This paper presents preliminary findings and is being distributed to economists

and other interested readers solely to stimulate discussion and elicit comments.

The views expressed in this paper are those of the authors and do not necessarily

reflect the position of the Federal Reserve Bank of New York or the Federal

Reserve System. Any errors or omissions are the responsibility of the authors.

Federal Reserve Bank of New York

Staff Reports

Optimal Monetary Policy

According to HANK

Sushant Acharya

Edouard Challe

Keshav Dogra

Staff Report No. 916

February 2020

Optimal Monetary Policy According to HANK

Sushant Acharya, Edouard Challe, and Keshav Dogra

Federal Reserve Bank of New York Staff Reports, no. 916

February 2020

JEL classification: E21, E30, E52, E62, E63

Abstract

We study optimal monetary policy in a heterogeneous agent new Keynesian economy. A

utilitarian

planner seeks to reduce consumption inequality, in addition to stabilizing output gaps

and inflation. The

planner does so both by reducing income risk faced by households, and by

reducing the pass-through from

income to consumption risk, trading off the benefits of lower

inequality against productive inefficiency

and higher inflation. When income risk is

countercyclical, policy curtails the fall in output in recessions

to mitigate the increase in

inequality. We uncover a new form of time inconsistency of the Ramsey plan—the temptation to

exploit households' unhedged interest rate exposure to lower inequality.

Key words: new Keynesian model, incomplete markets, optimal monetary policy

_________________

Acharya, Dogra: Federal Reserve Bank of New York (emails: sushant.acharya@ny.frb.org,

keshav.dogra@ny.frb.org). Challe: CREST and Ecole Polytechnique (email:

edouard.chal[email protected]). The authors thank Florin Bilbiie, Christopher Carroll, Russell

Cooper, Clodomiro Ferreira, Antoine Lepetit, Galo Nuño, Pedro Teles, Gianluca Violante, and

Pierre-Olivier Weil for helpful discussions. They also received useful comments from seminar

participants at HEC Paris, UT Austin, UC3M, EUI, Université Paris-Dauphine, Université Paris

8, Banque de France, and CREST, as well as from conference participants at the Barcelona GSE

Summer Forum (Monetary Policy and Central Banking), the NBER Summer Institute (Micro

Data and Macro Models), the Salento Macro Meetings, SED, and T2M. Edouard Challe

acknowledges financial support from the French National Research Agency (Labex

Ecodec/ANR-11-LABX-0047). The views expressed in this paper are those of the authors and do

not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal

Reserve System.

To view the authors’ disclosure statements, visit

https://www.newyorkfed.org/research/staff_reports/sr916.html.

1 Introduction

It is increasingly recognized by researchers and policymakers that monetary policy can have important

effects on inequality. Despite this, the study of how monetary policy should be conducted optimally has

only recently begun to depart from a representative agent framework in which concerns about inequality

are trivially absent. While the large recent heterogeneous agent New Keynesian (HANK) literature has

shown that uninsurable idiosyncratic risk and inequality can dramatically change the positive effects of

monetary policy on the macroeconomy (See for example Ravn and Sterk (2017, Forthcoming); Kaplan et

al. (2018); den Haan et al. (2018); Auclert et al. (2018); Auclert (2019); Bilbiie (2019a) and many others),

the normative implications of HANK and the reciprocal effects of monetary policy on risk and inequality,

have been less well studied. This gap in the literature partly exists because characterizing optimal policy

in HANK economies is technically difficult. Solving for the Ramsey optimal policy involves choosing the

evolution of an infinite dimensional state variable (the wealth distribution), as well as infinite dimensional

controls (the distribution of consumption and hours worked across agents) subject to an infinite number

of constraints (each household’s optimality condition and budget constraints).

One approach to solving optimal policy problems for HANK economies is computational, and re-

searchers have recently started developing numerical algorithms to handle them (Bhandari et al., 2018).

We instead take an analytical approach. We study a standard NK economy with nominal rigidities with

the exception that households face uninsurable idiosyncratic risk. Markets are incomplete and agents can

only self-insure by trading a riskless bond or by working longer hours. We assume that households have

constant absolute risk (CARA) utility and idiosyncratic shocks are normally distributed. As in Acharya

and Dogra (2018), these assumptions imply that the economy permits linear aggregation which in turn

means that the infinite dimensional distributions of consumption, hours worked and wealth can be summa-

rized by their cross-sectional averages: the positive behavior of macroeconomic aggregates can be described

independently of the distribution of the wealth distribution. Of course, from a normative perspective, the

dispersion of wealth does affect social welfare and hence the optimal conduct of monetary policy. Crucially,

the effect of inequality on social welfare is also summarized by a finite dimensional sufficient statistic. This

makes the optimal policy problem analytically tractable, allowing us to drill down and identify exactly the

features that makes the optimal conduct of monetary policy different in HANK economies compared to

the RANK benchmark.

As is commonly known, in RANK the planner seeks to stabilize prices and keep output at its produc-

tively efficient level. In HANK, the planner has an additional objective - to use monetary policy to reduce

the cross-sectional consumption dispersion that results from the cumulated effects of uninsured idiosyn-

cratic shocks. This incentive is shut down in RANK by construction. We show that there are three ways in

which the planner can use monetary policy to achieve this purpose. First, the central bank may attempt

to reduce the amount of income risk that households are exposed to (the income risk channel). How to

achieve this reduction naturally depends on the cyclicality of income risk: if this risk is countercyclical,

then the central bank has an incentive to raise output in order to lower risk, while the opposite is true

if risk is procyclical. Either way, the central bank’s willingness and ability to manipulate the amount of

idiosyncratic risk that households face gives it an incentive to move output away from the level consistent

1

with stable prices and productive efficiency.

1

The second way in which the central bank may reduce consumption dispersion, independently of affect-

ing the level of income risk, is by reducing the pass-through from income risk to consumption risk, that is,

by lowering the marginal propensity to consume out of a change in individual income (the self-insurance

channel). This pass-through ultimately reflects the ability of the households to self-insure against idiosyn-

cratic risk through borrowing or working longer hours, and is thus affected by the paths of real interest

rates and wages going forward. On the one hand, lower interest rates make it easier for households to

borrow in response to an unfavorable shock, making individual consumption less response to changes in

individual income; this ultimately reduces consumption dispersion at any level of income risk. On the other

hand, higher wages going forward make it easier for households to buffer the impact of a fall in current

income on current consumption by borrowing today and working longer hours in the future to repay the

debt. When future wages are high, only a small increase in hours ( and hence the incurred dis-utility)

worked is required to repay this debt. This again makes individual consumption less responsive to changes

in current income. It follows that the central bank has an incentive to commit to low interest rates and

high wages –i.e., to be expansionary– going forward in order to reduce the pass-through from income risk

to consumption risk. This incentive is of course absent in RANK.

Finally, the central bank can reduce consumption dispersion through unanticipated changes in the

marginal propensity to consume out of wealth. Given a distribution of wealth, an unexpected fall in

interest rates benefits poor debtors, reducing their interest payments and increasing their consumption

(the unhedged interest rate exposure (URE) channel) (Auclert, 2019). Conversely, lower interest rates

reduce the interest income of rich savers, reducing their consumption. Overall, lower rates reduce the

marginal propensity to consume out of wealth, reducing consumption inequality. Importantly, this channel

(unlike the previous two) only operates for unexpected changes in interest rates, as we explain in more

detail in Section 4.

How does the presence of these three channels, through which the planner can affect inequality, change

the optimal conduct of monetary policy? As is commonly known, in RANK, optimal monetary policy

features divine coincidence in response to productivity shocks (Blanchard and Gal´ı, 2007): it is both

feasible and optimal to stabilize both the gap between output and its efficient level (output gap), and

inflation. In our RANK economy, in the empirically relevant case where income risk is countercyclical,

while it remains feasible to stabilize the output gap and inflation, it is no longer optimal to do so. But

to understand the tradeoffs that lead the planner to deviate from divine coincidence in this case, it is

instructive to start by examining a HANK economy where divine coincidence is optimal. This is the case

when risk is mildly procyclical and there is no initial wealth inequality. In this knife-edge case, the two

channels through which anticipated monetary policy affects consumption inequality exactly offset each

other: expansionary policy raises output and hence income risk, but makes it easier for households to self-

insure, leaving the consumption risk faced by households unchanged. In addition, the absence of wealth

inequality at date 0 mutes the URE channel. Thus, while the planner would like to reduce consumption

inequality, since it is not possible to do this with monetary policy, it remains optimal to stabilize both the

1

Earlier work has stressed that the cyclicality of income risk affects the response of aggregate demand in HANK economies

(Werning, 2015; Acharya and Dogra, 2018; Bilbiie, 2019a), and this in itself generically requires a benevolent central bank

to implement a different path of the policy rate than in RANK (Challe, 2020). This does not, however, necessarily warrant

departing from price stability.

2

output gap and inflation.

Away from this knife-edge case, monetary policy can, and does exploit the channels above to affect

consumption inequality. Suppose first that risk remains mildly procyclical so that income risk and self-

insurance channels offset each other, but there is wealth inequality at date 0. In this case, monetary policy

cannot affect inequality through the first two channels, but it can through the URE channel. Consequently,

the optimal plan features an unexpected cut in interest rates at date 0, which reduces consumption in-

equality at the cost of deviating from the efficient level of output and inflation. That is, optimal policy

features higher output and inflation at date 0 than would be optimal in RANK. While monetary policy

cannot affect inequality from date 1 onwards, output and inflation continue to deviate from RANK as

policy seeks to smooth the transition back to steady state. If policy was somehow prevented from creating

the boom to exploit the URE channel at date 0, it would not seek to deviate from RANK at any other

date either.

This brings us to the empirically relevant case of countercyclical risk. In this case expansionary mone-

tary policy can reduce inequality at all dates through the self-insurance and income risk channels: a lower

path of interest rates makes it easier for households to insure themselves, and makes a boom in output

which reduces the level of income risk households face. In addition, at date 0, a cut in rates delivers a

further reduction in inequality through the URE channel. Consequently, the planner always trades off this

benefit of more expansionary monetary policy - namely, that it reduces consumption inequality - against

the costs of inefficiently high output and inflation. These tradeoffs change the optimal response to produc-

tivity shocks, relative to RANK. Following a negative productivity shock, the planner lets output decline

as much as output in the flexible price case and implements zero inflation by raising nominal interest rates.

However, in HANK, optimal policy implements a lower path of nominal interest rates, curtailing the fall

in output in order to mitigate the increase in inequality. Even though this entails higher inflation and

output above its efficient level, this is optimal because inequality is already higher in recessions and so is

the benefit from a reduction in inequality.

So far we have only discussed one channel through which unexpected cuts in interest rates can lower

inequality (the URE channel). Several authors have highlighted another way in which unexpected changes

in monetary policy can lower inequality, namely the Fisher channel: unexpected inflation redistributes

from savers who hold nominal assets to debtors who hold nominal liabilities. We deliberately abstract

from this channel in our baseline model (by letting households trade inflation-indexed debt) in order to

emphasize that the URE channel does not depend on the ability of monetary policy to redistribute wealth

through an inflation surprise. While conceptually distinct from the URE channel, the Fisher channel

provides another avenue through which expansionary monetary policy can reduce inequality. In Section

6 we show that when households trade nominally denominated assets, optimal monetary policy is more

expansionary in recessions compared to RANK.

Related Literature The paper most closely related to ours is Bhandari et al. (2018), who also study

optimal monetary policy in a HANK model. The main difference between our paper and theirs is method-

ological. Bhandari et al. (2018) propose a numerical algorithm to derive optimal monetary policy in HANK

models, while we study a HANK economy with constant constant absolute risk aversion (CARA) prefer-

3

ences and normally distributed shocks which permits closed form solutions.

2

We see the two approaches as

inherently complementary: the first allows more flexibility in the structure of preferences and idiosyncratic

shocks, while the second better isolates the channels by which the central bank manipulates consumption

dispersion along the optimal policy plan. Another closely related paper is Nu˜no and Thomas (2019) who

study how URE and Fisher effects affect the optimal conduct of monetary policy in the presence of het-

erogeneity. Unlike us, they study a small open economy in which short-term real interest rates and output

are unaffected by monetary policy. Thus, the classic output inflation trade-off which is central to New

Keynesian economies is absent in their setting.

Several authors have studied optimal monetary policy in simple HANK economies with limited cross-

sectional heterogeneity–see, e.g., Bilbiie (2008); Bilbiie and Ragot (2018); Bilbiie (2019a) and Challe

(2020).

3

Most of these papers achieve tractability by imposing the zero liquidity limit (households can-

not borrow and government debt is in zero net supply).

4

This assumption rules out the self-insurance

channel because in equilibrium households do not borrow or lend and hence they spend all their income

on consumption. Our analysis shows that this assumption rules out an important channel through which

monetary policy affects inequality.

More generally, our paper belongs to the growing strand of literature that revisits the transmission and

optimality of various economic policies within the HANK framework. This includes not only the work on

conventional monetary policy discussed above but also that on unconventional monetary policy (McKay

et al., 2016; Acharya and Dogra, 2018; Bilbiie, 2019a; Cui and Sterk, 2019), on unemployment-insurance

and social-insurance policies (McKay and Reis, 2016, 2019; den Haan et al., 2018; Kekre, 2019), and on

fiscal policy (Auclert et al., 2018; Bilbiie, 2019b).

The rest of the paper is organized as follows. Section 2 presents the model. Section 3 characterizes

equilibria, defining the implementability constraints the planner faces. Section 4 shows that the utilitarian

planner’s objective function can be written in terms of aggregate variables and a single sufficient statistic

for the welfare-relevant measure of inequality. Section 5 characterizes optimal monetary policy. Section 6

introduces nominal bonds and shows how our results extend to that case. Section 7 concludes.

2 Environment

2.1 Households

We study a Bewley-Huggett economy in which households face uninsurable idiosyncratic shocks to their dis-

utility from supplying labor. We abstract from aggregate risk but allow for a one time unanticipated shock

at date 0, after which agents have perfect foresight. Our economy features a perpetual youth structure `a la

Blanchard-Yaari in which each individual faces a constant survival probability ϑ in any period. Population

is fixed and normalized to 1. Consequently, the size of a newly born cohort at any date t is 1 − ϑ and the

2

Caballero (1990), Calvet (2001), Wang (2003), Angeletos and Calvet (2006) have used similar modeling assumptions in

real economies. Recently, Acharya and Dogra (2018) shows that these assumptions are very helpful in understanding the

positive properties of HANK economies.

3

See also Nistic`o (2016), who generalizes the Two-Agent New Keynesian (TANK) model of Gal´ı et al. (2007) and Bilbiie

(2008) to the case of stochastic asset-market participation, and Debortoli and Gal´ı (2018) on the comparison between the

TANK model and a HANK model with homogeneous borrowing-constrained households and heterogeneous unconstrained

households.

4

Bilbiie and Ragot (2018) is an exception as it it allows agents to hold money in positive amounts for self-insurance purposes.

4

date t size of a cohort born at s < t is (1 −ϑ)ϑ

t−s

. The date s problem of an individual i born at date s is:

max

{c

s

t

(i),`

s

t

(i),a

s

t

(i)}

∞

X

t=s

(βϑ)

t−s

u

c

s

t

(i), `

s

t

(i); ξ

s

t

(i)

s.t.

c

s

t

(i) + q

t

a

s

t+1

(i) = w

t

`

s

t

(i) + a

s

t

(i) + T

t

(1)

a

s

s

(i) = 0 (2)

Agents have CARA preferences over both consumption and (disutility of) labor:

u

c

s

t

(i), `

s

t

(i); ξ

s

t

(i)

= −

1

γ

e

−γc

s

t

(i)

− ρe

1

ρ

[`

s

t

(i)−ξ

s

t

(i)]

(3)

Each agent i saves in riskless real actuarial bonds, issued by financial intermediaries (described below),

which trade at a price of q

t

at date t and pay off one unit of the consumption good at t + 1 if the agent

survives.

5

Each agent can take unrestricted positive or negative positions in the bond and these choices are

only disciplined by the transversality condition. T

t

denotes lump-sum transfers net of taxes and dividends

from the firms. For simplicity, we assume that dividends are equally distributed across agents.

A household supplies labor `

s

t

(i) at the pre-tax real wage w

t

. The agent faces uninsurable shocks ξ

s

t

(i) ∼

N

ξ, σ

2

t

to the dis-utility of supplying labor. ξ

s

t

(i) is independent across time and across individuals. A

larger realization of ξ

s

t

(i) reduces the dis-utility from work and, given wages, increases the household’s labor

supply. Equivalently, one may think of ξ

s

t

(i) as a shock to the household’s endowment of time available to

supply labor.

6

To see this, define leisure as l

s

t

(i) = ξ

s

t

(i) − `

s

t

(i). Then one can rewrite the period utility

functional (3) as −e

−γc

s

t

(i)

/γ − ρe

−l

s

t

(i)/ρ

and the budget constraint as:

c

s

t

(i) + w

t

l

s

t

(i) + q

t

a

s

t+1

(i) = w

t

ξ

s

t

(i) + a

s

t

(i) + T

t

(4)

The LHS of (4) denotes the purchases of consumption, leisure and bonds by the household while the RHS

denotes the notional cash-on-hand - the value of the household’s time endowment along with savings net

of transfers. Henceforth, we will simply refer to this as cash-on-hand. We allow for the possibility that the

variance of ξ, σ

2

t

, vary endogenously with the level of economic activity as we discuss below.

2.2 Financial intermediaries

There is a competitive financial intermediation sector which trades actuarial bonds with households and

trades government debt. An intermediary only needs to repay households that survive between t and t + 1.

5

In economies with a distribution of nominal debt, unexpected inflation redistributes wealth between creditors and debtors.

Bhandari et al. (2018) and Nu˜no and Thomas (2019) discuss how optimal monetary policy takes this into account. Our

benchmark economy deliberately abstracts from this channel in order to highlight the other ways in which optimal monetary

policy differs in HANK and RANK economies. In Section 6, we replace real debt with nominal debt, bring this channel back

into play and show how our results change.

6

We thank Gianluca Violante for suggesting this interpretation.

5

The representative intermediary solves:

max

a

t+1

,B

t+1

−ϑa

t+1

+ B

t+1

s.t. −q

t

a

t+1

+ Π

t+1

B

t+1

1 + i

t

≤ 0

where B

t

denotes government debt, a

t

denotes claims held by households, R

t

=

1+i

t

Π

t+1

is the gross real

return on government debt, i

t

is the nominal interest rate which is set by the monetary authority and Π

t+1

denotes gross inflation between t and t +1. Zero profits require that the intermediary sells/buy bonds from

the households at a price q

t

=

ϑ

R

t

and that ϑa

t+1

= B

t+1

.

2.3 Final goods producers

A representative competitive final goods firm transforms the differentiated intermediate goods y

j

t

, j ∈ [0, 1]

into the final good y according to the CES aggregator y

t

=

h

R

1

0

y

t

(j)

1

λ

dj

i

λ

. As is standard, the final good

producer’s demand for variety j is:

y

t

(j) =

P

t

(j)

P

t

−

λ

λ−1

y

t

(5)

where

λ

λ−1

is the elasticity of substitution between varieties.

2.4 Intermediate goods producers

There is a continuum of monopolistically competitive intermediate goods firms indexed by j ∈ [0, 1]. Each

firm faces a quadratic cost of changing the price of the variety it produces (Rotemberg, 1982). If firm j

hires n

t

(j) units of labor, it can only sell to the final goods firm the quantity:

y

t

(j) = z

t

n

t

(j) −

Ψ

2

P

t

(j)

P

t−1

(j)

− 1

2

y

t

(6)

where z

t

denotes the level of aggregate productivity at date t. Firm j solves:

max

{P

j

t

,n

j

t

,y

j

t

}

∞

t=0

∞

X

t=0

Q

t|0

P

t

(j)

P

t

y

t

(j) − (1 − τ)w

t

n

t

(j)

subject to (5) and (6) where Q

t|0

=

Q

t

s=0

R

−1

s

. This yields the standard Phillips curve:

(Π

t

− 1) Π

t

=

λ

Φ (λ − 1)

1 −

z

t

(1 − τ) λw

t

+

1

R

t

y

t+1

z

t

w

t

y

t

z

t+1

w

t+1

(Π

t+1

− 1) Π

t+1

(7)

2.5 Government

The monetary authority sets the interest rate on nominal government debt. The fiscal authority subsidizes

the wage bill of firms at a rate τ and rebates lumpsum taxes/transfers to all households equally. The

government budget constraint is given by:

B

t+1

1 + i

t

= P

t

T

t

+ τP

t

w

t

Z

1

0

n

t

(j)dj + B

t

(8)

6

We further assume that government debt is in zero net supply, B

t

= 0 for all t ≥ 0.

2.6 Market clearing

In equilibrium, the markets for the final good, labor and assets must clear:

y

t

= (1 − ϑ)

t

X

s=−∞

ϑ

s−t

Z

i

c

s

t

(i)di

Z

1

0

n

t

(j)dj = (1 − ϑ)

t

X

s=−∞

ϑ

s−t

Z

i

`

s

t

(i)di

0 = a

t

= (1 − ϑ)

t

X

s=−∞

ϑ

s−t

Z

i

a

s

t+1

(i)di

where the last equation holds because B

t

= 0 for all t.

2.7 Shocks

As mentioned previously, we abstract from aggregate risk but allow for a one time unanticipated aggregate

shock to the level of labor productivity z

0

at date 0. We assume that the shock decays geometrically:

ln z

t

= %

t

z

ln z

0

for %

z

∈ [0, 1).

3 Characterizing equilibria

As in Acharya and Dogra (2018), CARA preferences and normally distributed shocks imply that the

model aggregates linearly and the distribution of wealth does not directly affect the dynamics of aggregate

variables. We begin by describing optimal household decisions in equilibrium.

Proposition 1 (Household Decision Rules). In equilibrium, the optimal date t consumption and labor

supply decisions of a household i born at date s are:

c

s

t

(i) = C

t

+ µ

t

x

s

t

(i) (9)

`

s

t

(i) = ρ ln w

t

− γρc

s

t

(i) + ξ

s

t

(i) (10)

where x

s

t

(i) = a

s

t

(i) + w

t

ξ

s

t

(i) −

ξ

is demeaned cash-on-hand, C

t

denotes aggregate consumption and µ

t

is the “marginal propensity to consume” (MPC) out of cash-on-hand. These evolve according to:

C

t

= −

1

γ

ln βR

t

+ C

t+1

−

γµ

2

t+1

w

2

t+1

σ

2

t+1

2

(11)

µ

−1

t

= 1 + γρw

t

+

ϑ

R

t

µ

−1

t+1

(12)

Proof. See Appendix A

To understand the role of market incompleteness in explaining the behavior of consumption and la-

bor supply it is useful to compare equations (9) and (10) to their counterparts under complete markets.

7

Under complete markets, all households are insured against dis-utility shocks, i.e. the marginal utility of

consumption e

−γc

s

t

(i)

and the marginal dis-utility of work e

1

ρ

(`

s

t

(i)−ξ

s

t

(i))

are equalized across all states and

so:

∂c

s

t

(i)

∂ξ

s

t

(i)

= 0 and

∂`

s

t

(i)

∂ξ

s

t

(i)

= 1. Thus, since households’ consumption is insured, a household which draws a

temporarily higher dis-utility from working can reduce hours without experiencing a drop in consumption.

Instead, when markets are incomplete (9) and (10) imply that:

∂c

s

t

(i)

∂ξ

s

t

(i)

= µ

t

w

t

> 0 and

∂`

s

t

(i)

∂ξ

s

t

(i)

= 1 − γρµ

t

w

t

< 1

For example, after a negative ξ shock (i.e., greater dis-utility from working), consumption declines instead

of remaining constant while labor supply does not fall quite as much as under complete markets. While

households use credit and labor market to insure themselves to some extent, these are not perfect substitutes

for Arrow securities, so agents are only able to partially insulate themselves from the shock. When the

dis-utility of labor rises, households would like to work less, but reducing hours as much as under complete

markets would cause consumption to drop too much. The optimal response to the shock is to use labor

supply for self-insurance, i.e. to work longer hours than under complete markets.

7

Proposition 1 also states that the MPC out of cash-on-hand is the same across individuals; (12) describes

its evolution over time. Intuitively, consider a household i that receives an additional dollar at date t. They

will optimally choose to spend dc

s

t

(i) = µ

t

of the dollar in the current period. Since consumption and leisure

are normal goods, they also reduce hours worked by γρµ

t

, resulting in γρw

t

µ

t

less income. Saving the

remaining 1 − µ

t

(1 + γρw

t

), they find themselves with da

s

t+1

(i) =

R

t

ϑ

[1 − µ

t

(1 + γρw

t

)] next period out

of which they will consume dc

s

t+1

(i) = µ

t+1

da

s

t+1

(i). Finally, it is optimal to smooth consumption so that

dc

s

t

(i) = dc

s

t+1

(i) which yields µ

t

= µ

t+1

R

t

ϑ

[1 − µ

t

(1 + γρw

t

)]. Rearranging this expression yields equation

(12). Iterating forwards yields:

µ

t

=

1

P

∞

s=0

Q

t+s|t

(1 + γρw

t+s

)

The MPC µ

t

, which measures the pass-through from a fall in cash-on-hand to consumption, is increasing in

current and future interest rates and decreasing in current and future wages. This is because interest rates

and wages affect households’ ability to use the bond and labor markets, respectively, for self-insurance.

Consider a household who receives an unfavorable shock ξ < 0. The household responds by working less

today, borrowing in order to mitigate the decline in consumption, and working longer hours in the future.

A lower path of interest rates reduces the cost of borrowing, making it easy to self insure using the bond

market and lowering the responsiveness of consumption to changes in cash-on-hand. Similarly, higher

future wages reduce the (disutility) cost of working more hours in the future since even a small increase

in hours worked suffices to repay the same debt. This too lowers the sensitivity µ

t

of consumption to

cash-on-hand.

8

While the sensitivity of household consumption to shocks (µ

t

) depends on the factors we have just

described, the average level of consumption in the economy C

t

depends on interest rates relative to impa-

7

As already mentioned, the model can be re-interpreted as one with an idiosyncratic time-endowment shock and utility

from leisure time. In this interpretation, both consumption and leisure time stay constant under complete markets, while both

co-vary with the idiosyncratic shock under incomplete markets.

8

While Acharya and Dogra (2018) already discuss how the MPC responds to future real interest rates, the path of wages

has no effect on the MPC in their paper because their environment features inelastic labor supply. In this model, however,

since households can choose how much labor to supply, they use this additional margin to self-insure.

8

tience and households’ desire for precautionary savings, as shown in equation (11). Absent idiosyncratic

risk, σ

t

= 0, (11) is a standard Euler Equation; higher real interest rates relative to household impatience

raise consumption growth. The last term in (11) reflects precautionary savings. Given (9), the conditional

variance of date t + 1 consumption of household i is V

t

c

s

t+1

(i)

= µ

2

t+1

w

2

t+1

σ

2

t+1

. To the extent that

consumption risk is positive and households are prudent (γ > 0), households save more than in a riskless

economy for the same interest rate, i.e. they choose a steeper path of consumption growth. The variance

of consumption, in turn, depends on both the variance of cash-on-hand V

t

x

s

t+1

(i)

= w

2

t+1

σ

2

t+1

, and the

pass-through of cash-on-hand risk into consumption risk measured by the (squared) MPC µ

2

t+1

.

Determination of y

t

In a symmetric equilibrium, aggregating (6) across firms, we have:

y

t

= z

t

n

t

−

Ψ

2

(Π

t

− 1)

2

y

t

(13)

Aggregating labor supply (10) across currently alive households and using goods and labor market clearing:

n

t

= ρ ln w

t

− γρy

t

+ ξ (14)

Combining the two equations above, we have:

y

t

= z

t

ρ ln w

t

+ ξ

1 + γρz

t

+

Ψ

2

(Π

t

− 1)

2

(15)

where

Ψ

2

(Π

t

− 1)

2

denotes the resource cost of inflation - higher inflation reduces output.

Deriving the aggregate IS equation Imposing goods market clearing in (11) yields the aggregate IS

equation which describes the relation between output today and tomorrow:

y

t

= y

t+1

−

1

γ

ln β

i + i

t

Π

t+1

−

γµ

2

t+1

w

2

t+1

σ

2

t+1

2

(16)

Time varying σ

t

Following McKay and Reis (2019), we allow for the variance of ξ shocks to vary

endogenously with economic activity so that the model generates cyclical changes in the distribution of

earnings risks. In particular, we assume that σ

2

t

w

2

t

= σ

2

w

2

e

2φ(y

t

−y)

where y denotes steady state output

and φ =

∂ ln V(x)

∂y

is the constant semi-elasticity of the variance of cash-on-hand w.r.t output. This flexible

specification allows the variance of cash-on-hand V

t

(x) to be either increasing in y

t

(procyclical risk), when

φ > 0; decreasing in y

t

(countercyclical risk), when φ < 0; or independent of the level of y

t

(acyclical risk)

when φ = 0.

3.1 Steady state

We now characterize allocations in the zero inflation steady state. We normalize the level of productivity

z = 1 in steady state. Imposing Π

t

= Π

t+1

= 1 in (7) requires that steady state wages w =

1

λ(1−τ)

. Given

9

this wage, steady state output is y =

ρ ln w+ξ

1+γρ

. Imposing steady state in (16) and (12) yields:

R = β

−1

e

−

Λ

2

and µ =

1 −

e

β

1 + γρw

(17)

where Λ = γ

2

µ

2

w

2

σ

2

denotes the consumption risk faced by households in steady state (scaled by the

coefficient of prudence) and

e

β =

ϑ

R

is the steady state price of an actuarial bond. Observe that the

presence of uninsurable risk (Λ > 0) implies that the equilibrium real interest rate R < β

−1

. Furthermore,

the steady state distribution of cash-on-hand x in the population is given by:

F (x) = (1 − ϑ)

∞

X

s=0

ϑ

s

Φ

x

wσ

√

s + 1

(18)

where Φ(·) is the cdf of the standard normal distribution. This follows since, conditional on survival, x is

a random walk with no drift and a variance of w

2

σ

2

in steady state.

3.2 Linearized demand block

The demand block of the economy, given a path of interest rates, can be described by the IS equation

(16), the MPC recursion (12) and the definition of GDP (15). Before analyzing optimal policy, it is useful

to compare the dynamics of this HANK economy to its RANK counterpart. It is easiest to compare the

first-order Taylor expansion of the equations describing aggregate dynamics in the neighborhood of the

zero inflation steady state, which are:

9

by

t

= Θby

t+1

−

1

γ

(i

t

− π

t+1

) −

1

γ

Λbµ

t+1

(19)

bµ

t

= −(1 −

e

β)

γρw

1 + γρw

bw

t

w

+

e

β (bµ

t+1

+ i

t

− π

t+1

) (20)

by

t

=

ρ

1 + γρ

bw

t

w

+

y

1 + γρ

bz

t

(21)

where Θ = 1 −

Λφ

γ

. In RANK, there is no idiosyncratic risk, i.e. σ

2

= 0 which implies Θ = 1 and Λ = 0, so

that (19) becomes the standard RANK IS curve. As discussed in Acharya and Dogra (2018), uninsurable

idiosyncratic risk changes the IS equation in two ways. First, it can introduce either discounting (Θ < 1)

or compounding (Θ > 1) depending on the cyclicality of risk. If risk is acyclical, φ = 0, then Θ = 1 as

in the RANK IS equation. If risk is procyclical φ > 0 then Θ < 1 and there is discounting in the IS

equation. This is because in this situation low future output implies low idiosyncratic income risk, hence

(all else equal) a fall in precautionary savings that mutes down the effect of the forthcoming recession

on current aggregate demand. The opposite occurs when risk is countercyclical (φ < 0), in which case

Θ > 1 –that is, we have compounding in the IS equation–, because then the impact of a future recession

on current aggregate demand is magnified by the rise in precautionary savings. Second, the strength of

the precautionary motive depends not only on the level of income risk but also on its pass-through to

consumption risk, i.e. bµ

t+1

, which in turn depends of the future path of real interest rates and wages. By

committing to a lower path of real rates or a higher path of wages, monetary policy can lower the strength

9

We linearize y

t

and w

t

in levels while all other variables are log-linearized.

10

of the precautionary savings motive at any level of income risk.

Equations (7), (12), (15) and (16) summarize the optimality conditions of the private sector and define

the implementability constraints faced by the central bank. We may now turn to its objective function.

4 Objective function of the planner

We assume that the planner maximizes a utilitarian criterion; at any date t the planner assigns equal

weights to the welfare of all households currently alive and a weight of β

s−t

on the welfare of cohorts

who will be born at dates s > t. Given these Pareto weights, the planner’s objective can be written as

maximizing

P

∞

t=0

β

t

U

t

where U

t

, the period t felicity function of the planner is simply the average utility

of all surviving agents:

10

U

t

= −(1 − ϑ)

0

X

s=−∞

ϑ

−s

Z

u

c

s

t

(i), `

s

t

(i); ξ

s

t

(i)

di,

This expression for U

t

feature the full cross-sectional distribution of agents and is in general not tractable.

Fortunately, it can be greatly simplified by exploiting our CARA-Normal structure again.

Proposition 2 (Social Welfare Function). The period felicity function U

t

can be written as

U

t

= u(y

t

, n

t

; ξ)Σ

t

where

Σ

t

= (1 − ϑ)

0

X

s=−∞

ϑ

−s

e

1

2

γ

2

σ

2

c

(t,s)

and σ

2

c

(t, s) is the date-t cross-sectional dispersion of consumption amongst the surviving households from

the cohort born at date s ≤ t, i.e., c

s

t

(i) ∼ N

y

t

, σ

2

c

(t, s)

.

Proof. See Appendix B.2.

Intuitively, u(y

t

, n

t

; ξ) is the notional flow utility of the representative agent, i.e., the period utility

functional (3) evaluated at aggregate consumption y

t

, aggregate labor supply n

t

, and mean labor dis-

utility ξ. Σ

t

can be thought of as the welfare cost of inequality, and is increasing in the within cohort

dispersion of consumption. In a riskless economy, there would be no consumption dispersion and hence

Σ

t

= 1 at all dates. However, in the presence of risk, Σ

t

> 1, reducing welfare relative to this representative

agent benchmark. Recall that u(·) < 0 and so higher Σ

t

reduces welfare.

10

Note that the planner discounts felicity at the same rate as the households would themselves. Consider a change in

allocations which reduces the date t felicity of cohort s by du

t

and increases their date t + 1 felicity by du

t+1

, while keeping

the felicity at all other dates and for all other agents the same. A cohort s individual will be indifferent regarding this change

if du

t

= βϑdu

t+1

. From the planner’s perspective this changes aggregate welfare by −ϑ

s−t

du

t

+ βϑ

s+1−t

du

t+1

. Thus, the

planner will be indifferent about this change if and only if the individuals themselves are indifferent. As discussed by Calvo

and Obstfeld (1988), assuming that the planner and the households share the same rate of time preference ensures that social

preferences are time-consistent, so that the first-best intertemporal allocation of consumption across cohorts does not change

over time. This does not prevent other from of time inconsistencies from arising in decentralized equilibrium (as shown below),

but these are unrelated to the form of social preferences.

11

Appendix B.2.1 shows that the evolution of Σ

t

for t > 0 can be written as:

ln Σ

t

=

1

2

γ

2

µ

2

t

w

2

t

σ

2

t

+ ln [1 − ϑ + ϑΣ

t−1

] (22)

with

ln Σ

0

=

1

2

γ

2

µ

2

0

w

2

0

σ

2

0

+ ln [1 − ϑ + ϑΣ

−1

] + ln

1 − ϑe

Λ

2

1 − ϑe

Λ

2

µ

0

E

−1

µ

0

2

| {z }

effect of date 0 surprise / URE

(23)

where Σ

−1

= Σ =

(1−ϑ)e

Λ

2

1−ϑe

Λ

2

is the steady state Σ.

11

Intuitively, higher cash-on-hand risk w

2

t

σ

2

t

and a higher

pass-through µ

t

both tend to increase consumption inequality. In addition, consumption inequality inherits

the slow moving dynamics of wealth inequality, as can be seen from the presence of Σ

t−1

in (22).

12

Equation (23) shows that the relation between µ

0

and Σ

0

is different than the relation between µ

t

and Σ

t

at all other dates. This can be explained intuitively as follows. At the beginning of date 0, the

distribution of wealth a is at its steady state level: some households have positive net wealth and some

are debtors. Since savers and debtors have different unhedged interest rate exposures (UREs) in the sense

of Auclert (2019), an unanticipated change in interest rates affects consumption inequality. Suppose that

at date 0, the central bank chooses a policy path that implements a transitory drop in the real interest

rate. The lower interest rates benefit poor debtors, reducing their interest payments and allowing them to

increase their consumption. By the same token, a lower path of rates reduces the interest income of rich

savers, causing them to reduce consumption. In other words, lower rates reduce the MPC out of wealth

(µ

0

↓) which reduces consumption inequality and hence Σ

0

.

Importantly, an anticipated cut in rates would not reduce inequality as much as this unanticipated cut.

If wealthy agents at date t − 1 anticipated lower rates at date 0, they would save more in order to insure

a higher level of consumption at date 0. Equally, the poor debtors would borrow more at date -1 knowing

that their debt would be less costly to repay. For this reason, what reduces Σ

0

through this channel is not

a fall in µ

0

per se but a fall in µ

0

relative to its expected value E

−1

µ

0

, as can be seen from the last term

in (23). To be clear, anticipated cuts in rates do reduce inequality as discussed earlier: lower µ

t

reduces

Σ

t

in equation (22). But there is an additional effect that comes from a surprise fall in rates. In our

environment, since we do not have aggregate shocks (except for the unanticipated shock at date 0) and the

fact that the Ramsey planner is only allowed to re-optimize at date 0 imply that this additional affect of

an unanticipated change in µ can only occur at date 0. More generally, in an environment with aggregate

shocks, surprise changes in µ would have this effect on any date, for example when there is an aggregate

productivity shock and z

t

6= E

t−1

z

t

.

Of course, this one-off redistribution would not operate in the absence of wealth inequalities at time

0. If the economy were starting with equal (zero) wealth for all households, instead of starting from the

invariant distribution, then only the first effect would play out and the equilibrium value of consumption

11

We are assuming that the economy is in steady state at date −1.

12

Note that within-cohort consumption dispersion σ

2

c

(t, s) in general rises without bounds as the cohort ages (i.e., as

t − s → ∞), due to the cumulated effect of idiosyncratic shocks on the distribution of cash-on-hand. However, since every

cohort gradually shrinks in size, while newborn cohorts have little consumption dispersion (i.e., σ

2

c

(t, t) = µ

2

t

w

2

t

σ

2

t

), Σ

t

does

not necessarily blow up. In fact, provided that the survival rate ϑ < e

−Λ/2

, Σ

t

is stationary.

12

dispersion at time zero would simply be:

ln Σ

0

=

1

2

γ

2

µ

2

0

w

2

0

σ

2

0

. (24)

5 Optimal monetary policy

The planner chooses sequences {w

t

, Π

t

, µ

t

, Σ

t

, i

t

, n

t

}

∞

t=0

to maximize

P

∞

t=0

β

t

u

y

t

, n

t

; ξ

Σ

t

subject to the

aggregate Euler equation (16), agggregate labor supply (14), the evolution of µ

t

(12), the Phillips curve

(7), the evolution of Σ

t

(22)-(23) and the relationship between GDP and wages (15). In the RANK version

of our economy, σ = 0 and (22) is replaced by Σ

t

= 1 for all t. Appendix D presents the Lagrangian

associated with this problem along with the first order necessary conditions for optimality.

5.1 Long run outcomes under the optimal Ramsey plan and the payroll subsidy

To proceed further, we need to take a stand on the value of the payroll subsidy τ. In RANK, if we imposed

a production subsidy to eliminate the distortions caused by market power, zero inflation is optimal in the

long run in the absence of aggregate shocks. This need not be true in our HANK economy where σ > 0

and so Σ

t

is endogenous. As in the standard NK model, the Phillips curve (7) implies a long-run trade-off

between inflation and economic activity:

(Π − 1)Π =

λ

(1 −

e

βϑ

−1

)(1 − λ)Ψ

1 −

1

(1 − τ)λw

(25)

The presence of a long-run tradeoff implies that the policymaker can move wages (or equivalently output)

above or below its flexible-price level by persistently deviating from price stability. While it is not optimal

to do so in RANK, it may in fact be optimal in HANK because the level of economic activity affects both

the amount of income risk households face w

2

t

σ

2

t

and their ability to self-insure against this risk, µ

t

. For

example, if income risk is countercyclical, Θ > 1 the planner may want to create inflation to raise wages

(and output) above the level consistent with productive efficiency (w > 1), and thereby reduce income risk.

To make our results as comparable as possible to the classic NK literature on optimal monetary policy,

we eliminate this motive for deviating from price stability by introducing an appropriately chosen payroll

subsidy τ . To see how this works, consider the case with countercyclical risk in which the planner wants

to implement a high after-tax wage w > 1 in the long run in order to reduce inequality. From (25) it is

easy to see that if τ =

λ−1

λ

(the standard subsidy used in the RANK literature, such a high level of wages

entails a marginal cost greater than 1 which implies positive long run inflation Π > 1. However, if the

payroll subsidy is larger, the steady state marginal cost can be brought down to 1, consistent with zero

inflation in the long run.

More generally, Appendix D.1 shows that in the presence of an appropriately chosen payroll subsidy to

ensure zero inflation Π = 1, the planner’s first-order condition for wages - which states that the net-benefit

13

of higher economic activity must be zero at an optimum - becomes:

13

Ω

|{z}

benefit from

reduction of

inequality

≡

Λ

(1 −

e

β)(1 − Λ)

| {z }

reduction of inequality

due to low interest rates

+

Θ − 1

(1 −

e

β)(1 − Λ)

| {z }

reduction of inequality

due to high output

=

w − 1

1 + γρw

| {z }

cost of deviating

from productive efficiency

(26)

Equation (26) implies that the steady state wage and payroll subsidy consistent with the optimality of zero

long-run inflation satisfy:

w =

1 + Ω

1 − γρΩ

and τ =

λ − 1

λ

+

1 + γρ

λ

Ω

Ω + 1

(27)

Ω summarizes the benefit from a reduction in consumption inequality due to higher economic activity. The

planner has the option to reduce interest rates and raise output above the flexible price level. Equation

(27) states that at an optimum, the marginal benefit of lower inequality due to lower rates and higher

output, Ω, must equal the marginal cost of distorting productive efficiency by raising output (and wages)

above the flexible price level which is proportional to w − 1, the negative of the labor-wedge.

Absent uninsurable risk (Λ = 0, Θ = 1), there is no inequality and so there is no benefit from higher

economic activity in terms of reducing inequality, Ω = 0. Consequently, in RANK, optimal policy equates

the cost of deviating from productive efficiency in steady state to 0 and hence w = 1 in the long run. In

this case, Π = 1 in steady state can be implemented with the standard RANK subsidy τ =

λ−1

λ

(from eq.

(27)) which removes the monopolistic distortion.

In the presence of risk (Λ > 0), optimal monetary policy seeks to reduce consumption inequality. This

can be accomplished both by reducing labor income risk w

2

t

σ

2

t

and by making it easier for households to

self-insure against this risk (by reducing µ

t

). Thus the policymaker may want to deviate from productive

efficiency and price stability, both to facilitate self-insurance and to reduce income risk; equation (26)

shows that Λ and Θ − 1 represent the strength of these two motives respectively.

Consider first the self-insurance channel. When Θ = 1, income risk is acyclical: the level of economic

activity does not affect household income risk. In this case, deviating from price stability and productive

efficiency (say by implementing a wage w > z = 1) delivers no benefits in terms of lower income inequality

(second term on the LHS of (26) is zero). However, lowering real interest rates still makes it easier for

households to smooth consumption by borrowing and reduces the pass-through from income shocks into

consumption, measured by the first term of the LHS, reducing consumption inequality. Lower interest

rates and the associated higher level of economic activity also have a cost, since they distort output and

employment above the productively efficient level. Optimal policy equates these costs and benefits. So,

even with acyclical risk, Ω > 0, and output is optimally above productive efficiency in the long run. Since

higher wages increase the firms marginal cost, it takes a higher payroll subsidy than in RANK τ >

λ−1

λ

to

implement Π = 1 in steady state.

Next, consider the income risk channel. When Θ > 1, income risk is countercyclical: higher economic

activity lowers income risk. In this case, stimulating output above its productively efficient level lowers

consumption inequality even for a fixed µ; in addition, the lower interest rates necessary to implement

13

Note that here there is no term representing the cost of inflation, precisely because we assume that whatever the steady

state level of wages, the appropriate payroll subsidy is chosen so that firms’ marginal costs are consistent with zero inflation

in the long-run, i.e., (25) holds with Π = 1.

14

higher output reduce µ further reducing consumption inequality. Thus, the benefit from higher output is

even larger than if Θ = 1 - both LHS components in (26) are positive and Ω is larger - and so output (and

wages) must be even further above the productive efficient level than if Θ = 1. Again, it takes a higher

payroll subsidy τ >

λ−1

λ

to implement Π = 1 in steady state.

In contrast, when risk is procyclical (Θ < 1), the effect of higher economic activity and lower rates on

consumption inequality are ambiguous. While lower rates decrease the passthrough from income shocks to

consumption (Λ > 0), they also raise output which now increases income risk (Θ − 1 < 0). For sufficiently

procyclical risk, the second effect dominates, Ω < 0 and the optimal steady state level of output (and

wages) is below the productively efficient level. In this case, it takes a lower payroll subsidy than

λ−1

λ

to

implement Π = 1 in steady state. For mildly procylical risk, the self-insurance channel dominates and

Ω > 0 with w > 1 in steady state. The self-insurance channel is perfectly balanced by the income risk

channel if 1 − Θ = Λ in which case Ω = 0; higher economic activity and low interest rates have no first

order effect on consumption inequality and in this case, the planner does not wish to distort productive

efficiency in steady state, setting w = 1. The Ω = 0 case will be a useful benchmark in what follows.

Remark 1 (Comparison with Zero-Liquidity Limits). The self-insurance channel is absent in models which

feature incomplete markets but impose the zero liquidity limit such as Bilbiie (2019a,b); Ravn and Sterk

(2017); Challe (2020) and others. Zero liquidity implies that in equilibrium, the passthrough from income

risk to consumption risk is invariant to policy since it always equals 1. Instead, our analysis emphasizes

that in HANK economies interest rate policy affects welfare not just via its effect on the level of economic

activity, as in RANK, but also by affecting the ease with which households can self-insure.

As is standard in the NK literature, a useful benchmark is the level of output under flexible prices. In

a flexible-price version of the HANK economy, we would have w

t

= wz

t

at all times, and output would be

y

n

t

= z

t

ρ (ln w + ln z

t

) +

¯

ξ

1 + γρz

t

while the efficient level of output is:

y

e

t

= z

t

ρ ln z

t

+

¯

ξ

1 + γρz

t

In RANK, the flexible-price and efficient levels of output coincide: y

e

t

= y

n

t

. This is also true in HANK with

Ω = 0. But in general, when Ω 6= 0, the flexible-price and efficient levels of output no longer coincide. With

strongly procyclical risk Ω < 0, the flexible-price level of output y

n

t

is always below its efficient level y

e

t

,

while with mildly procyclical or countercyclical risk Ω > 0, y

n

t

is always above y

e

t

. Using these definitions,

we can express the linearized version of the Phillips curve (7) as:

π

t

=

e

β

ϑ

π

t+1

+ κ (by

t

− by

n

t

) (28)

where κ =

1+γρ

ρΨ

λ

λ−1

, by

e

t

=

ρ+1

1+γρ

bz

t

and by

n

t

=

ρ+y

1+γρ

bz

t

.

5.2 Calibration

While our results are primarily analytical, when plotting IRFs we parameterize the model as follows.

We choose

¯

ξ to normalize aggregate steady state output y

∗

to 1 in the HANK economy with Ω = 0

15

(equivalently, in the RANK economy). We calibrate the model to an annual frequency and choose the

standard deviation of ξ

s

t

(i), σ, so that the standard deviation of income in steady state equals 0.5.

14

This

is in line with Guvenen et al. (2014) who using administrative data find the standard deviation of 1 year

log earnings growth rate to be slightly above 0.5. We set the slope of the Phillips curve κ = 0.01, and the

elasticity of substitution between varieties

λ

λ−1

to 10, implying a 10 percent steady state markup, λ = 1.1.

We set the coefficient of relative prudence for the median household, −

cu

000

(c)

u

00

(c)

= γ, to be 3, within the range

of estimates in the literature (see e.g. Cagetti (2003); Fagereng et al. (2017); Christelis et al. (2015)). We

set r = 4%. ρ can be interpreted as the Frisch elasticity of labor supply for the median household; we set it

equal to 1/3, within the range of estimates from the micro literature. We set the persistence of the shock

%

z

= 0.8. Following Nistic`o (2016), we set ϑ = 0.85. Finally, we consider two values for the cyclicality of

income risk: φ = γ (which implies Ω = 0), and φ = −3 (which implies Ω > 0 and countercyclical risk).

Finally, we set ξ = 1 + γρ to normalize the efficient level of output in steady state to 1.

5.3 Dynamics under optimal monetary policy under RANK

As is common in the NK literature, we characterize optimal policy by linearizing the first order conditions

arising from the planner’s Lagrangian (presented in Appendix E). It is useful to compare this characteri-

zation to optimal policy in a RANK version of our economy.

Lemma 1 (Optimal monetary policy in RANK). In RANK (Λ = 0, Θ = 1), output and inflation {by

t

, π

t

}

∞

t=0

under optimal policy satisfy

η

t

= by

t

− by

n

t

(29)

η

t

= η

t−1

−

λ

λ − 1

π

t

(30)

π

t

=

e

β

ϑ

π

t+1

+ κ (by

t

− by

n

t

) (31)

where η

t

is the (normalized) multiplier on the Phillips curve (7) and is defined in Appendix E.1.

Proof. See Appendix E.1.

Combining (29)-(30), we see that optimal policy in RANK satisfies the standard target criterion:

15

(by

t

− by

n

t

) −

by

t−1

− by

n

t−1

+

λ

λ − 1

π

t

= 0 (32)

where by

−1

= by

e

−1

= 0. Combining this with (31) and using the fact that by

n

t

= by

e

t

in RANK, we see that the

economy features a divine coincidence: it is both feasible and optimal for monetary policy to set by

t

= by

e

t

and π

t

= 0 at all dates and states. Given the appropriate steady state subsidy τ =

λ−1

λ

, the flexible-price

level of output, which is also consistent with zero inflation, maximizes social welfare –there is no tradeoff

between implementing the efficient level of output and price stability.

14

The standard deviation of income is given by (1 − γρµw)wσ. We calibrate all parameters except the cyclicality of income

risk to an economy with Ω = 0, which implies w = 1.

15

See for example, chapter 5 in Gal´ı (2015).

16

5.4 Dynamics of monetary policy under HANK

In HANK, the planner has an additional objective relative to RANK: in addition to stabilizing inflation

and keeping output close to its efficient level, she wants to keep inequality Σ

t

as low as possible. The

innovations to inequality depend on consumption risk µ

2

t

σ

2

t

which in turn depends on both income risk σ

2

t

and the pass-through µ

2

t

. This can be seen from the linearized version of (22) which is given by:

b

Σ

t

Σ

=

γ (1 − Θ) by

t

+ Λbµ

t

| {z }

consumption

risk

+

ϑ

βR

b

Σ

t−1

Σ

for t > 0

γ (1 − Θ) by

0

+ Λbµ

0

+

ϑΛΣ

1−ϑ

bµ

0

for t = 0

(33)

One way to reduce consumption inequality is to affect the level of output: with procyclical risk (Θ < 1)

lower output directly reduces income risk (Θ > 1) faced by households while with countercyclical risk,

a higher level of output is necessary to reduce income risk. An alternative path to lower consumption

inequality is to commit to a lower path of interest rates which reduces pass-through from income to

consumption risk.

However, the planner only has one instrument - the nominal interest rate. Lowering the nominal interest

rate lowers the pass-through from income risk to consumption risk (measured by µ

t

) but increases output.

If risk is countercyclical Θ > 1, then this too reduces consumption risk. However, if risk is procyclical

Θ < 1, then it increases income risk, leaving the overall effect on consumption risk unclear. To see what

combinations of {by

t

, bµ

t

} that the planner can implement with some path of nominal interest rates, combine

the IS equation (19), µ recursion (20) using the definition of GDP (21) and solve forwards:

γ

h

1 +

1 −

e

β

Ω

i

by

t

+ bµ

t

=

1 −

e

β

(1 + Ω)

γy

y + ρ

∞

X

s=0

e

β

s

(1 − Λ)

s

by

n

t+s

≡ Γ

t

(34)

where Γ

t

is an exogenous process driven by the sequence {y

n

t

}, which in turn depends solely on {bz

t

}.

5.4.1 HANK with Ω = 0

To understand the trade-offs facing the planner, it is useful to consider the special case in which Ω = 0

(or equivalently 1 − Θ = Λ). Recall from (26) that this is the case in which the zero inflation steady state

features productive efficiency (Π = 1, w = 1). This benchmark features mildly procyclical risk: while this

may not be the empirically relevant case, it is a useful benchmark because in this case, the constraint

on the planner’s ability to affect consumption inequality is particularly severe. Recall that when risk is

procyclical, the effect of expansionary monetary policy on consumption inequality is generally ambiguous:

higher output reduces the level of income risk, but lower interest rates reduces the passthrough from income

to consumption risk. When Ω = 0, both these effects exactly cancel each other out and consumption is

invariant to monetary policy to first-order. To see this, note that (33) becomes:

b

Σ

t

Σ

=

Λ(γby

t

+ bµ

t

) +

ϑ

βR

b

Σ

t−1

Σ

for t > 0

Λ(γby

0

+ bµ

0

) +

ϑΛΣ

1−ϑ

bµ

0

for t = 0

(35)

17

while (34) becomes:

γby

t

+ bµ

t

= Γ

t

(36)

Clearly, in this case, the planner cannot affect the evolution of consumption risk for dates t > 0 which is

solely driven by exogenous shocks {y

n

t

}

t≥0

denoted Γ

t

in (36). Plugging in (36) into (35) shows that the

evolution of inequality after date 0 is governed completely by the exogenous sequence {Γ

t

}:

b

Σ

t

Σ

=

ΛΓ

t

+

ϑ

βR

b

Σ

t−1

Σ

for t > 0

ΛΓ

0

+

ϑΛΣ

1−ϑ

bµ

0

for t = 0

(37)

Again, while a cut in interest rates lowers bµ

t

, it increases output by

t

and hence income risk, leaving con-

sumption risk unchanged. A higher path of aggregate productivity {bz

t

} (which implies a higher path of

{by

n

t

}) increases consumption risk in this case and monetary policy cannot do anything to prevent it: higher

productivity tends to increase output and hence the level of income risk that households face but tighter

monetary policy, which would be needed to forestall the rise in output, tends to make µ higher which itself

increases consumption risk.

Even though changes in interest rates (and hence µ) cannot affect consumption inequality after date

0, the planner can affect consumption inequality at date 0 (and thus at all subsequent dates, because

b

Σ

t

depends on

b

Σ

t−1

). This is because monetary policy changes after date 0 are anticipated while the date

0 change in monetary policy is unanticipated. As described in section 4, an unanticipated cut in interest

rates (and hence µ

0

) effectively redistributes from savers to borrowers. To be clear, since we have an

economy where agents hold real (and not nominal) claims, this is not because inflation redistributes date

0 real wealth from savers to borrowers: the date 0 distribution of real wealth is unaffected.

16

But the

distribution of consumption is affected, as rich savers find that they receive a lower return on their bond

holdings than they had anticipated while poor debtors find that their interest payments are smaller than

they had expected.

In sum, while the planner seeks to reduce consumption inequality in addition to stabilizing prices and

the gap output and its flexible-price level, this is not possible after date 0 since (to first order) the evolution

of consumption inequality is unaffected by policy. Effectively, then after date 0, the planner faces the same

trade-off between output and inflation as in the RANK economy. At date 0, it is possible to reduce

consumption inequality via a surprise cut in interest rates which exploits households’ unhedged interest

rate exposure. Thus, the planner has an additional motive to cut rates at this date. This is reflected in

the optimal design of monetary policy, as we now demonstrate.

Proposition 3 (Optimal monetary policy with Ω = 0). Output and inflation {by

t

, π

t

}

∞

t=0

under optimal

16

Section 6 discusses the case where households hold nominal debt.

18

policy satisfy

η

t

=

α (by

t

− δby

n

t

− χ) for t = 0

by

t

− by

n

t

for t ≥ 1

(38)

η

t

=

1

βR

η

t−1

−

λ

λ − 1

π

t

(39)

π

t

=

e

β

ϑ

π

t+1

+ κ(by

t

− by

n

t

) (40)

where α > 1, 0 < δ < 1 and χ > 0 are defined in Appendix E.1 and η

t

is the (normalized) multiplier on the

Phillips curve (40).

Proof. See Appendix E.1.

Combining (38) and (39), we get the following target criterion for all dates t > 1:

(by

t

− by

n

t

) −

1

βR

by

t−1

− by

n

t−1

+

λ

λ − 1

π

t

= 0 (41)

Comparing equations (32) and (41) shows that when Ω = 0 the target criteria in HANK and RANK for

t > 0 are almost identical (under complete markets we have βR = 1 so the former collapses to the latter).

This reflects that fact that monetary policy cannot affect consumption risk at dates t > 0, and thus faces

the same tradeoff as RANK. But this is not true at t = 0, where the target criterion is:

by

t

− δby

n

t

+

1

α

λ

λ − 1

π

t

= χ (42)

Equation (42) shows that at time 0 optimal policy in HANK deviates from that in RANK in three ways.

First, it is optimal to create a boom at date 0. To see this most clearly, suppose that productivity is at its

steady-state value, so by

n

t

= bz

t

= 0 for all t. Even in this case, it is optimal to move away from by

0

= π

0

= 0

and implement an output boom by

0

> 0 which is accompanied by inflation π

0

> 0. This is because, as

discussed earlier, the evolution of Σ

t

is different at date 0, compared to all other dates. A surprise cut

in interest rates at date 0 reduces consumption inequality–as is summarized by the last term of (37) for

t = 0. The constant term χ > 0 in the date-0 target criterion (42) reflects exactly this benefit from cutting

rates and reducing inequality at date 0. This is not because it is infeasible to set by

t

= by

e

t

= 0 and π

t

= 0

in the HANK economy; this remains feasible, and it remains costly for the planner to deviate from this

benchmark. But the costs of doing so are balanced by benefits of reducing consumption inequality via

a surprise interest rate cut. Note that the desirability of exploiting households’ unhedged interest-rate

exposure for redistribution (the URE channel) makes the Ramsey plan time-inconsistent. Suppose that

the planner has been following a Ramsey plan since t = −∞ and the economy has converged to steady

state. Given the opportunity to deviate from this plan at date 0, the planner would do so, lowering interest

rates temporarily - i.e. the continuation of a Ramsey plan is not a Ramsey plan.

Second, whereas in RANK, optimal policy seeks to move output by

t

one-for-one with its efficient level

by

e

t

(= by

n

t

in RANK), which fluctuates due to productivity shocks, under HANK it is optimal to track the

flexible-price level of output by

n

t

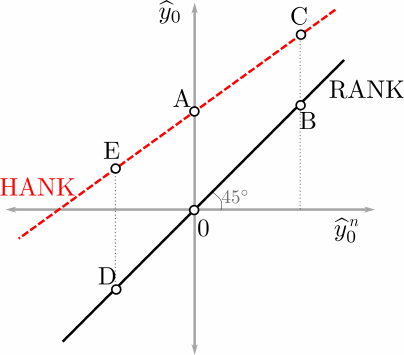

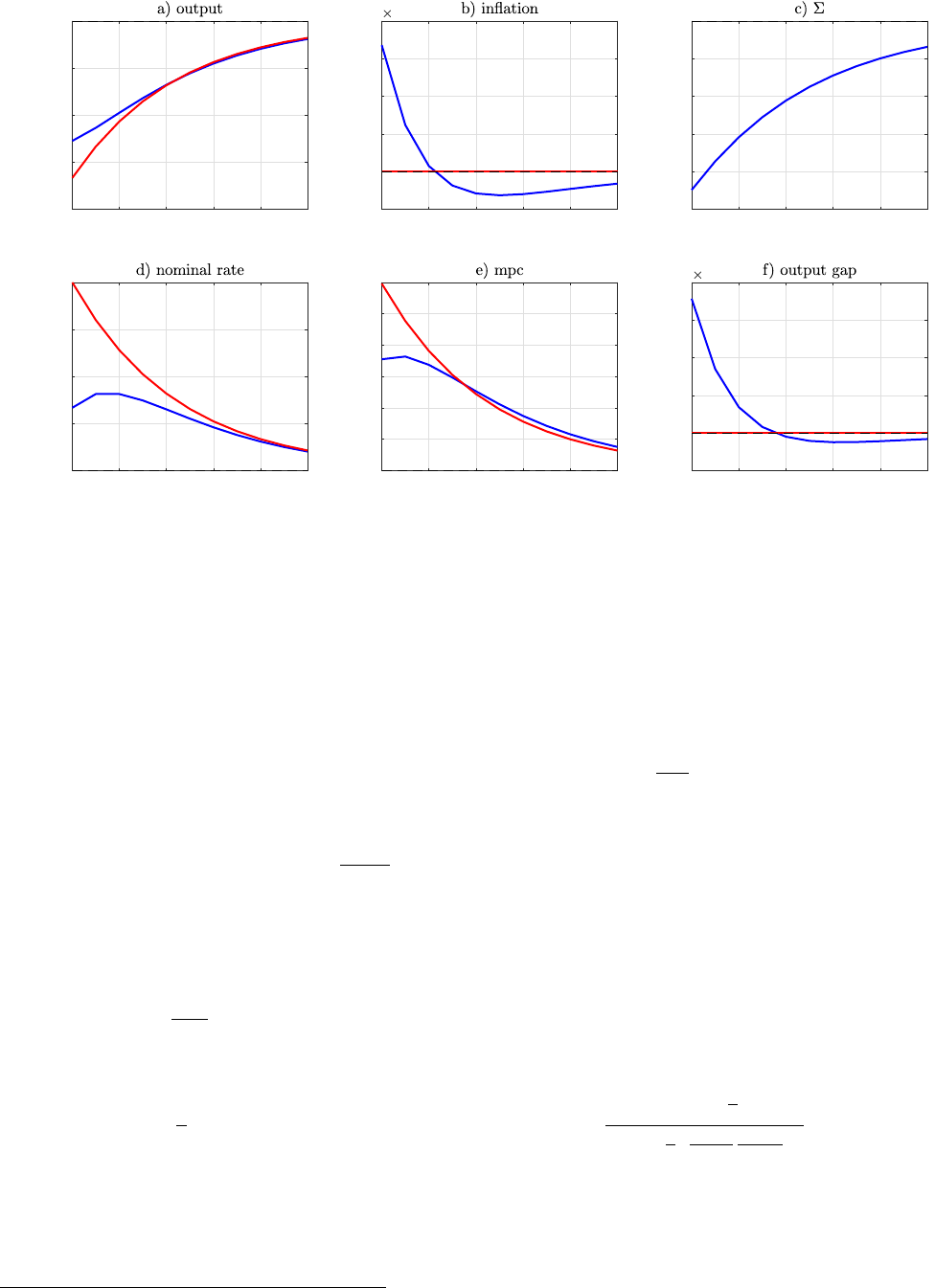

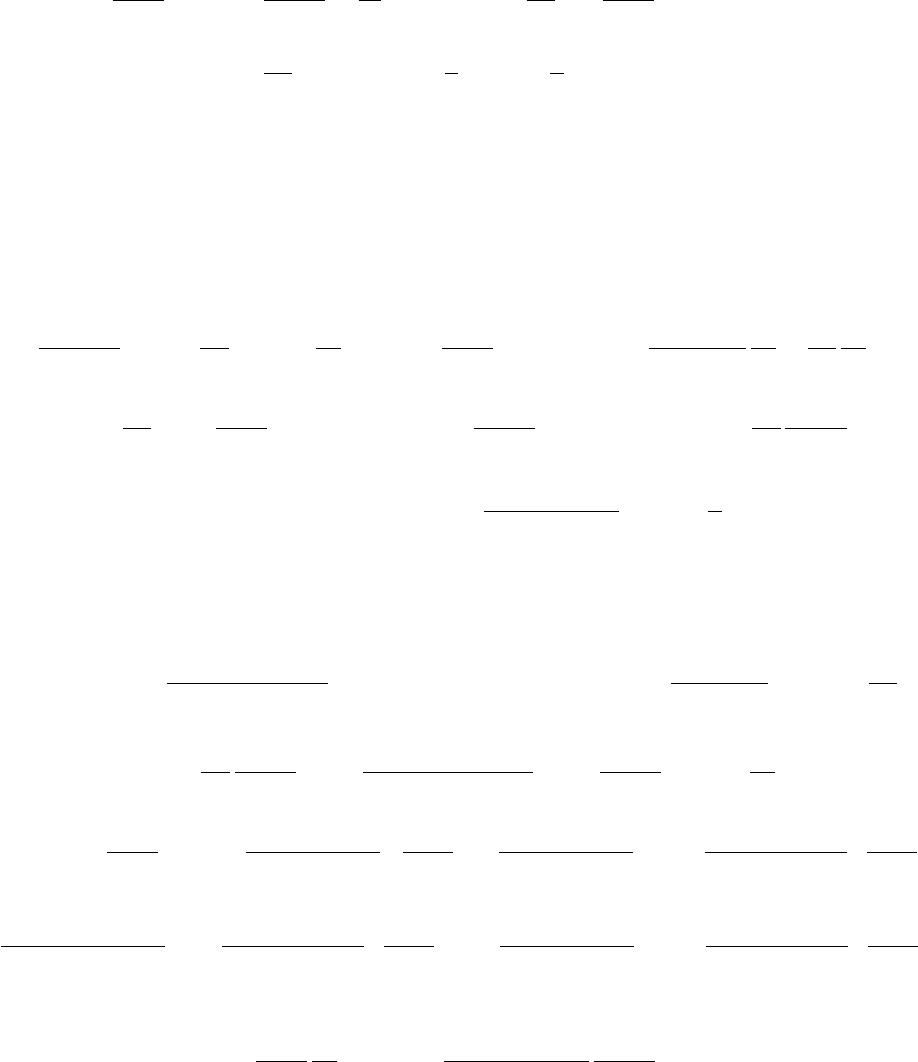

less than one-for-one. In other words, 0 < δ < 1 in (42). Figure 1 depicts

the optimal level of date 0 output as a function of flexible-price level of output by

n

t

in HANK and RANK.

19

Figure 1. Optimal level of by

0

in HANK (Ω = 0) and RANK absent markup shocks

First, suppose, by

n

0

= 0. In RANK, it is optimal to track this and to set by

0

= by

n

0

= 0. But in HANK there

is a first order benefit from cutting interest rates to reduce inequality, creating a boom in output, until

the marginal benefit of an additional reduction in nominal rates is outweighed by the cost of distorting

output further above its efficient level (point A in Figure 1). Next, suppose that by

n

0

> 0. Again, the

RANK planner sets by

0

= by

n

0

(denoted by point B in the Figure). If the HANK planner were also to set

by

0

= by

n

0

> 0, this would already generate a surprise fall in interest rates, which would reduce inequality to

some extent. The HANK planner still perceives some additional benefit to reducing inequality further but

the marginal benefit is smaller since inequality has already been reduced. Consequently, it is not optimal

to deviate as much from productive efficiency as in the case by

n

0

= 0, and so the gap between points C and

B is smaller than that between points A and the origin. Conversely, when by

n

0

< 0, tracking the flexible

price allocation would entail a surprise interest rate increase which would increase consumption inequality.