployment benefits, where the weight is the probability of getting

a job.

20

The setting of the model makes it clear where the sources of income fluctuations come

from. The first source, which is due to idiosyncratic labour productivity shocks that shift

households between labour market segments, is acyclical. These shocks can be thought of as

shocks that make a particular skill either more sought-after or less desired on the market.

21

This type of risk is fully taken into account by the households in our model. The second

type of income fluctuation in our model is cyclical and comes from different labour market

conditions in labour market segments. These conditions depend on the state of the business

cycle and, in our model differ across the labour market segments. Because of these differ-

ences, transition from one labour market segment to the other implies a different gain or loss

of income, depending on the state of the business cycle.

Labour firms. We assume that each productivity segment of the labour market is populated

by a continuum of its own labour firms. Labour firms hire workers and sell their effective

labour as a homogeneous good at a competitive aggregate wage ω

t

to the intermediate-goods

firms. Each labour firm employs one worker. The value function of the labour firm is

J

z

h

,t

= ω

t

z

h,t

− w

z

h

,t

, (27)

where ω

t

z

h,t

is the total revenue received by the labour firm from selling labour services (one

worker provides labour services corresponding to his productivity z

h,t

, which is sold to the

20

Equation (26) also nests standard labour supply model; if p

W

z

h

,t

= 1, so that everyone finds a job (implying

u

h,t

= 0), and B = 0, it reduces to the standard labour supply condition.

21

For example, automation in some industries have made workers with skills that can be automated less

sought-after, and workers who can program the machinery used for automation of these jobs more sought-after.

ECB Working Paper Series No 2850

22

intermediate-goods firm at the rate ω

t

). The labour firm pays the worker real wage w

z

h

,t

and

returns profits to the household as lump-sum.

The free-entry condition for labour firms is

ψ

z

h

= p

F

z

h

,t

J

z

h

,t

, (28)

where ψ

z

h

is the per-period vacancy posting cost in the labour market segment with produc-

tivity z

h

. In equilibrium, the labour firm’s optimality condition states that the per-period cost

of posting a vacancy is equal to the probability that the firm will find a worker, times the

value of that worker for the firm, which is equal to the profit the firm will earn in this period.

Wage determination. We consider two settings for wage determination. When wages are

fully flexible, we assume that the wage rate that is paid to the workers in each segment is

a fraction (1 − α

z

h

) of the aggregate wage cost (which is the revenue received by the labour

firm),

w

z

h

,t

= (1 − α

z

h

)ω

t

z

h,t

. (29)

The aggregate wage cost is determined in equilibrium as the cost that equates the labour

demand from intermediate goods firms with the labour services’ supply from labour firms.

When we analyse a setting with rigid wages, we follow Hall (2005) and model wage

rigidity as a weighted average of the wage that would be determined in the current period

(as described above), and a wage norm. For the wage norm we take the steady-state wage.

22

We allow wage rigidity to differ across labour market segments. The rigid wage is then

w

z

h

,t

= [(1 − ω

R

)(1 − α

z

h

)ω

t

+ ω

R

(1 − α

z

h

)ω]z

h,t

, (30)

where ω

R

∈ [0, 1] is the weight of the wage norm in wage determination, and (1 − α

z

h

)ω is

the wage norm.

Relation to Nash bargaining. Here we show that our flexible wage rule is just a particular

case of the standard Nash bargaining. With Nash bargaining, the wage is the outcome of

bargaining between workers and firms regarding the split of the total surplus generated by a

successful match. The solution to the Nash bargaining problem is

χ

z

h

J

z

h

,t

= (1 − χ

z

h

)(W

E

z

h

,t

− W

N

z

h

,t

), (31)

where χ

z

h

∈ (0, 1), is the bargaining power of the worker that can be labour-market-segment-

specific,

23

J

z

h

,t

is the value of a job for a firm, and W

E

z

h

,t

, W

U

z

h

,t

are the value functions of being

employed and unemployed. The value functions for a firm and a worker are

22

This allows us to avoid introducing past wage as an additional state variable.

23

With χ

z

h

= 1, firms would have zero profits (all the surplus goes to workers), but would still have to pay

positive vacancy posting costs which would prevent them from posting any vacancies.

ECB Working Paper Series No 2850

23

J

z

h

,t

= ω

t

z

h,t

− w

z

h

,t

, (32)

W

E

z

h

,t

= w

z

h

,t

− η

1

(l

h,t

+ u

h,t

)

η

2

c

−γ

h,t

, (33)

W

U

z

h

,t

= B − η

1

(l

h,t

+ u

h,t

)

η

2

c

−γ

h,t

. (34)

To get the wage equation, one substitutes (32), (33), and (34) into (31) yielding

w

z

h

,t

= χ

z

h

(ω

t

z

h,t

− B) + B, (35)

which means that the bargained wage a worker receives is equal to the outside option (in

our case unemployment benefits) and a fraction (χ

z

h

) of the surplus from a successful match.

Note that the larger the χ

z

h

, i.e. the larger the bargaining power of the worker, less “sticky”

is the real wage. If we set B = 0, so that there are no unemployment benefits, and define

χ

z

h

≡ (1 − α

z

h

), we get exactly (29).

Finally, in order to see how the wage depends on the labour market developments, we

substitute (28) and (25), together with (33), and (34) into (31) to obtain

w

z

h

,t

=

χ

z

h

1 − χ

z

h

ψ

z

h

ϕ

z

h

(θ

z

h

,t

)

µ

z

h

+ B, (36)

which states that the negotiated wage is increasing in bargaining power of the worker χ

z

h

,

vacancy posting cost (ψ

z

h

), labour market tightness θ

z

h

,t

, and decreasing in matching efficiency

ϕ

z

h

.

3.2 Calibration

The model is quite stylised and we largely rely on standard values from the literature to

calibrate it. However, for the labour market, we do match some of the properties reported in

the empirical section of the paper. In particular, we calibrate the model to match job finding

probabilities by educational attainment and their relative volatility. We also perform several

experiments illustrating how the model properties depend on the calibration choices.

The calibration of production and utility functions follows McKay et al. (2016), and is

reported in Table 9.

Idiosyncratic risk of transiting from one labour market segment to the other is calibrated

using the transition matrix from McKay et al. (2016) who use the persistent component of

wage process from Floden and Lind

´

e (2001), approximated using a 3-state Markov process

with the transition matrix P:

ECB Working Paper Series No 2850

24

Table 9: Utility function and production function

Parameter Value

Risk aversion γ 2

Frisch elasticity (inverse) η

2

2

Disutility weight for labour η

1

1

Markup µ 1.2

Price rigidity θ 0.15

P =

0.966 0.034 0

0.017 0.966 0.017

0 0.034 0.966

This matrix gives rise to the population shares [0.25 0.5 0.25], for each labour market

segment, ”poor”, ”middle”, and ”rich”. These transition probabilities do not vary over the

business cycle so that the mass of households in each segment is constant.

The calibration of the labour market is reported in Table 10. Labour endowment corre-

sponds to the level of wages in each labour market segment and follows McKay et al. (2016).

The differences in wage level also give rise to differences in the wealth distribution, which

reflects, to some extent, the differences in the wage level (hence the labels ”poor”, ”mid-

dle”, and ”rich”). The calibration of matching elasticities relies on the standard values from

Petrongolo and Pissarides (2001). Since wages in Continental Europe and in Germany are

fairly rigid, and since we do not have good data on the differences in the wage rigidity by

educational attainment levels, we assume that the degree of wage rigidity is equal across

all labour market segments.

24

We investigate the implications of this assumption when we

recalibrate the model to US data.

We use the calibration of the entrepreneur’s share and the vacancy posting cost to match

the job finding probability for the typical case where this probability increases by educational

attainment. We have picked the values that very closely correspond to the values found for

Germany. The model is quarterly, and we report quarterly probabilities corresponding to the

monthly rates from Section 2 in Table 12 in the appendix. Because the job finding probability

depends on the ratio of vacancy posting cost and the entrepreneur’s share, we could have

fixed one and used the other to match the job finding probability. However, we wanted also

to match the relative volatility of the labour market segments, which in Germany are more

volatile and much more procyclical for the low-educated (see Table 14 in the appendix). To do

so, we follow the idea in Hagedorn and Manovskii (2008), who propose to solve the puzzle of

low volatility of labour market variables in the standard search-and-matching model (Shimer,

2005) by calibrating the entrepreneur’s share to be small. We set the entrepreneur’s share to

be smaller in the labour market segment with the lowest educational attainment, where we

24

Our choice of wage rigidity calibration implies that wages adjust only by half of what they would if they

were flexible.

ECB Working Paper Series No 2850

25

observe higher labour market volatility, and then adjust the vacancy posting cost to match

the job finding probability.

Table 10: Matching function and labour firms

Parameter Poor Middle Rich

Labour endowment z

h

0.4923 1.0000 2.0313

Matching elasticity µ

z

h

0.5 0.5 0.5

Matching efficiency ϕ

z

h

0.6 0.6 0.6

Vacancy posting cost ψ

z

h

0.01 0.11 0.37

Entrepreneur’s share α

z

h

0.01 0.06 0.11

Wage rigidity ω

R

0.5 0.5 0.5

Job finding probability p

W

0.14 0.16 0.18

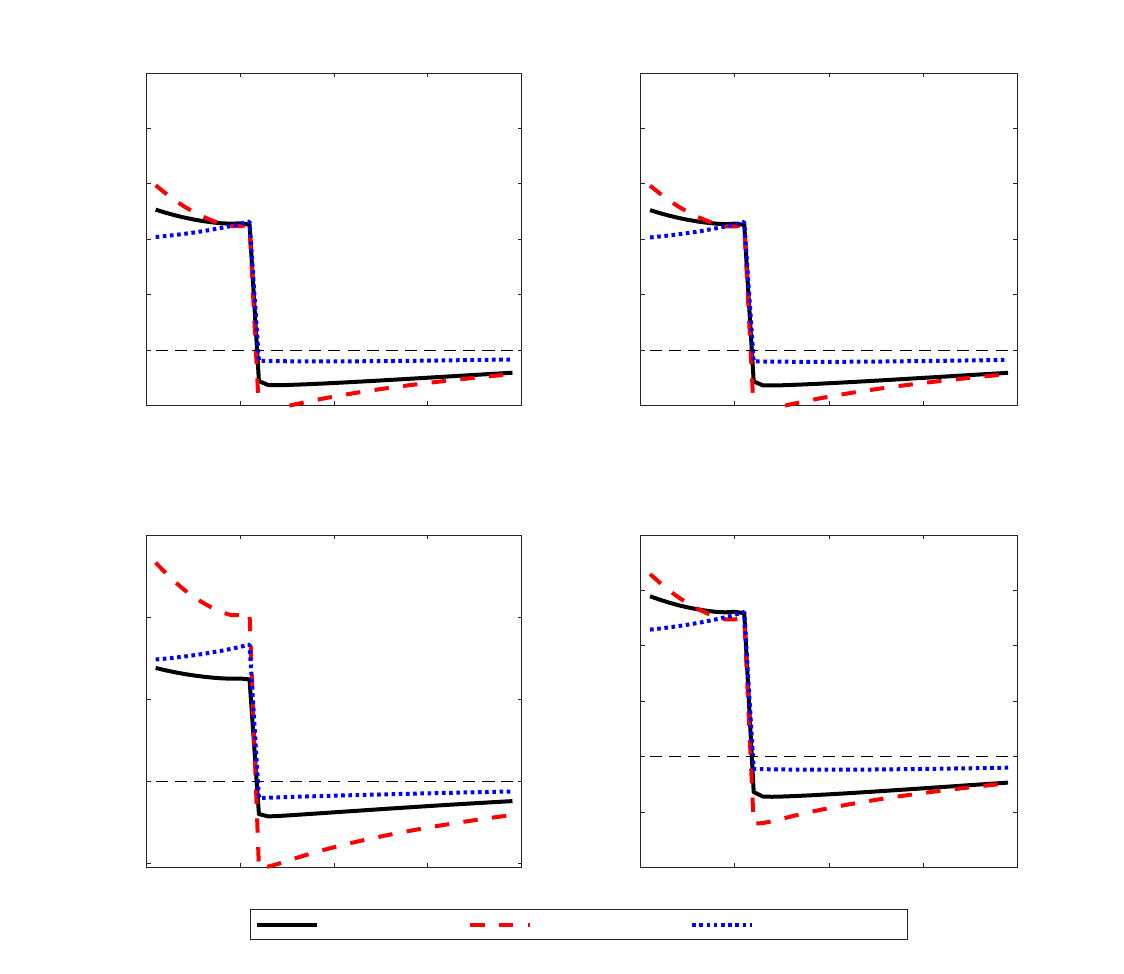

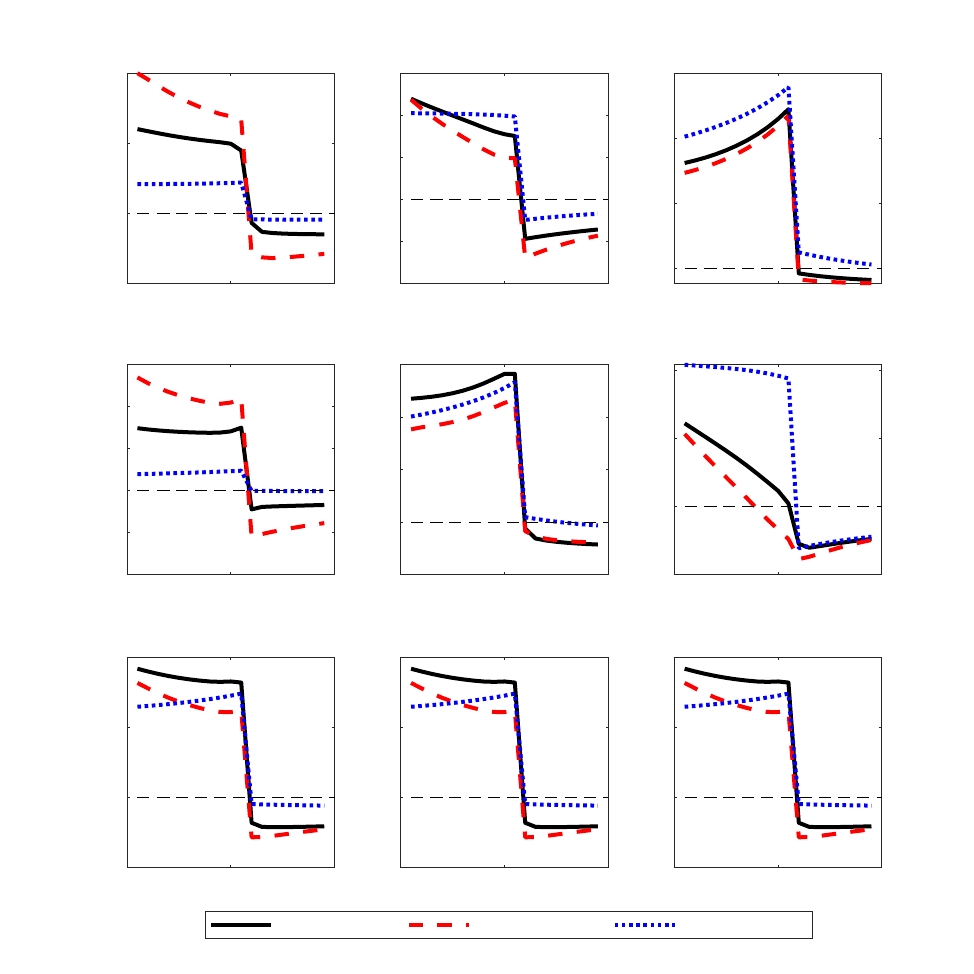

While modelled on Germany, this calibration is meant to represent the typical case found

in the labour data also for other European countries, such as France. We refer to this cali-

bration as ”Poor more volatile”. There are, however, countries such as Spain where there

seem to be fewer differences in terms of volatility and cyclicality between different labour

market segments (Table 14 in the appendix). To illustrate the difference this makes, we also